Economists associate the mass distress of firms during recessions with Joseph Schumpeter’s creative destruction theory, which says that during downturns small, less efficient, younger firms are the ones to exit the market. Their exit allows for more efficient firms to expand, lifting overall productivity. In a global pandemic like COVID, however, this theory may be on less certain grounds, as recent LSE research suggests.

In our latest LSE working paper, we test this theory directly. In particular, we use firm-level data for 11,148 firms across 34 countries to approximate the financial distress of manufacturing companies. We rely on firms’ responses to various questions in the World Bank’s Enterprise Surveys from 2016 to 2020 regarding firms’ age, sales, costs, external financing, employment, export orientation and product diversification.

We examine firm characteristics that previous studies relate to the likelihood of financial distress. The first measure for firm size is the number of employees in the previous fiscal year. For the sample population of 11,148 firms, the employees’ mean is 123 while the median is 30.

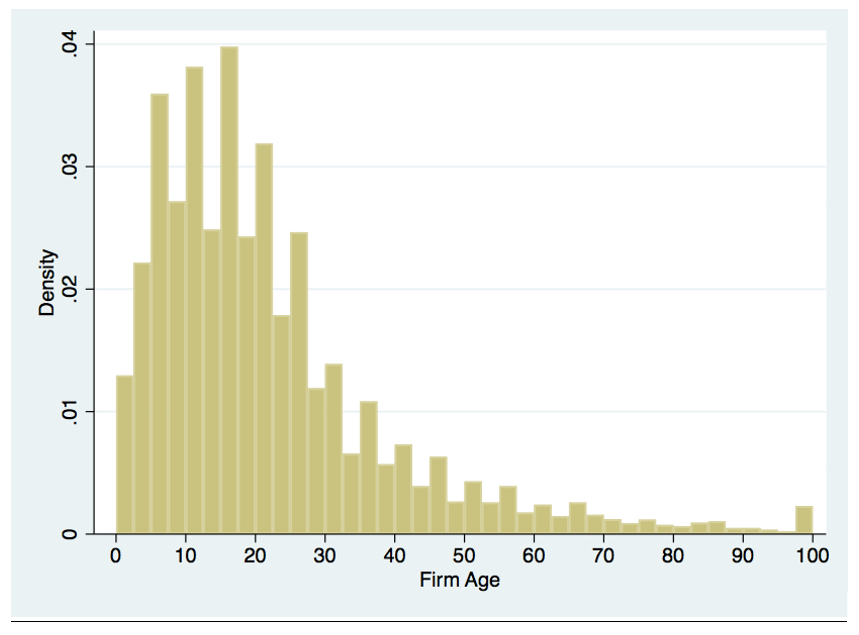

The second measure for firm size is a firm’s total sales from the previous fiscal year. The third measure is firm’s age. Firms have ages clustered between 0 and 50 years, with 99% of the companies being younger than 100 years old (figure 1). The average firm age is 22 years, while the median is 17 years. Uzbekistan has the lowest average firm age of 12 years, while Italy has the highest average of 35 years. Some Italian firms have existed for over 150 years, lasting through previous pandemics. For median age, Rwanda and Uzbekistan have the lowest age of nine years while Italy again has the highest of 31 years.

Figure 1. Distribution of firm age

Source: World Bank’s Enterprise Surveys, https://www.enterprisesurveys.org/. The sample constitutes 34 countries with surveys in the past 5 years and with a sample size above 50 firms.

In addition to the main measures related to firm size, we use a measure to account for the reliance on exports for sales revenue. For export intensity, we use firms’ responses to the question “In the last Fiscal Year, what percent of your total annual sales came from direct as well as indirect exports?”. Looking at the distribution of export reliance, we see that many firms do not export at all: 50% of firms reported no exporting and the mean fraction of sales from exports is merely 15% per cent. By country, Sierra Leone had the lowest average export reliance of 3% while Moldova had the highest average of 39%.

Simulating corporate distress

We employ Edward Altman’s version of the Z-score, as adapted for private firms. The private specification of the Z-score is an alternative to the original score that allows for the substitution of book value of equity instead of market value of equity. The Altman Z-Score employs seven accounting ratios: earnings before income and taxes (EBIT), total assets, net sales, the book value of equity, total liabilities, working capital, and retained earnings.

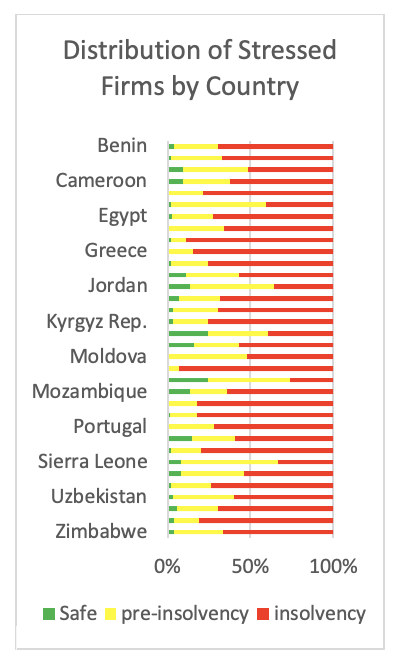

A score above 2.9 is indicative of a solvent firm. A score between 1.23 and 2.9 relates to firms that should be on alert for insolvency risk. A score below 1.23 is highly predictive of insolvency (figure 2). In half-dozen countries (Gambia, Greece, Mongolia, Myanmar, Nicaragua and Zambia) four out of every five firms fall to insolvency due to COVID.

Figure 2. Simulated insolvency by country (50% sales decline)

Source: World Bank’s Enterprise Surveys, https://www.enterprisesurveys.org/. The sample constitutes 34 countries with surveys in the past five years and with a sample size above 50 firms.

Since we do not have access to standard balance sheets in the data, we make assumptions based on survey responses to obtain the needed ratio inputs. EBIT is calculated as the firm’s total annual sales minus its total costs of goods sold. ‘Total assets’ is approximated as the sum of total sales and the market value of the firm’s machinery. ‘Net sales’ uses the annual sales responses. ‘Working capital’ and ‘retained earnings’ are both approximated as the firm’s profit after taxes, the latter also assuming 10% dividends and 15% depreciation. To calculate the firm’s total debt, we utilise responses to the question “What percentage of your working capital is financed from internal funds/retained earnings?”. ‘Book value of equity’ is the difference between total assets and outstanding debt, and total liabilities is the sum of ‘equity’ and ‘debt’.

Characteristics of distressed firms

We next perform various tests to see what determinants of financial health hold in economic crisis, assuming a fifty per cent fall in annual sales. A 1% increase in employment predicts an increase in z-score of between 0.03 and 0.04 points. Higher sales also play a role, with a 1% increase in sales predicting an increase of between 0.07 and 0.08 points for the z-score. Firm age is a weaker but still significant determinant of financial distress. The effect of export reliance is positive and significant.

Taken together, the results suggest that Schumpeter’s theory of creative destruction holds some credence even in a large pandemic-driven crisis. The magnitude of the possible insolvency during COVID-19, however, may dictate government intervention, something Joseph Schumpeter would no doubt have disapproved.

♣♣♣

Notes:

- This blog post is based on Firms in Financial Distress, by Simeon Djankov and Jeremy Evans, Special Paper 260 of LSE’s Financial Markets Group.

- The post expresses the views of its author(s), not the position of LSE Business Review or the London School of Economics.

- Featured image by Marco Bianchetti on Unsplash

- When you leave a comment, you’re agreeing to our Comment Policy

Simeon Djankov is policy director of the Financial Markets Group at LSE and a senior fellow at the Peterson Institute for International Economics (PIIE). He was deputy prime minister and minister of finance of Bulgaria from 2009 to 2013. Prior to his cabinet appointment, Djankov was chief economist of the finance and private sector vice presidency of the World Bank. He is the founder of the World Bank’s Doing Business project. He is author of Inside the Euro Crisis: An Eyewitness Account (2014) and principal author of the World Development Report 2002. He is also co-editor of The Great Rebirth: Lessons from the Victory of Capitalism over Communism (2014).

Simeon Djankov is policy director of the Financial Markets Group at LSE and a senior fellow at the Peterson Institute for International Economics (PIIE). He was deputy prime minister and minister of finance of Bulgaria from 2009 to 2013. Prior to his cabinet appointment, Djankov was chief economist of the finance and private sector vice presidency of the World Bank. He is the founder of the World Bank’s Doing Business project. He is author of Inside the Euro Crisis: An Eyewitness Account (2014) and principal author of the World Development Report 2002. He is also co-editor of The Great Rebirth: Lessons from the Victory of Capitalism over Communism (2014).

I do not agree with the article. Recent events with the pandemic have proven that little may actually be better. The UK high street has been decimated. Statistics are dangerous. The current pandemic has proven how many companies considered strong are not. Sadly, In the UK larger firms carry smaller firms along while absorbing their working capital. Changes need to be made in insolvency laws to protect smaller businesses.

I act as a partner in an Insolvency Practice and see every day the results of the companies act deficiencies. Talk about shouting out once the Bull has escaped out of the field. Perhaps, major changes are required to limit insolvencies rather than prosecute directors, many who guarantee their business with their homes, rather than the larger companies who tend not too.