In the early days of 2020, when measures to contain the coronavirus pandemic hurt economies worldwide, many publicly listed firms omitted or suspended their dividend payments. For investors across the world, who seek for or solely rely on dividend income, this situation caused great difficulty. By the end of 2021, dividends had bounced back. Globally, 90 per cent of companies either increased their dividends or maintained them steady. Erhan Kilincarslan analyses key developments affecting dividend policies.

The dividend policy of firms is one of the most “puzzling” issues in finance and investment—questions such as why some companies pay dividends, and some do not, why investors care, and to what extent dividend policy may affect a firm’s market value have been subject to a long-standing argument. Although dividend experts offer various explanations and attempt to provide extensive empirical reasoning, the dividend puzzle remains unsolved.

One obvious reason why companies distribute their corporate earnings to shareholders is that dividends are a source of income for investors to finance their own liabilities and consumption needs. When the coronavirus pandemic struck economies worldwide in the early days of 2020, many publicly listed firms omitted or suspended their dividend payments. For investors across the world, who seek for or solely rely on dividend income, this situation has caused great difficulty.

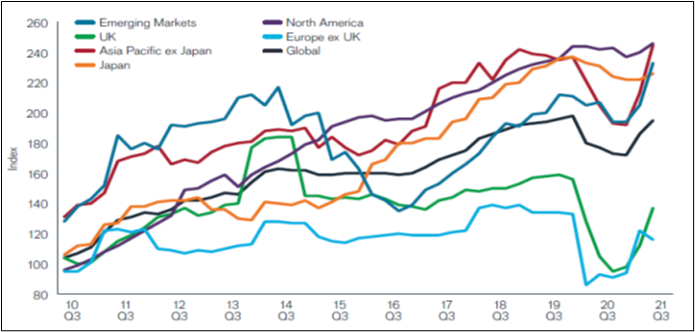

Figure 1. Dividends bounced back globally

Source: Janus Henderson Investors

The good news is that global dividends had bounced back strongly by the end of 2021 after the major cuts of 2020, mainly due the pandemic. According to the latest global dividend index of Janus Henderson Investors, companies all over the world have kept recovering from the pandemic. Increasing profits and solid balance sheets enabled them to raise dividends by a 22 per cent on an underlying basis – an all-time high for Q3 pay-outs in 2021.

Janus Henderson’s report further highlights that globally 90 per cent of companies either increased their dividends or maintained them steady. Dividends in North America were not cut much during 2020, thus they displayed less growth than the global average, but still US dividends rose by 10.2 per cent on an underlying basis reaching an all-time record for Q3. Whereas Europe and parts of Asia and emerging markets also showed large increases. Nevertheless, countries such as Australia and the UK, which experienced the steepest cuts in 2020, have exhibited the greatest rebounds.

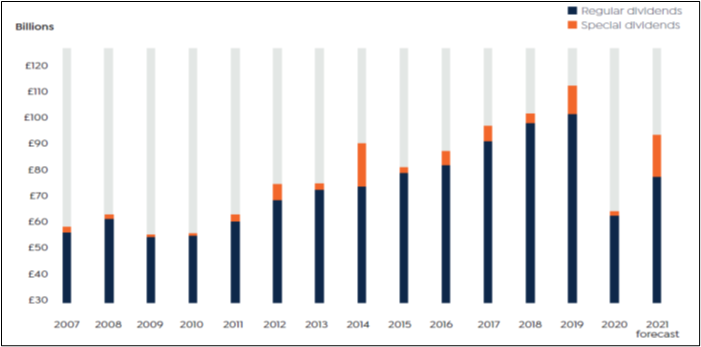

Figure 2. UK dividends coming back strongly

Source: Link Group

The latest UK Dividend Monitor report from Link Group also highlights the strong recovery in UK dividends in the post-pandemic. Link Group forecasts that total dividends, including special payouts, could reach over £93 billion with an increase of about 44.8 per cent on 2020.

The dividend debate in the UK

This is great news for income investors in the UK stock market. Indeed, UK-listed companies have a tradition of distributing generous dividends by pursuing stable dividend payments. One of the major reasons is that the UK equity market is highly characterised by institutional investors, who hold very large shareholdings, and they generally have a taste for sizeable dividends – especially, long-horizon institutions typically tend to influence UK managers to distribute higher payouts.

The rise in UK payouts is actually good for tax-exempt investors (e.g., pension funds, insurance companies, and charities), who prefer income to retentions due to their tax advantage on dividends, and for those financial institutions (e.g., fund managers) that are subject to the common institutional charter and prudent-person rule restrictions – long-term and steady dividends would satisfy their liquidity needs on an ongoing basis to fund their activities and serve as an income source for reinvestments.

From the signalling perspective, cash dividends are a useful device to convey insider information about corporate performance to outsiders in reducing the information asymmetry. In this respect, the strong rebound of UK dividends from the coronavirus pandemic can be considered as a credible signal of returning to strength in earnings and cashflows among companies – so does the British economy. This signal, then, increases investor confidence in dividend-friendly companies which in turn reflects in their share prices.

Now, for the caveat – progressive taxation and high dividends increase investors’ tax burden. In fact, recently the UK has announced that a 1.25 percentage point increase in taxes on dividend income will take effect from 6 April 2022 to help fund health and social care services. The increase in dividend taxation will definitely raise a red flag for UK companies that make regular payouts to shareholders and for investors looking for income.

Another concern involving high payouts is that dividends are a drawback for potential growth opportunities when companies choose to pay large amounts of internally generated cash to shareholders rather than reinvesting it in positive net present value projects. It is indeed argued that the long record of UK stock market’s tendency to prioritise dividends over any other kind of return slows down growth and thus the UK is falling behind the US and Chinese markets.

The new rules (the Pension Schemes Act 2021) set by the UK Pensions Regulator came into force on 1 October 2021 and will surely add new pieces to the dividend puzzle. Under new rules, company directors could face a legal challenge if a dividend distribution results in a “material reduction” in the recovery that a defined benefit pension scheme can expect to get in the event of a hypothetical insolvency.

In the aftermath of COVID-19, the dividend tax rise and new rules would actually prompt UK companies to think much more carefully while setting their dividend polices. Also, investors and portfolio managers will have to re-evaluate their investment strategies when shaping their portfolios – perhaps, this will significantly increase investments in venture capital trusts and share repurchase practices. However, it would be interesting to see how UK dividends will evolve in the new era, from the points of view of both corporate policymakers and investors.

♣♣♣

Notes:

- This blog post represents the views of its author(s), not necessarily those of the European Commission, LSE Business Review or the London School of Economics and Political Science.

- Featured image by Mathieu Stern on Unsplash

- When you leave a comment, you’re agreeing to our Comment Policy.

I think that there is less of a puzzle than financial theory makes out to be honest. I sometimes feel that that people view dividends paid from listed equities as different to dividends paid from private ones. When someone invests in a private business, they expect a return on that capital and unless they work there, they either get rewarded by a dividend or at some point the business must be sold. The dividend paid in that situation is what the company can pay, after investment. With listed equities there is the added possibility of selling shares in the market, but the is no guarantee that you think it is a good time to sell, and no guarantee that not paying a dividend will enhance the capital value (see corporate Japan for an example of cash hoarding depressing values). Therefore, if you don’t get a dividend you can end up getting a very poor return on your investment, especially in falling or flat equity markets.