Fears about robots taking people’s jobs are overplayed, say Rui Costa and Yuanhang Yu. Their research shows the real fear to overcome should be Britain’s lack of productivity-enhancing robots, software, artificial intelligence and other technologies.

| #LSEUKEconomy |

|---|

Worries that jobs will be lost to automation are not new but have been heightened since a seminal study in 2013 warned that nearly half (47%) of jobs in the United States were at “high risk” of automation. Nearly a decade on, we look at both the current and longer-term picture of the relationship between technology, jobs and pay.

We make two observations. First the period since the 2013 Carl Frey and Michael Osborne study has been one of rising rather than falling employment. In the four decades to the 2000s, the UK’s employment rate tended to peak at around 73%; on the eve of the Covid-19 pandemic, it reached 76%. Second, it’s also the case that even some of the jobs considered by Frey and Osborne to be at highest risk of automation, such as car washers and kitchen assistants, have grown fast in this period. Alongside high employment, productivity and real wages have stagnated. On the face of it, this is not a picture that fits well with concerns about the loss of jobs to technology.

But of course, job destruction was only ever half of the story. Automation doesn’t just destroy jobs, it can also raise demand for other workers, and create the space for entirely new jobs. Consistent with this, we have evidence that exposure to automation has affected the cross-section of employment growth in the UK – both in the last decade but also in the longer term. This is consistent with what is now a wide body of international evidence pointing to the importance of automation for wage determination.

So, automation is affecting jobs. But the fact that aggregate employment continues to grow alongside these effects suggests automation’s job-destroying impact continues to be offset by positive indirect effects.

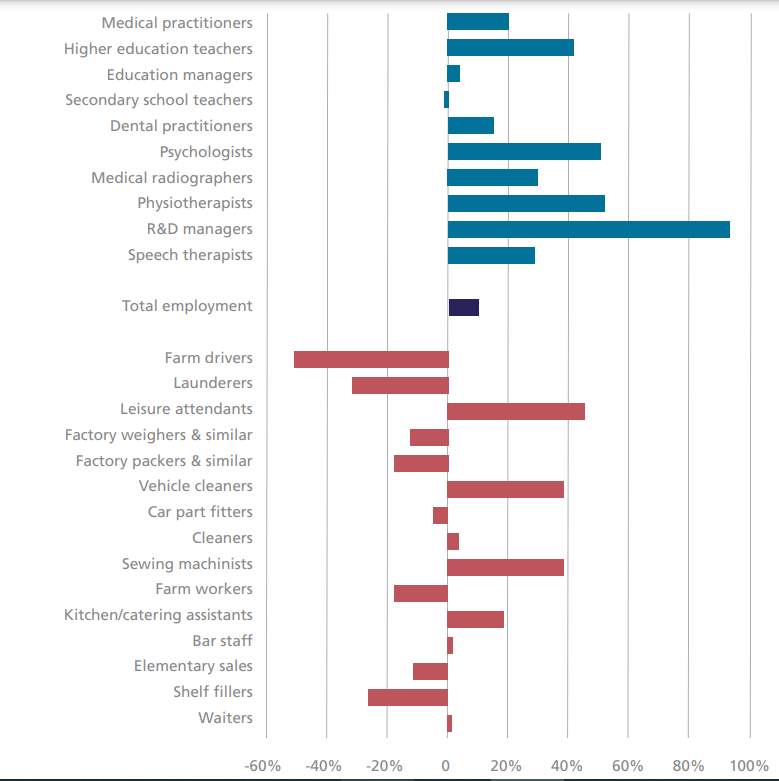

In Figure 1, we show employment growth from 2013 to 2019 for the occupations which, according to automobility probabilities produced by the Office for National Statistics and the Organisation for Economic Co-operation and Development based on the Frey and Osborne study, were at highest and lowest risk of automation. There is some vindication for Frey and Osborne: generally speaking, the occupations with low risk (in blue – including doctors and teachers) have seen stronger employment growth than the occupations with highest risk of automation (the occupations in red – including farm drivers or shelf fillers). But there are important exemptions to this pattern. Some “high risk” occupations have seen strong employment growth – including leisure attendants and kitchen assistants.

Figure 1. Some occupations considered by Frey and Osborne to have the highest risk of automation have grown in size since their report in 2013

Notes: Occupations ordered by automatability score: lowest (top) to highest (bottom). Scores are taken from an ONS database, which maps Frey/Osborne automatability scores to UK occupations. Source: Employment data from analysis of LNS, ONS. Automatability scores are from ONS, derived from Frey/Osborne, published in the article: ONS, Which occupations are at highest risk of being automated?, July 2019. Used in the Economy 2030 report Adopt, Adapt and Improve, Nov 2022.

We also look at data spanning the last four decades, and set out how – at the level of different occupations and places – the adoption of and exposure to automation has shaped the UK labour market.

A clear pattern emerges when looking at the exposure to different technologies across pay percentiles: workers in lower-paid occupations have historically been more exposed to robot advancements, those in the middle of the pay distribution have seen software innovations being able to perform part of their tasks and higher earners may start to see some of their work being automated by artificial intelligence.

Higher robot exposure has been associated with worse employment and wage performance. On average over the last 40 years, the jobs most highly exposed to robotisation have experienced wage growth 10 percentage points lower than jobs with low exposure, and have seen employment fall (by roughly 50% on average), while jobs with the lowest exposure have seen employment grow by a similar amount.

Similar to workers exposed to robotic advancements, individuals working in occupations highly exposed to software technologies have seen slower employment growth over the last four decades. But the relation with respect to wage growth is less clear. It is too early to make an assessment of the effects of artificial intelligence on the economy and labour markets.

Automation doesn’t just destroy jobs: it can also raise demand for other workers; and create the space for entirely new jobs

While increased automation does present risks, it also presents opportunities for growth and rising living standards. Industries with higher rates of robot adoption, such as the automotive sector, have seen higher productivity gains than those with lower rates, such as metal production. Between 1995 and 2019, an industry with one additional robot per thousand workers experienced 3% faster productivity growth on average.

We find both negative and positive effects stemming from the adoption of new technologies, albeit unequally distributed across workers contingent on their occupation and industry. The focus for policymakers should not be to stop or prevent technological advancements that strongly contribute to create desirable increases in added value and productivity. Instead, the policy conversation should be directed at how best to prepare and retrain workers at risk of being adversely affected by automation technologies. A careful investigation of the effects of automation on workers, households and firms is required, for the formulation of efficient policies which minimise negative displacement effects of technology and ensure that gains in productivity and from reinstatement are more equally spread.

Overall, while we must remain vigilant to the impact of automation, especially since it affects some people and places more than others, the most pressing problems facing the UK economy are not too much automation, but low investment and low productivity growth. We should worry more about these and less about robots taking our jobs.

♣♣♣

Notes:

- This blog post appeared first at CentrePiece, the magazine of LSE’s Centre for Economic Performance (CEP). The research is part of the Economy 2030 Inquiry by the Resolution Foundation and CEP, funded by the Nuffield Foundation.

- The post represents the views of its author(s), not the position of LSE Business Review or the London School of Economics.

- Featured image by Testalize.me on Unsplash

- When you leave a comment, you’re agreeing to our Comment Policy.