In May 2011 Portugal negotiated an IMF-EU bailout package of 78 billion euros, designed to help the country stabilise its finances. In return Portugal agreed to implement a number of reforms, with a target to reduce its budget deficit to 2.5 per cent by 2014. Paulo Trigo Pereira assesses the country’s progress over the last two years, and suggests some new measures to aid the recovery. He argues that the troika should consider decreasing the interest rates and extending maturity dates on its loans to Portugal.

In May 2011 Portugal negotiated an IMF-EU bailout package of 78 billion euros, designed to help the country stabilise its finances. In return Portugal agreed to implement a number of reforms, with a target to reduce its budget deficit to 2.5 per cent by 2014. Paulo Trigo Pereira assesses the country’s progress over the last two years, and suggests some new measures to aid the recovery. He argues that the troika should consider decreasing the interest rates and extending maturity dates on its loans to Portugal.

The idea that any country can change its economic structure, its budgetary framework, its budgetary culture, and its institutions within the short period of an adjustment programme (typically three or four years) is simply unrealistic. It is not possible to correct the errors of past decades in a couple of years and this will not happen. The right perspective to look at a bailout adjustment programme is that it is the beginning of a ten year process of reform, which includes fiscal consolidation, economic structural reform and institutional reform (including constitutional) in order to guarantee the long term sustainability of public finances. However, it is necessary to combine economic and institutional reform with democratic legitimacy. This needs consensus building across political parties. One lesson of the Italian election is that it is not enough to do the right things: it is essential that citizens also understand them and start seeing some light at the end of the tunnel.

Nearly two years on from its bailout, and in the week that the EU’s finance ministers gathered to discuss it, now is an apt time to take stock of Portugal’s adjustment programme and the progress that has been made in the country, while also addressing what may be unrealistic projections for the future. There is a need to revise the adjustment programme and clarify the role of the European Central Bank (ECB) in the short term, although in the medium term this will not be enough. Portugal also needs domestic changes, as well as a stronger, more federal European Political Union, with economic governance, and a Treasury and budget directed towards the people who are suffering from adjustment policies.

Some key facts about Portugal

Portugal has never had a fiscal surplus since its transition to democracy in 1974, which is quite unique among European countries. This simple fact shows that, until quite recently, there has been a political culture which dictated that deficits do not matter. In February 2013, the Portuguese Parliament approved changes in the Budget Framework Law (BFL) in order to introduce the provisions of the “Fiscal Compact”. However, the BFL is not a Law requiring a supermajority to be changed, so it is not as stable as it should be.

In May 2011 the then socialist government approved a bailout programme of €78 billion (of which €12 billion was for bank recapitalisation) with the acquiescence of opposition right wing parties. In June, elections put the socialists out of power and a new government was elected. Therefore, we have now had 21 months of the bailout adjustment programme and we can look at some data.

The current sixth revision of the programme establishes a consolidation path of reducing the public deficit from 9.8 per cent of GDP in 2010, to 5.9 per cent in 2011, 5 per cent in 2012, 4.5 per cent in 2013, and 2.5 per cent in 2014. The target for 2011 was achieved (a deficit of 4.4 per cent) through extraordinary revenues. The target for 2012 may not be reached, even with extraordinary revenue (accounting for 0.5 per cent of GDP) that the government has considered, but EUROSTAT may not accept to register (the privatisation of ANA, Aeroportos de Portugal). Missing the fiscal target in 2012 is down to an over-evaluation of fiscal revenues, particularly VAT. All major fiscal revenues were below the budget estimates and the deviation was around €3 billion, or 1.8 per cent of GDP. This was a result, on the one hand, of a higher than expected contraction of consumption and imports, and on the other hand of gross miscalculations within the Ministry of Finance.

As expected, a pro-cyclical fiscal policy had a negative effect on economic growth and employment. The real variation of GDP was a fall of 1.6 per cent in 2011, and a fall of 3.2 per cent in 2012. Austerity measures lead to a collapse in domestic demand, which was compensated for by positive developments in net external demand in the last quarter of 2011 and half of 2012. Unemployment has been rising from 12.9 per cent in 2010 to an expected 17.6 per cent, particularly among younger citizens, and public debt has reached 120 per cent of GDP.

The main positive short term economic consequences of the adjustment programme are twofold. The current account balance which was highly in deficit in the past is now almost balanced (-0.2 per cent of GDP in 2012). Also, the public corporations, which are considered within general government, are improving their economic results. Finally, at the start of this year Portugal went to the capital markets to borrow €2.5 billion with a medium term maturity (5 years) for the first time since the beginning of the adjustment programme. This was a relative success. Some credit must be given to the government’s strong commitment to fiscal consolidation, but a considerable part of the credit should also be attributed to the President of the ECB, Mario Draghi .

What lies ahead?

What lies ahead depends as much on Portugal as it depends on the evolution of the European Economy and the actions of the European Commission, the ECB and the IMF (the troika). But one thing is sure, the period 2013-2016 will not be easy, and Europe and Portugal are still some distance away from overcoming the current crisis. Last autumn the government and the troika forecasted a recession of 1 per cent for 2013. At the same time a panel of independent economists predicted a recession no smaller than 2 per cent.

The Bank of Portugal has since revised its growth forecasts down (now to a fall of 1.9 per cent) and in February 2013 the Portuguese government and the European Commission endorsed this forecast. The continuation of the recession into 2013 has been caused by a combination of : i) the recession in other Eurozone countries, which are the main export markets of Portugal; ii) relatively adverse financial conditions (the Portuguese Government borrowed €1.155 billion for 12 months at 1.27 per cent, while Germany on the same day (20/02/13) borrowed at 1.66 per cent for 10 year bonds); iii) relative high taxes when compared with Eastern European countries; and iv) the continuation of pro-cyclical and unstable fiscal policies.

Portugal has to do its part by following a consolidation path and taking measures to promote growth and employment. One example of the wrong type of measure is the application of the top VAT rate to restaurants, which led to small restaurants facing bankruptcy, decreased employment and in all likelihood a fall in VAT revenues. On the other hand the renegotiation of public-private partnership (PPPs), which the government has started, but without much success, should be a priority. Over this period, Portugal will have its peak expenditures on PPPs (€1.5 billion in 2014), which will surpass 1 billion euros per annum until 2019.

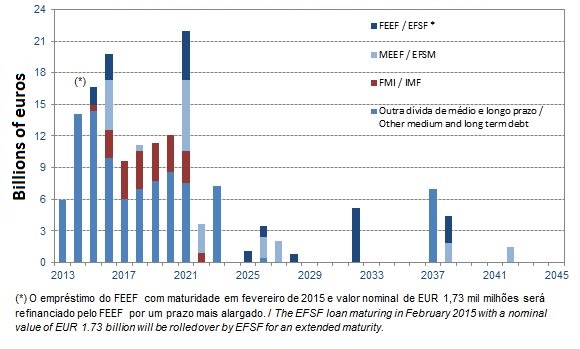

The “troika” also has to help, particularly by extending the maturities of loans and decreasing interest rates. Figure 1 illustrates the huge borrowing requirements of Portugal in the forthcoming years (€48.8 billion in three years – 2014-16 – excluding the rollover of European Financial Stability Facility (EFSF) funds in 2015). An extension of maturities of long term debt is essential and a decreasing of interest rates and commissions also seems urgent. This week (5th March) the ECOFIN Ministers “discussed whether EU Finance Ministers would be ready in principle to consider an adjustment of the maturities on the EFSF and EFSM loans to Ireland and Portugal in order to smooth the debt redemption profiles of both countries.” The fiscal target for 2014 and 2015 should also be somewhat relaxed. It is simply not possible to get a 2.5 per cent deficit in 2014 without a deep recessive impact. Even a 3 per cent target will be difficult to achieve.

Figure 1: Portugal’s Medium and Long Term Debt

Source: IGCP- Portuguese Treasury and Debt Management Agency

A recent study from a large private bank (BPI) has indicated that the EFSF is borrowing at an average rate of 1.5 per cent and charging Portugal 3 per cent. This means that there is some room for maneuver to decrease interest rates of the EFSF and EFSM to say 1.9 per cent or 2 per cent. This would be much more beneficial than an extension of maturities (and should complement that measure). Unless there is some decrease in interest rates, or the restrictive fiscal policy, the situation will continue to depress domestic demand, aggravating recession and promoting social unrest. The austerity measures adopted in 2012, and the large increase in taxes in 2013, are eroding social support for the adjustment programme.

It is likely that the EU Finance Ministers and the troika will agree on extending maturities an extra year for the excessive deficit to be corrected. But this will not be enough. If debt interest rates do not go down, the amount of expenditure cuts will be of sufficient magnitude to depress the economy even further. Therefore, in order to facilitate access to capital markets, and decrease interest rates, the ECB should clarify the conditions under which it will launch the Outright Monetary Transactions in countries like Ireland and Portugal.

Large demonstrations in 18 cities (about half a million in Lisbon) on March 2nd illustrate that Europe and the troika should recognise the efforts that are being made by Portuguese citizens, and should acknowledge that they have made overly optimistic forecasts on the deficit, debt, growth, and employment. The effects of austerity are much larger than those anticipated by the troika. On the other hand, the Portuguese government should be much more innovative and creative in measures that promote employment, exports and economic growth. Unless sufficient measures are put in place at the European and domestic levels, Portugal will see a progressive decline of its economic base and will not be capable of regaining economic growth, employment creation and full access to capital markets.

These are the “small things” that have to be done in the short term. In the medium and long term either Europe progresses decidedly towards further political integration with the countries that want to move forward, and based on a common sense of solidarity among the peoples of Europe, or the euro, as it exists today, will collapse. The European Commission cannot be seen to be the ‘bad guys’ who, with the IMF and ECB, implement austerity measures that lead to unemployment and poverty for hundreds of thousands of citizens in peripheral countries, and keep youth unemployment high. It also must show, not in words but in practical terms, the meaning of solidarity: or what Adam Smith called “sympathy”. This can be done with economic governance, with a Treasury, and a budget that assumes, at a Union level, some of the redistribution allowances of the Member States, targeted to youth employment and elderly poverty, and not just to farmers.

If Europe shows its human face, and makes progress towards reforming the treaties, it may win the support of European citizens and have democratic legitimacy for further political integration. If not, it will be impossible to sustain fragile coalitions that still support austerity measures in peripheral countries. We are still far away from solving the euro crisis, but this is a complementary story…

Please read our comments policy before commenting.

Note: This article gives the views of the author, and not the position of EUROPP – European Politics and Policy, nor of the London School of Economics.

Shortened URL for this post: http://bit.ly/10bjEaY

_________________________________

Paulo Trigo Pereira – Technical University of Lisbon

Paulo Trigo Pereira is a Professor at the Economic and Business Management Faculty (ISEG) of the Technical University of Lisbon. He has been chairing the Master of Public Policy and the Public Finance Courses at ISEG, with several books on Portuguese Public Finance and Institutional Economics, and research published in public and social choice. His research interests are public finance, public choice and electoral institutions. He leads civil society projects on Budget Transparency in Portugal (Open Budget Survey, and Budget Watch) and is a regular columnist for Portuguese newspaper “O Público”.

1 Comments