Although debt restructuring and austerity have defined the debate on Greece and the Eurozone crisis, the role of structural reforms has been less well-understood. Nauro Campos and Fabrizio Coricelli write that this is partly because analysing structural reforms is only possible through a re-examination of the relationship between the EU and Greece, which requires robust ‘counterfactuals’. Presenting evidence from a detailed study of the effect of EU accession on current member states, they write that Greece is the only country that has experienced negative growth as a result of its EU membership, but that this negative effect also shrank after 1995. They argue that structural reforms may offer one explanation for this successful shift.

Although debt restructuring and austerity have defined the debate on Greece and the Eurozone crisis, the role of structural reforms has been less well-understood. Nauro Campos and Fabrizio Coricelli write that this is partly because analysing structural reforms is only possible through a re-examination of the relationship between the EU and Greece, which requires robust ‘counterfactuals’. Presenting evidence from a detailed study of the effect of EU accession on current member states, they write that Greece is the only country that has experienced negative growth as a result of its EU membership, but that this negative effect also shrank after 1995. They argue that structural reforms may offer one explanation for this successful shift.

There is an interesting imbalance in the current debate about Greece and the Eurozone crisis. On the one hand, regarding debt and austerity, there are strong theoretical foundations and a broad empirical consensus within academia. On the other, there are structural reforms. We are far from a full understanding of how reforms evolve, fit, and can hopefully help solving the crisis and, in the case of Greece, this task starts with a re-examination of the EU-Greece relationship that requires counterfactuals.

Did Greece benefit from joining the EEC?

Greece joined the European Communities in 1981. The EU-Greece relationship is one of the most politically charged in the history of European integration. In 1974, Turkey invaded Cyprus and the Greek military dictatorship collapsed. One of the main ideas of the Karamanlis Premiership (1974-1980) was to diplomatically convince Europe to allow the “cradle of democracy” to join as soon as possible.

Karamanlis succeeded, but barely. In 1976 the Council of Ministers (unusually) rejected the European Commission’s Opinion which favoured delaying entry until Greek producers were able to compete in the Common Market. This shows awareness of the competitiveness problem facing Greek firms. Yet it was not deemed strong enough a reason to delay membership. The diplomatic lobbying was highly effective and Greece joined five years ahead of Spain and Portugal. It joined despite French worries (agriculture) and German concerns (migration). Considering the few agreed “transition periods”, it is fair to say Germany played a key role in Greece’s early entry.

Did Greece benefit from joining early? This is an important yet difficult question. One way to address it is to conjure counterfactual scenarios. If we could agree on what would have happened if Greece had not joined, then we can compare and contrast it with what actually happened. The direction (sign) and size of the eventual difference would provide valuable information.

We, along with our co-author Luigi Moretti, have previously assessed the level of per capita GDP and productivity that would have existed in Greece if it had not joined the EEC in 1981. We estimated similar counterfactuals for all countries that joined the EU in the 1973, 1980s and 1995 enlargements, and for 8 of the 10 that joined in 2004.

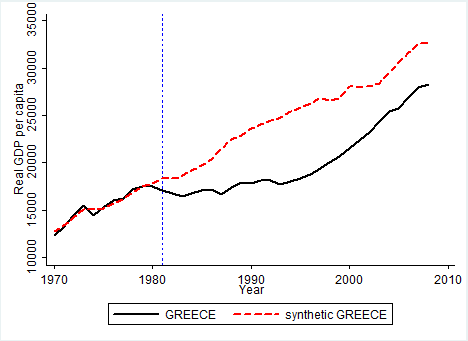

The statistical methodology adopted (the “synthetic control method”) selects the optimal weighted combination of countries from a “donor pool” that better mimic the behaviour of the target country (Greece) in the pre-shock period (in this case, the period before joining, that is, before 1981). This hypothetical or synthetic Greece is constructed as being 49 per cent Japan, 28 per cent Australia, 14 per cent Brazil and 9 per cent Tunisia (the percentages are the estimated weights, the four countries are those statistically selected from the broader donor pool). The results of this calculation are shown in the figure below.

Figure: Estimated per capita GDP of Greece if it had not entered the European Economic Community in 1981

Note: The estimate for Greece if it had not entered the EEC is indicated by the dotted line (‘synthetic Greece’), while the solid black line indicates the actual per capita GDP that Greece experienced. The vertical blue dotted line marks 1981: the year in which Greece joined the EEC.

The effects from EU membership this analysis uncovers for all EU countries are large, significant and almost unanimously positive. EU membership caused an increase in per capita incomes in EU states of about 12 per cent in the first ten years after accession. Yet, for only one country (out of 17) there is a negative effect of EU membership. That country is Greece. The analysis suggests that Greece’s per capita GDP would have been higher if it had not become a full-fledged EU member in 1981.

The figure shows how the behaviour of these net benefits changes over time. There seem to be two different regimes. Regime 1 lasts from 1981 until approximately 1995. During this period the gap between the actual and hypothetical Greek per capita GDP increased. This means that Greece until 1995 would have increasingly benefited more and more from not joining.

Regime 2 starts in 1995. The gap decreases and is on its way to closing until the 2007 crisis. After 1995 the Greek economy progressively benefited from joining, thus making non-membership increasingly unattractive. Does this imply Greece would have been better off leaving the euro and the EU? Surely not. It suggests instead that the broadening and deepening of structural reforms was delayed until about 1995.

From 1981 to 1995 growth rates in the EU were relatively high and Greece experienced divergence. Yet, our results are deeper: in this regime, Greece lost by joining. The opening up of uncompetitive industry was too early and the Commission’s Opinion about Greek traditional agriculture and highly protected manufacturing seems to have been vindicated. In this period, unchecked regulation was allowed to flourish and take root. It extended to various industries and professions making Greece one of the most expensive and cumbersome countries in which “to do business” in Europe.

Yet things change around 1995. The entry process into the economic and monetary union prompted growth rates faster than in the EU for 1995-2010, but the results show a deeper causal effect: now, Greece seemed increasingly better off inside. The main explanations for this turnaround are competitiveness improvements in selected industries (such as tourism and telecommunications, both non-tradables) and reforms in the financial sector. The effects of such limited financial reforms were amplified by growing financial (and political) integration in Europe, which ultimately may have helped shore up this convergence process.

With the onset of the debt crisis, many observers jumped to the conclusion that the crisis revealed Greece was “living beyond its means” and that the pre-crisis growth was nothing but an unsustainable boom. Notwithstanding the data corrections, the OECD “Going for Growth 2015” estimates that during 2000-2012 Greece was one of the countries that benefited the most from structural reforms. This is consistent with Regime 2 above, the period of accession to the euro. The same report indicates that in the crisis years (2007-2014) Greece was a frontrunner in structural reforms.

Yet the subject of structural reforms in Greece requires two further caveats. One is that restricted financial reform is intertwined with “partial democracy” and state capture, thus explaining the persistence of (elites’) rent-seeking behaviour. The second is that we still know much less about the causes and consequences of reforms than about debt or stabilisation. The limited lessons from the greatest experiment in this regard (the transition from communism) should encourage analysts to be more humble.

In short, Greece was always exceptional in Europe. Its entry in the EU owes more to political lobbying than to economic preparedness. A period of relative stagnation lasted until the conditionality for euro membership was laid bare. The oft-heard notion that “Greece was bad for the euro” has much less empirical support than the idea that the euro was good for Greece. By prompting structural reforms it may have helped open the way for a Greek turning point in Europe. That is, at least until the crisis hit.

Please read our comments policy before commenting.

Note: This article gives the views of the authors, and not the position of EUROPP – European Politics and Policy, nor of the London School of Economics. Featured image credit: Wayne Lam (CC-BY-SA-3.0)

Shortened URL for this post: http://bit.ly/1C1gTK0

_________________________________

Nauro Campos – Brunel University London

Nauro Campos is Professor of Economics and Finance at Brunel University London. He is also affiliated with ETH Zurich and IZA-Bonn.

–

Fabrizio Coricelli – Paris School of Economics

Fabrizio Coricelli is Professor of Economics at the Paris School of Economics. He is also affiliated withCEPR-London.