The Italian government will present its public finance projections by 10 April. Lorenzo Codogno writes that fiscal policy is expected to be strongly expansionary in 2016, but courtesy of flexibility clauses, the government will likely avoid entering into the EU’s so called ‘Excessive Deficit Procedure’ in May. He argues however that a fiscal problem looms large in 2017, while Italy’s reduction of its debt-to-GDP ratio remains fragile and subject to external shocks.

The Italian government will present its public finance projections by 10 April. Lorenzo Codogno writes that fiscal policy is expected to be strongly expansionary in 2016, but courtesy of flexibility clauses, the government will likely avoid entering into the EU’s so called ‘Excessive Deficit Procedure’ in May. He argues however that a fiscal problem looms large in 2017, while Italy’s reduction of its debt-to-GDP ratio remains fragile and subject to external shocks.

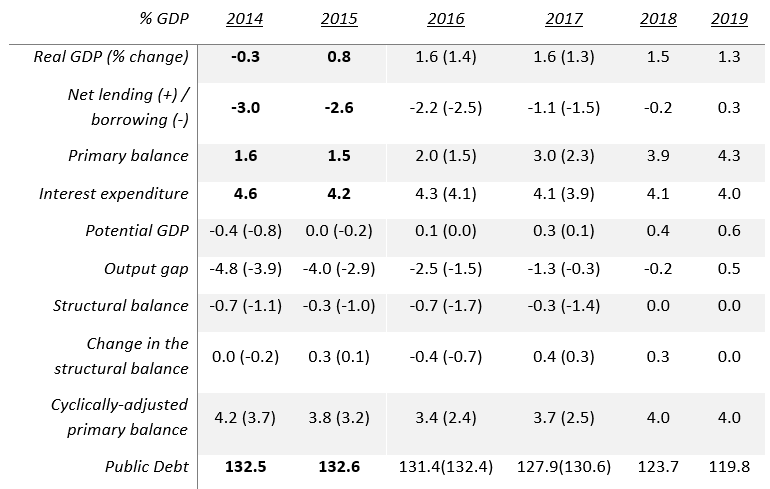

By 10 April, the Italian government will unveil its budgetary projections (Economic and Financial Document – the DEF – which includes the Stability Programme to be delivered to Brussels). It will indicate new projections for economic growth and public finances and will set the stage for the preparation of the Budget to be delivered in October. Table 1 shows the key figures the government presented back in September 2015 and, in brackets, the European Commission Winter forecasts.

Table 1: Italy’s key macroeconomic and public finance projections

Note: Projections from the Update to the Economic and Financial Document presented on 18 September 2015 and, in brackets, European Commission Winter Forecasts; in bold actual or preliminary figures. Structural balance is cyclically-adjusted and net of one-offs. Cyclically-adjusted primary balance is gross of support to other Eurozone countries and payment in arrears of the public administration.

The government also asked for an extra 0.2pp of GDP flexibility to deal with the migration crisis, which is not included in the September projections; otherwise, the net borrowing for 2016 would have moved from 2.2% to 2.4% of GDP. Please note that estimates of potential growth, output gap, and the structural balance tend to fluctuate widely, as can be seen in the table (Italian government vs Commission using the same methodology), but compliance with EU fiscal rules will be checked exclusively against the European Commission’s Spring Forecasts to be published on 4 May 2016.

Key forecast revisions: will they matter?

Back in September 2015, the government projected GDP growth at 1.6% in both 2016 and 2017. In February, the European Commission’s more recent Winter Forecasts projected 1.4% and 1.3% respectively. Given the soft 2015 ending (i.e. 0.1% quarter on quarter), which led to a lower carry-over into 2016 (0.2%), and a likely slight downward revision in exogenous variables, the European Commission’s projections will likely be around 1.1%, or even 1.0%, for 2016 and possibly a bit stronger for 2017 (1.2-1.3%).

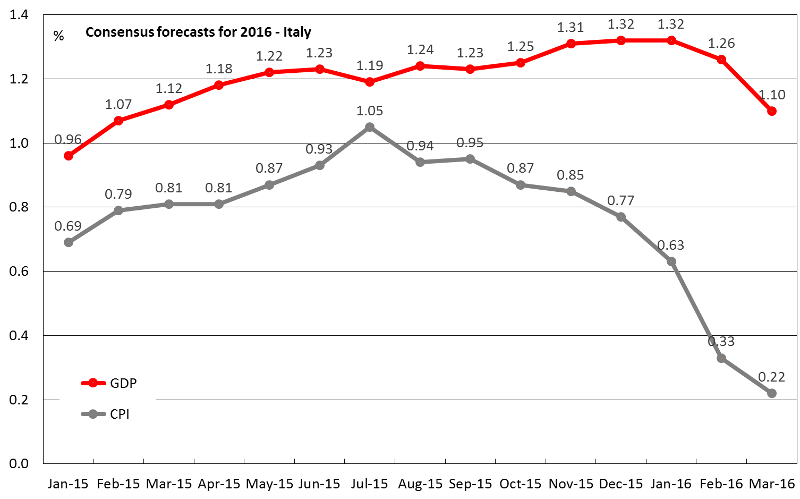

Government projections are going to be slightly more positive (my guess is 1.2% and 1.4% respectively). In March, Consensus Forecasts called for GDP growth at 1.1% in 2016 (see Figure 1) and 1.3% in 2017. There is probably some upside potential for 2016 linked to a likely rebound in 1Q16 GDP, and I would not be surprised to see a better outcome (1.4%), but there are also downside risks related to the global scenario.

Figure 1: Italy’s GDP projections for 2016 (Consensus Forecasts)

Source:Consensus Forecasts 7 March 2016

2016: the government is likely to get the go-ahead from Brussels

Italy will likely manage to avoid the Excessive Deficit Procedure in 2016. The decision is due by the end of May based on Commission forecasts to be published on 4 May. Let me briefly highlight why this is likely to be the case.

In July 2015, the European Council already approved flexibility for structural reforms by reducing the required structural adjustment for 2016 to 0.1pp of GDP. On top of that, the government asked for another 0.1pp in September (to make for 0.5pp, the maximum allowed for structural reforms) and 0.3pp for public investments. Another 0.2pp was added off the cuff, not included in baseline projections, for extra costs linked to the immigration crisis (as it would be a one-off, this extra flexibility would not change the required structural adjustment). Stretching flexibility to the limits, the Italian government presented projections that called for a worsening of the structural balance by 0.4pp in 2016, and then a gradual adjustment thereafter (0.4pp in 2017 and 0.3pp in 2018 in structural terms), writing in official documents that it would be “counterproductive” to do anything more.

Back in September, there was still uncertainty as to whether flexibility clauses could add up, i.e., flexibility for reforms, plus those for investments and possibly for the immigration crisis. At the time, the prevailing interpretation was indeed that they could add up. The Commission Communication of 13 January 2015 on flexibility within the Stability and Growth Pact said that “under the preventive arm of the Pact, some investments deemed to be equivalent to major structural reforms may, under certain conditions, justify a temporary deviation from the MTO of the concerned Member State from the adjustment path towards it”.

The General Secretariat of the Council published a note on “Commonly agreed position on Flexibility in the Stability and Growth Pact” on 30 November 2015, which presented the position agreed upon at the Economic and Financial Committee, the junior Committee of Ecofin, as a result of discussions on the operationalisation of the Commission Communication. The document clarified how three specific policy dimensions can best be taken into account when applying rules: (i) cyclical conditions; (ii) structural reforms; and (iii) “government investments aiming at, ancillary to, and economically equivalent to major structural reforms”.

The note indicated what types of reforms would qualify for budget flexibility and that they have to be “major”, have “long-term positive budgetary effects” and be “fully implemented”. Italy’s reforms should not have problems qualifying, although arguments need to be fully spelled out in the forthcoming DEF. Flexibility is granted provided that: (i) the reforms meet the criteria, (ii) the temporary deviation does not exceed 0.5% of GDP, (iii) the cumulative temporary deviation granted under the structural reform clause and the investment clause does not exceed 0.75% of GDP, effectively putting a ceiling on possible flexibility.

Moreover, flexibility can be allowed only if the output gap is greater than 1.5% in the year of application, i.e., 2016 for Italy. Italy would be a borderline case as the Winter Forecasts of the Commission show 1.5%. Still, with a small downward revision in GDP projections for the current year (and possibly a marginal increase in potential growth following technical discussions on the lengthening of the forecast horizon), Italy should make it.

Finally, flexibility is conditional on Italy’s pursuit of structural balances leading to the MTO within the time horizon of the Stability Programme. In the Commission opinion on Italy’s Draft Budgetary Plan published on 16 November 2015, Italy was considered “at risk of non-compliance with the requirements for 2016 under the SGP. [Italy’s Budgetary Plan] might result in a significant deviation from the adjustment paths towards the Medium-Term Objective (MTO).”

Assuming that all the above (and other things I have not mentioned) are respected, Italy’s structural balance would still be allowed to deteriorate by only 0.25pp in 2016, while the Winter Forecasts of the Commission would call for an increase of the structural deficit by 0.7pp. As there is a margin (“significant deviation”) in the Commission assessment of 0.25%, this leaves a gap of 0.2pp, barring no major changes due to the lower economic projections.

This gap matches press leaks related to an additional fiscal correction the Commission requested from the Italian government for the current year. The government has already said that it will use “administrative measures” instead of a supplementary budget to close the gap, with some extra savings on interest expenditures, unused funds already allotted, voluntary disclosure, and so on. The bottom line is that Italy will likely make it, but only just. The final decision will be made by the end of May.

2017: a high mountain to climb

To be fair, I have never seen an easy year in my nine years at the Italian Treasury and 2017 will be no easier than in the past. It is no wonder that Italy is trying to team up with other countries to ask for a revision of the methodology for estimating potential growth and the output gap, which would provide some extra leeway.

According to the more recent Winter Forecasts of the Commission, the output gap for 2017 was estimated at -0.3%, requiring a structural correction of more than 0.5, i.e., at least 0.6pp (see Figure 2). The fiscal adjustment required for 2017 will be frozen once the 2016 Spring Forecasts (t-1) are out. As it appears likely that the estimated output gap will be smaller than 1.5, the required structural adjustment will definitely be 0.6pp. Any possible methodology revision, including a potential lengthening of the forecast horizon, is unlikely to close such a gap, even assuming it becomes effective immediately, in time for the Spring Forecasts.

On top of this required adjustment, the government needs to repeal a previously legislated VAT hike – a safeguard clause automatically increasing VAT should adequate spending cuts not be legislated. This was a way to make the commitment credible, allowing deficit projections to include the results and thus respect fiscal rules. These safeguard clauses amount to 15.1bn, i.e., 0.9% of GDP for 2016 (4.4bn for 2018), and should ideally be addressed only through spending cuts.

My back-of-the-envelope estimate of budgetary measures required for 2017 to comply with fiscal rules call for 0.3/0.4pp of GDP in extra structural adjustment to reach the required 0.6pp correction. Including safeguard clauses, this makes for a gap of about 1.2/1.3% of GDP that needs to be financed in October. Finally, the Prime Minister has made yet-to-be-financed promises to reduce taxation and introduce a €500 bonus for young people. The reduction of IRAP, the local tax for companies, is already financed but nothing else is. It is difficult to estimate how much the total bill will be.

In the past, some of the spending cuts were set aside. Tax expenditure in particular proved to be a very difficult political subject. It is not clear whether the government will promise to reduce tax expenditures in the next Budget to help finance the large fiscal gap. It seems encouraging that it set up a working group tasked with delivering proposals for the Budget, although I am somewhat suspicious of working groups when the problem is political. As an example, reducing tax expenditures would imply eliminating tax benefits on fuel for lorry drivers, tax benefits for agriculture, and subsidies for newspapers, which are all very touchy political issues.

The Italian government will try to do whatever it can to reduce the overall structural adjustment in 2017, but flexibility clauses can no longer be invoked. The mentioned note by the General Secretariat of the Council says that “the application of the structural reform clause is restricted to a single time per period of adjustment towards the MTO, i.e., Italy will not be allowed to benefit from the clause again until it has attained its MTO. This provision is not designed to restrict structural reforms, of course, but to keep the MTO from becoming a moving target.

Italy should move from a Commission-estimated structural deficit of 1.7% (likely to become 1.5%) to 0.0% within the timeframe of the Stability Programme. This effectively means that Italy should reduce its structural deficit from 1.7% to 1.5% for the current year (as required by the Commission and leaked in newspapers) and that the targets for the following years should be 0.9%, 0.3%, and 0.0%, decreasing by 0.6pp per year until MTO is met.

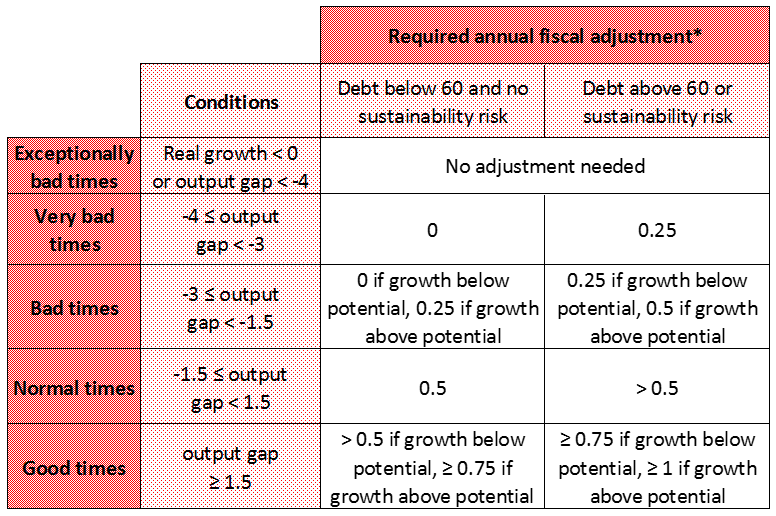

The matrix in Figure 2 specifies the fiscal adjustment requirements under the preventive arm of the Pact. The matrix is symmetric and aims at requiring larger fiscal efforts in better times and smaller fiscal efforts under difficult economic conditions.

Figure 2: Matrix for required annual fiscal adjustment in structural terms (% of GDP)

Source: General Secretariat of the Council, “Commonly agreed position on Flexibility in the Stability and Growth Pact”, 30 November 2015. “Sustainability risk” in the matrix refers to the medium-term overall debt sustainability as measured by the S1 indicator, among other information. S1 is defined as the adjustment effort required, in terms of steady improvement in the structural primary balance to be introduced until 2020 and then sustained for a decade, to bring the debt ratios to 60% of GDP in 2030, also taking into account the costs arising from an ageing population.

There is a crack in everything, that’s how the light gets in

Over the past couple of years, there has been a restless search for ‘cracks’ in the EU fiscal framework. Flexibility clauses, and relevant factors have been sought out to reduce the burden of adjustment and allow economic growth to strengthen, i.e., allow ‘light to get in’ after the dark period of deep fiscal consolidation between 2012-2014. Why does the Italian government strenuously oppose more fiscal consolidation?

The first reason is that, according to the Italian government, returning to a restrictive fiscal policy is wrong from an economic point of view. In a world suffering from aggregate demand deficiency, given the difficulty of central banks to do more to support it, fully enforcing European rules would risk derailing Italy’s feeble recovery. For example, spending cuts are important for reassessing the way in which the state provides services to citizens, but they have a high multiplier and negatively affect economic growth in the near term. In addition, the calls of the G20 and the European Central Bank for governments to “do their part” would seem to indicate the need for a different fiscal policy. True, structural reforms may at times be costly in the near term, but I do not think this was the main reason Italy searched for flexibility.

In September, the planning document included a review of the literature on fiscal multipliers. Spending cuts have the highest multiplier effect on the economy, and the underlying message was that reducing projected spending cuts would allow aggregate demand to strengthen. Flexibility is a way to smoothly reduce high-multiplier expenditures while somewhat reducing taxation at the same time.

Thinking that achieving a more accommodative fiscal stance should be the primary policy aim and that Italy can solve its structural problems with an expansionary fiscal policy as a facilitator for structural reforms may prove a big mistake. Countries that can afford it should definitely take a less restrictive or even expansionary policy to contribute to Euro Area aggregate demand, but Italy can only continue the consolidation process. Supporting domestic demand as the primary goal may even prolong the structural problems and pose a risk to financial stability.

There is also a second, more political objection. With the opposition increasingly radicalised, Eurosceptic and populist, Renzi seems to say (and perhaps rightly): “there is no alternative to my government”. To avoid any risk, Renzi has adopted an increasingly confrontational stance with Europe and a more populist stance in budgetary matters. There is no other justification for measures such as the famous “80 euro” to households, the recent abolition of the TASI (the recurrent taxation on first residencies) and the €500 cheque for Italian youth. Moreover, the government set aside some of the most thorny and delicate questions on the spending review, essentially all that could cause political and electoral damage in the short term.

Lobbies, vested interests, and rent-seekers form a hard amalgam to crack, even for a young, dynamic leader eager to deliver. Moreover, as often happens, pursuing the common good with reforms does not lead to immediate returns, not only in terms of growth and employment but also in electoral terms.

Can the debt-to-GDP ratio be reduced soon?

Reducing the very high debt-to-GDP ratio is very challenging for Italy, especially in a low-inflation environment and with the legacy of the crisis on the cost of servicing the debt.

In 2015, the Italian economy grew in real terms by 0.8% and 1.5% at current prices, with the latter being more important for the debt-to-GDP ratio dynamics. The result was driven by an unusually high GDP deflator (0.8%) compared to broadly flat consumer prices. The GDP deflator has in fact benefited from the collapse of the deflator of imports (-2.7%) due to the decline in prices of imported energy products. With this result and with net borrowing at 2.6% the debt-to-GDP ratio almost stabilised (132.6% compared to 132.5% the previous year).

In 2016, nominal GDP growth would likely be below last year’s result, assuming a flat deflator as the effect of declining oil prices is fading while the effect of monetary policy will take a while to do its magic (somewhat oddly, the Commission indicated 0.8% in February). The European Commission projects net borrowing at 2.5% for 2016. Even if the government reduces it to 2.3% with administrative measures, it would be difficult to project a debt-to-GDP ratio below last year’s levels. The reduction will likely start in 2017 and the following years but at a pace that leaves Italy exposed to a sudden increase in interest rates or an unexpected downturn in the global economy.

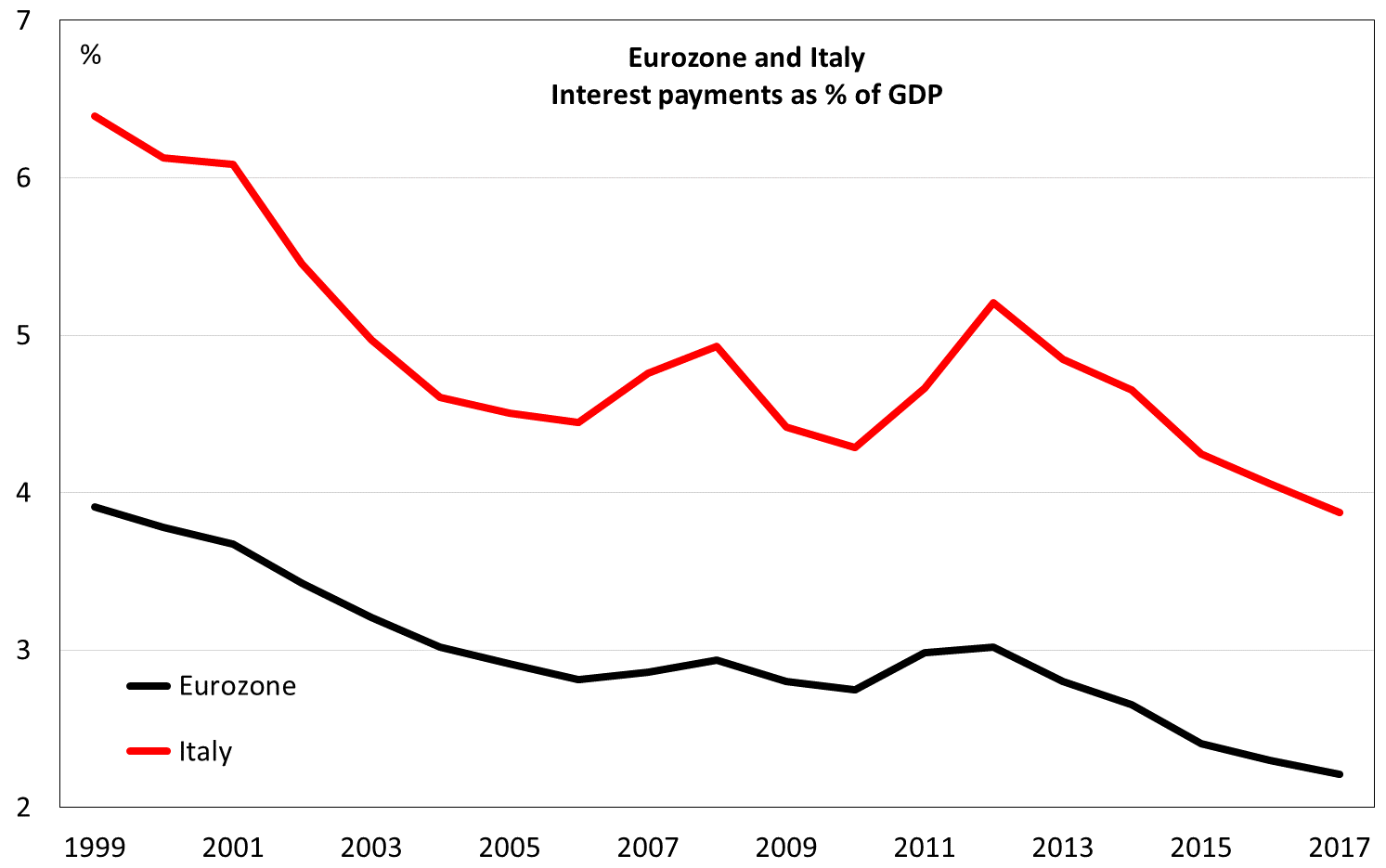

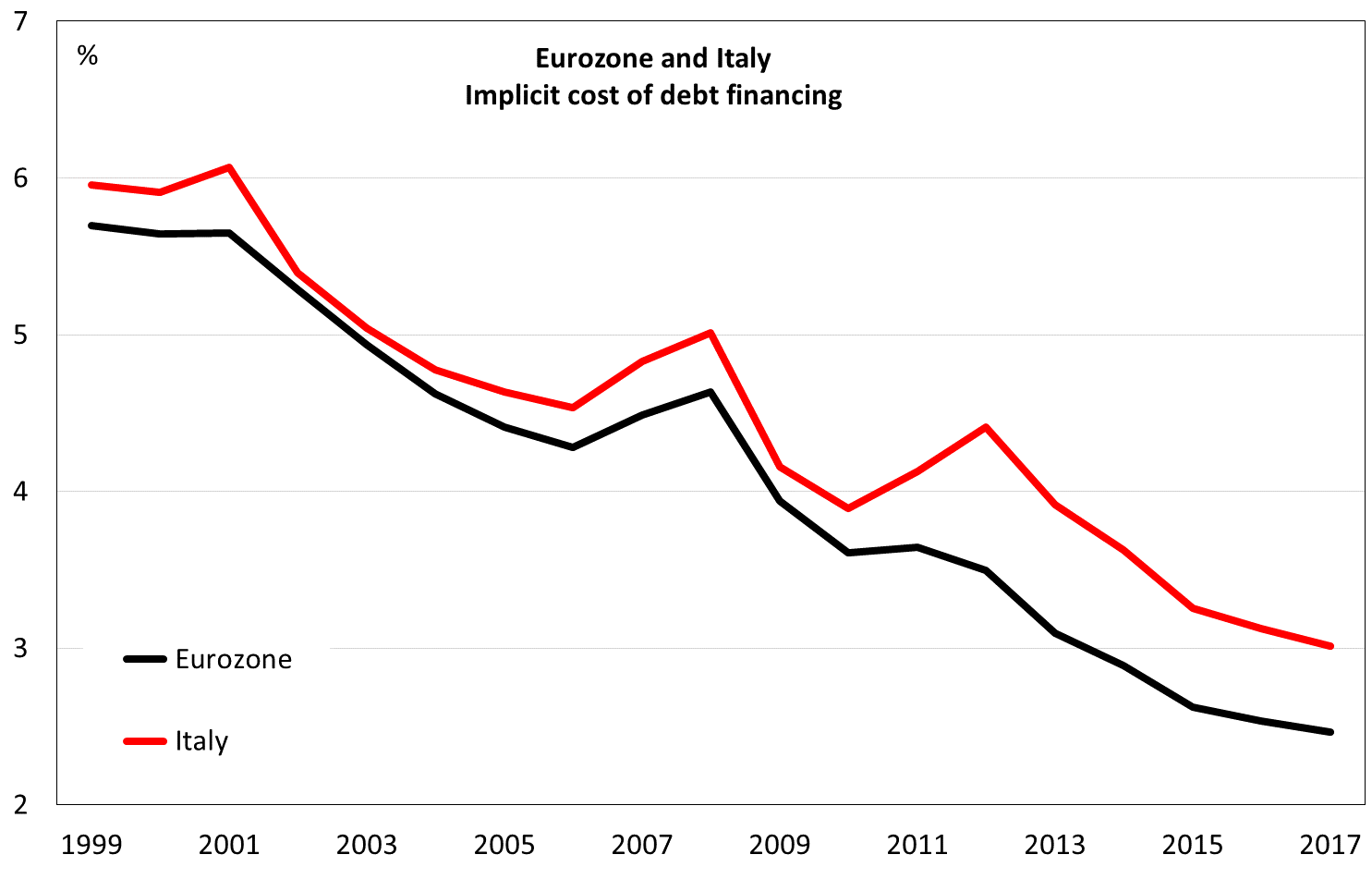

Interest expenditure still accounts for close to 4.0% of GDP, well above the Eurozone’s (Figure 3 and Figure 4). The implicit cost of debt financing is still higher than the Eurozone’s and the gap is not closing. This is partly due to the long duration of debt. While reducing refinancing risk, this also prevents a quicker decline in the cost of borrowing when interest rates decline. The other reason is that the expensive bonds issued during the crisis in 2011-2013 will remain in the portfolio for a number of years, thereby keeping the average implicit cost high. As a result, the gap with the Eurozone remains wide.

Yet, Italy has used lower interest rates as a way to deliver fiscal consolidation. In fact, the cyclically adjusted primary balance has declined from close to 4.0% in 2014 to 2.4% in 2016. The cyclically adjusted primary balance (or the structural primary balance) is probably a better measure than the structural balance to assess the true fiscal effort.

In this situation, there is clearly a need to reduce the stock of debt as soon as possible. Speeding up the disposal of remaining state-owned stakes in major companies would be a possible option. The government may announce the disposal of another stake (probably 30%) in Poste Italiane. Yet, not many assets are left at the central level and the privatisation process at the local level is still painfully slow. Reducing the stock of debt by 0.5% of GDP each year with the privatisation process, as targeted in the latest official projections, seems very ambitious. As a result, there is no silver bullet other than bringing the cyclically adjusted primary balance back to 4.0% as soon as possible.

Figure 3: Italy’s interest payments as % of GDP

Source: European Commission, Winter Forecasts, February 2016

Figure 4: Italy’s implicit financing costs

Source: European Commission, Winter Forecasts, February 2016

The bottom line

My guess is that the government will manage to pass the exam in May, but the situation will become increasingly tricky for 2017. Without bold actions to reduce current expenditures, the consolidation effort is unlikely to deliver a sustainable reduction in labour taxation and an increase in public investments. Complying with EU fiscal rules and speeding up the reduction in the debt-to-GDP ratio will be very difficult and the process will remain fragile and subject to external shocks.

Please read our comments policy before commenting.

Note: This article gives the views of the author, and not the position of EUROPP – European Politics and Policy, nor of the London School of Economics. Featured image credit: Palazzo Chigi (CC-BY-SA-2.0)

Shortened URL for this post: http://bit.ly/1RZtkVf

_________________________________

Lorenzo Codogno – LSE, European Institute

Lorenzo Codogno is Visiting Professor in Practice at the European Institute and founder and chief economist of his own consulting vehicle, LC Macro Advisors Ltd. Prior to joining LSE he was chief economist and director general at the Treasury Department of the Italian Ministry of Economy and Finance (May 2006-February 2015) and head of the Italian delegation at the Economic Policy Committee of the EU, which he chaired from Jan 2010 to Dec 2011, thus attending Ecofin/Eurogroup meetings with Ministers. He joined the Ministry from Bank of America where he was managing director, senior economist and co-head of European Economics based in London. Before that he worked at the research department of Unicredit in Milan.