Think the outlook for the UK labour market in the wake of the coronavirus pandemic looks bad? But just how bad? And along which dimensions? Jonathan Wadsworth answers these questions. He concludes that the crisis was marked by higher absences from work as well as a large rise in short-time working and hiring freezes, not by wage cuts and mass layoffs.

Think the outlook for the UK labour market in the wake of the coronavirus pandemic looks bad? But just how bad? And along which dimensions? Jonathan Wadsworth answers these questions. He concludes that the crisis was marked by higher absences from work as well as a large rise in short-time working and hiring freezes, not by wage cuts and mass layoffs.

In a rapidly evolving crisis, there is a need for timely information to assess labour market performance and develop strategies to address the problems that emerge. Statisticians are currently using graphical techniques to illustrate the grim path of ‘excess deaths’ over the Covid-19 crisis – deaths over and above the norm in any given week. These are useful, if extremely morbid, ways of conveying and updating information at regular intervals. So it can be helpful to harness these techniques to analyse labour market performance.

Administrative data, like the claimant count measure of unemployment, are timely but not generally rich enough to provide the comprehensive view of labour market performance needed to inform and develop policy. Household surveys, like the Labour Force Survey (LFS) – used to estimate the official UK unemployment rate – are much richer but have been used/made available at more discrete intervals, making assessments of labour market performance better, but less contemporary.

The LFS is, however, conducted every week of the year. So we can use this weekly information to estimate a broad range of labour market indicators at much higher frequencies than usual. We can compare the current weekly performance of, say, the unemployment rate with the equivalent weekly norm observed over the previous five years. Any sustained departures from the norm is something to take heed of.

What indicators should we look out for? Faced with a shock, firms may adjust their labour costs through changes in wages, hours or personnel. Workers have some influence on this through unions and their intrinsic worth to an employer. This means that mass layoffs should usually be a last resort, and hiring, hours, or wages may be a first response. Self-employment and temporary working are also more cyclical types of working and so could be among the first to decline in a downturn. Which of these features stands out in any recession typically varies across countries, recessions, and often during the course of a recession.

So we need to track as comprehensive a set of indicators as frequently as possible and look for any departures from the norm (‘excess’).

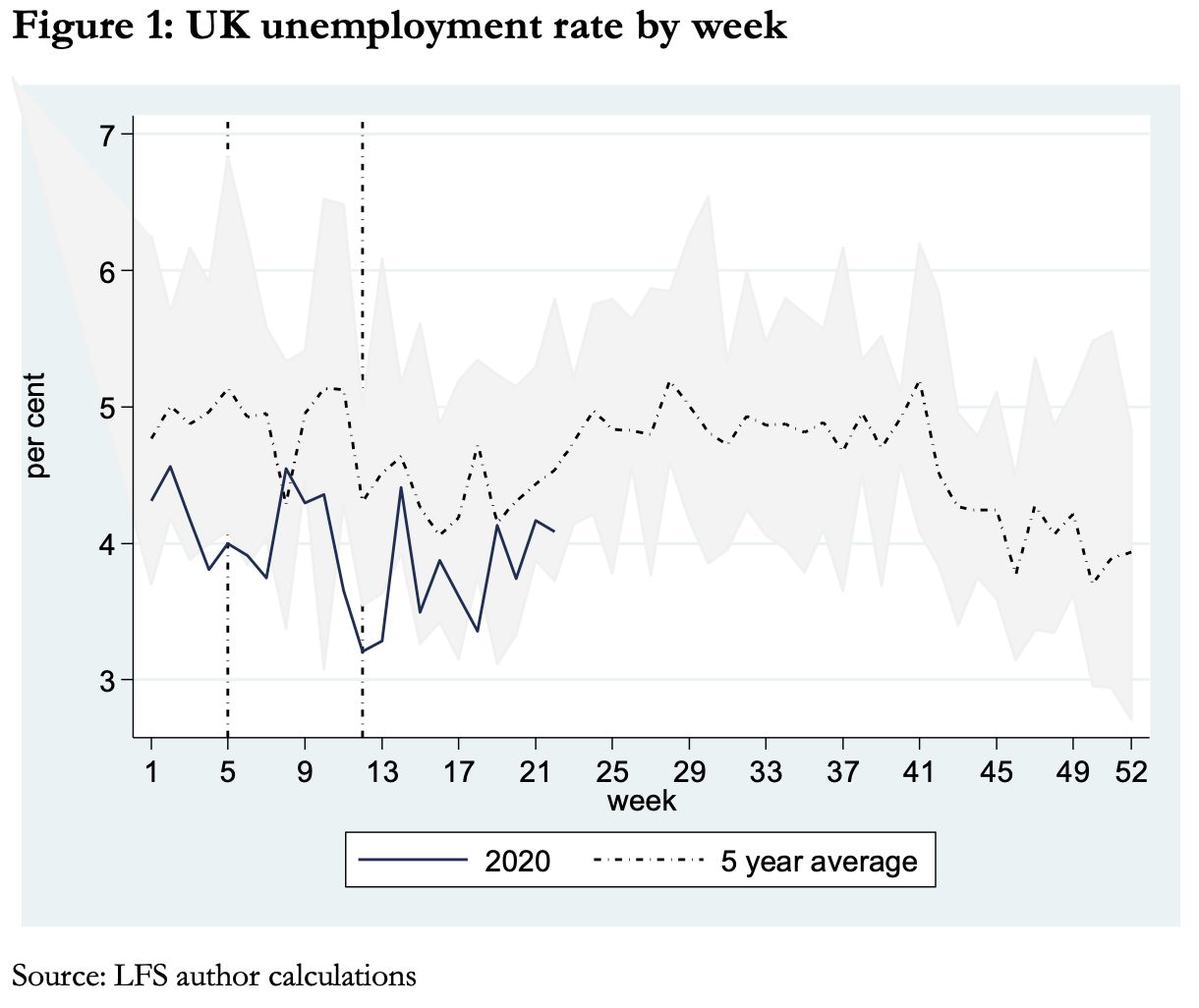

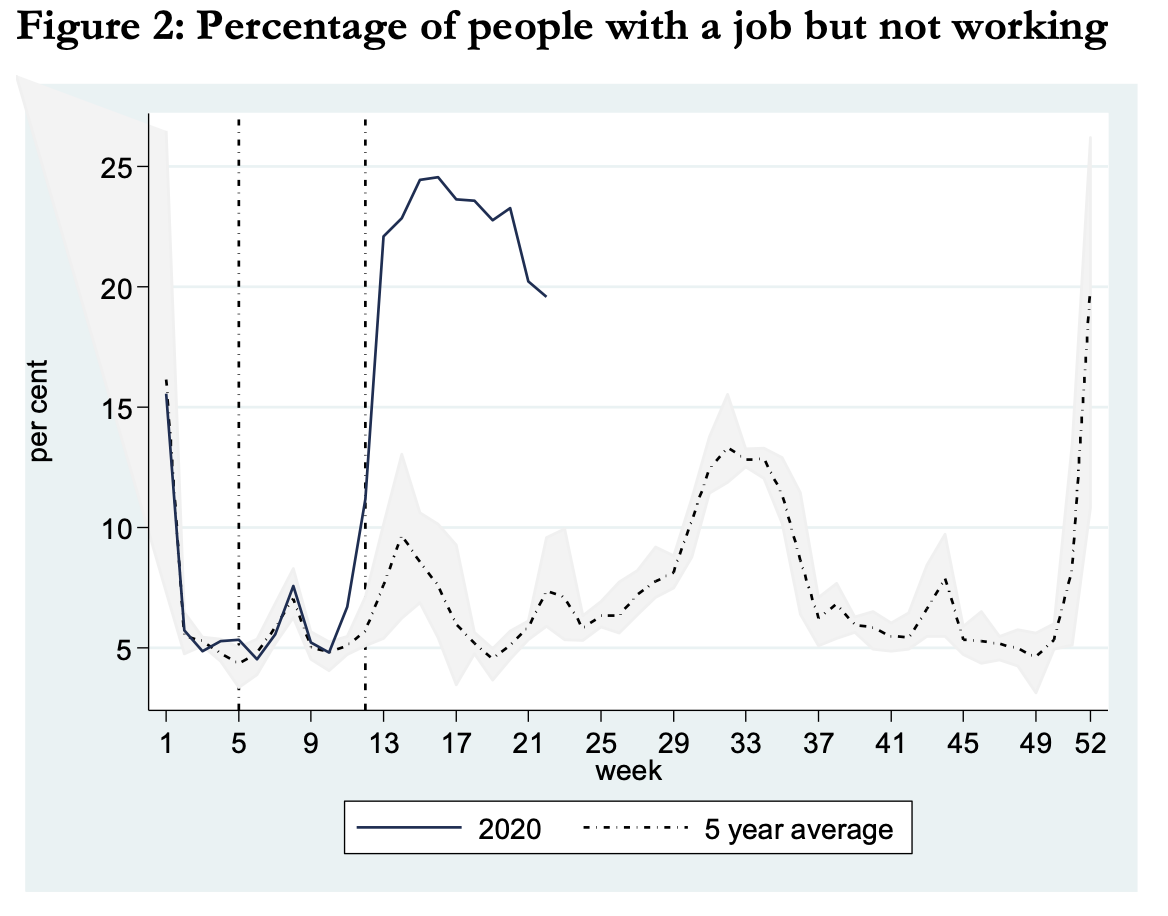

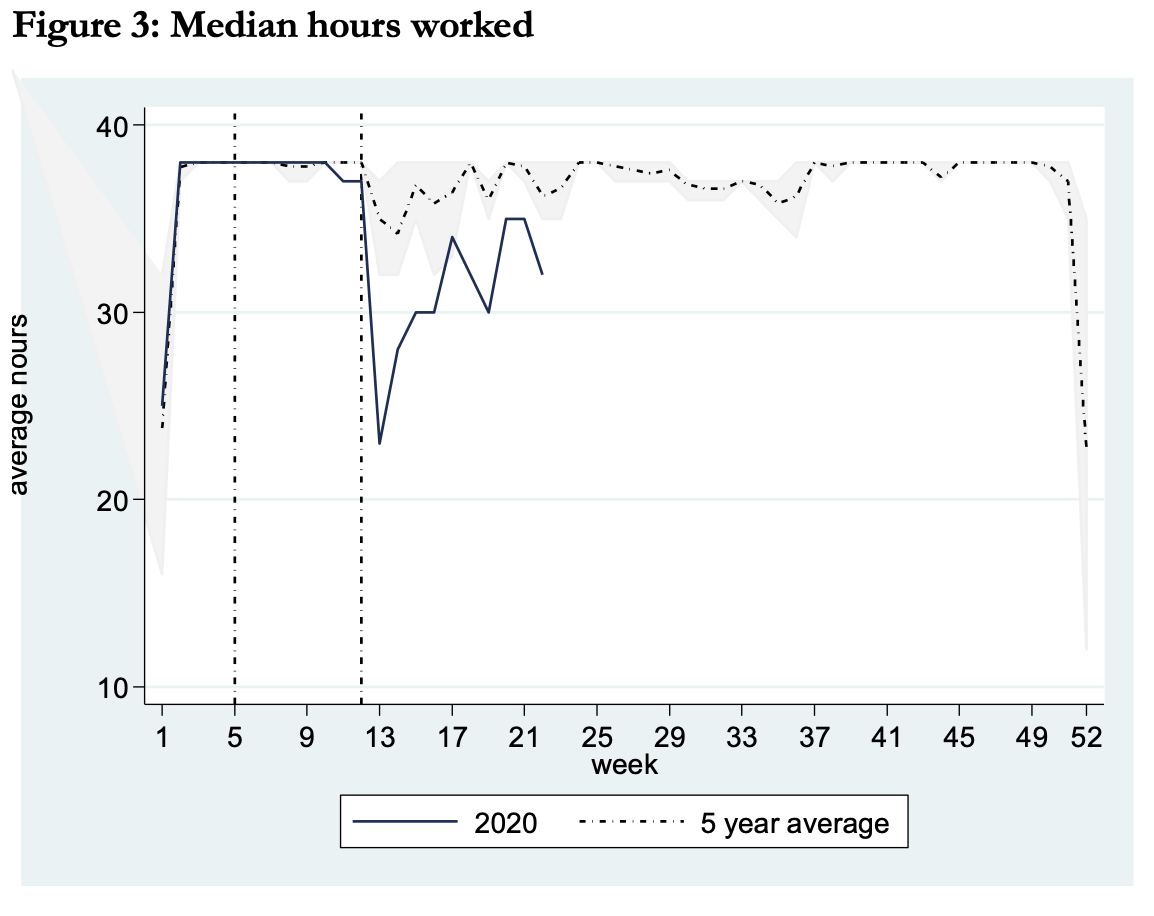

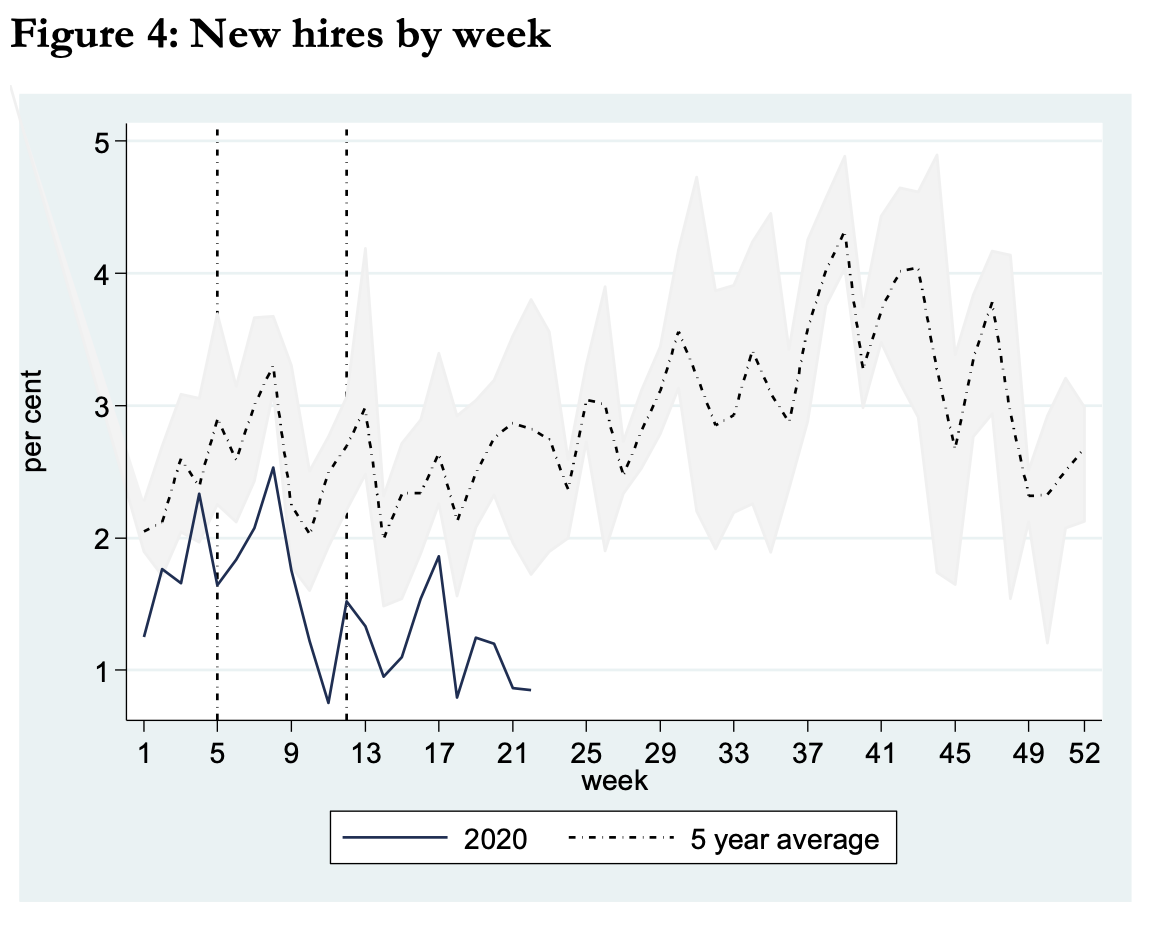

The graphs that follow plot the five-year average (dotted line) for an indicator in each week of the year – the ‘norm’ – alongside its five-yearly maximum and minimum values for the same week (grey shade). The equivalent 2020 weekly estimates (solid line) are then overlaid. The ‘excess’ on the graphs is the difference between the solid and dotted lines. Any 2020 data outside the grey range is a notable departure from the norm. Adding these weekly excesses gives the ‘cumulative excess’ of, say, unemployment, (for details see here).

The dashed vertical lines on the graphs highlight the first registered Covid-19-related death (week 5 of the calendar year) and the week the UK went into lockdown (week 12). The 2020 data currently run to week 22, the last week of May.

Unemployment

Using the most common metric of labour market performance, not much can be observed over the first twenty-two weeks of 2020 that was unusual. Figure 1 shows that UK unemployment is typically lower in the weeks that run up to Christmas and higher immediately after. However, the weekly unemployment rate in the first eighteen weeks of the coronavirus crisis was well below the average of the last five years. A similar story applies to the employment rate and self-employed and temporary jobs. No obvious departures from previous norms.

However, things start to look less than normal when we look at other margins of labour market adjustment. Figure 2 shows the percentage of workers who say they had a job but were away and did zero hours during the survey week. The weekly norms show large spikes around Christmas, Easter, and the summer holiday season. However, there is a notable departure from the norm that begins in week 10 of 2020 and increases rapidly to 24% of the employed by week 16 (four weeks into lockdown). This is around 5.4 million more workers away from their jobs than expected at that week in the year. By week 22, the start of the government’s gradual relaxation of lockdown, absences from work had fallen back to just under 20% of the employed workforce. Adding up these excesses from week 5 to week 22 suggests that there were around 53 million additional person-week absences from work. This is equivalent to the entire UK workforce doing nothing for one week and three days.

The shock to output is larger than this because among the majority of employed still in work and not away, many were working fewer hours than usual. Some 48% reported working fewer hours than usual in lockdown week 12. The number of hours worked by the average (median) worker fell from the norm of 38 to 23 during week 13 (Figure 3), before gradually rising back to around 32 hours a week by week 22, still much less than the norm for this week. Average hours worked usually drop at Christmas, Easter, and the summer holiday weeks, but the departures from the norm in week 13 and afterwards are notable.

The shock to output is larger than this because among the majority of employed still in work and not away, many were working fewer hours than usual. Some 48% reported working fewer hours than usual in lockdown week 12. The number of hours worked by the average (median) worker fell from the norm of 38 to 23 during week 13 (Figure 3), before gradually rising back to around 32 hours a week by week 22, still much less than the norm for this week. Average hours worked usually drop at Christmas, Easter, and the summer holiday weeks, but the departures from the norm in week 13 and afterwards are notable.

With 31.5 million people in work, multiplying by the number of hours each person works gives a weekly norm of around 1000 million person hours. If we add all the lost hours for every individual, the cumulative excess suggests a fall of 1700 million hours since the crisis began, equivalent to the entire workforce doing nothing for one week and two days.

Hiring in the UK also fell noticeably over the crisis. Figure 4 plots the proportion of employees who have been in new jobs for under one month. Between 2% to 4% of the workforce is usually newly-hired in any week, with fewer hires in spring and autumn being the main hiring period. However, hiring rates in the spring of 2020 were some one to two percentage points below seasonal norms in the weeks leading up to the lockdown and thereafter. In short, hiring stalled over the crisis. Cumulative hires were some 21.5 percentage points lower than usual by the end of week 22. This is around 6.8 million fewer hires than might be expected.

Hiring in the UK also fell noticeably over the crisis. Figure 4 plots the proportion of employees who have been in new jobs for under one month. Between 2% to 4% of the workforce is usually newly-hired in any week, with fewer hires in spring and autumn being the main hiring period. However, hiring rates in the spring of 2020 were some one to two percentage points below seasonal norms in the weeks leading up to the lockdown and thereafter. In short, hiring stalled over the crisis. Cumulative hires were some 21.5 percentage points lower than usual by the end of week 22. This is around 6.8 million fewer hires than might be expected.

With hiring stalled, it could be that employers have adjusted their workforce costs without the need for further adjustments. This indeed appears to be the case so far. There is no obvious departure from weekly norms in the incidence of layoffs. Nor does it seem that wages have yet taken a hit.

With hiring stalled, it could be that employers have adjusted their workforce costs without the need for further adjustments. This indeed appears to be the case so far. There is no obvious departure from weekly norms in the incidence of layoffs. Nor does it seem that wages have yet taken a hit.

So where are we?

It seems that the typical metrics of labour market performance have not been noticeably affected during the first three months of the coronavirus crisis in the UK. Instead, the crisis was marked by higher absences from work, a large rise in short-time working and hiring freezes rather than wage cuts and mass layoffs. Things may change, but we now know where and how to look.

Please read our comments policy before commenting.

Note: This article first appeared on our sister site, British Politics and Policy at LSE. It gives the views of the author, not the position of EUROPP – European Politics and Policy or the London School of Economics. Featured image credit: Pippa Fowles / No 10 Downing Street (CC BY-NC-ND 2.0)

_________________________________

Jonathan Wadsworth – Royal Holloway, University of London / LSE

Jonathan Wadsworth is Professor of Economics at Royal Holloway, University of London and a Senior Research Fellow at the LSE’s Centre for Economic Performance.