Dimitri Zenghelis argues that the government can help stimulate growth by recognising the inevitable transition to a low-carbon economy. This could provide new business opportunities for investors while tapping into a fast-growing global market for resource-efficient activities.

Dimitri Zenghelis argues that the government can help stimulate growth by recognising the inevitable transition to a low-carbon economy. This could provide new business opportunities for investors while tapping into a fast-growing global market for resource-efficient activities.

The UK faces the prospect of a protracted recession even before output has fully made up the losses from the last recession, with GDP yet to return to its 2008 peak. Yet the current period of low confidence presents a golden opportunity for UK to boost employment and stimulate economic growth, while encouraging competition and innovation.

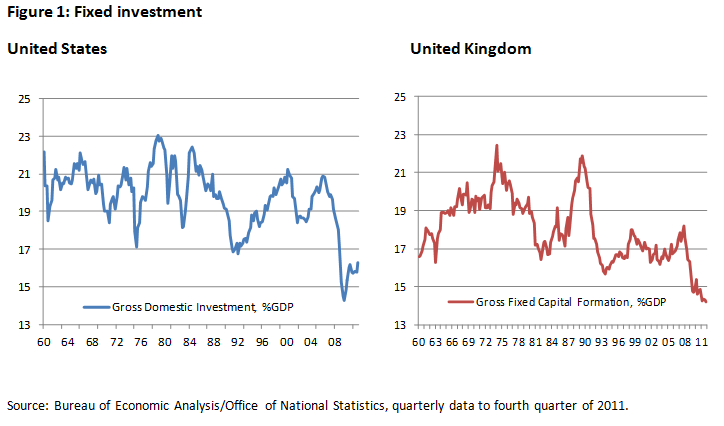

Growth requires investment, yet investment has slumped to record lows in most rich countries mainly because households, businesses and banks are nervous about future demand, and have responded by forgoing more risky investment in physical capital.

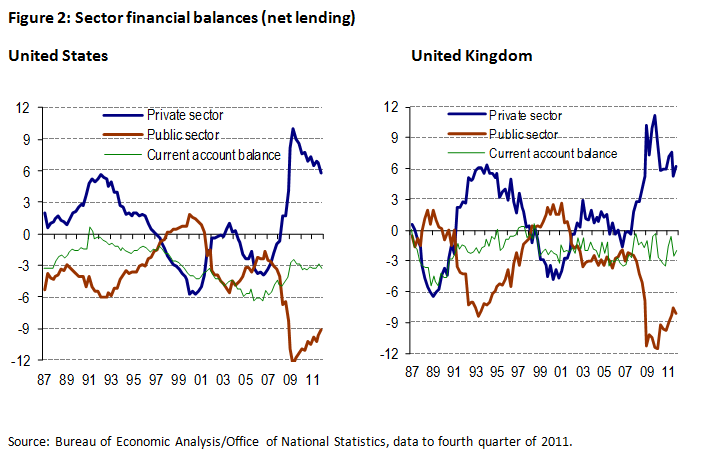

Instead, companies and households are squirreling private saving into ‘risk-free’ assets such as solvent sovereign bonds. As a result, annual private sector surpluses over the past few years have been at record levels, and amounted to £99 billion last year, equivalent to 6 per cent of UK GDP.

After the financial crash, households, businesses and banks undertook necessary and unavoidable long-run stock readjustment in balance sheets. But we are now witnessing a classic ‘paradox of thrift’, in which pessimism over the short term outlook prompts households, businesses, banks and now government to cut investment, shed labour, restrict credit and store money. But when everyone retrenches simultaneously, fear of recession becomes a self-fulfilling prophecy yielding a vicious circle of low demand and low investment.

Desired saving has exceeded desired investment in many advanced economies to such a degree that global real ‘risk-free’ interest rates for the next 20 years have been pushed below zero. Savings are losing value by the day as pension funds and financial institutions pay real interest to (rather than receive interest from) solvent governments; a truly perverse state of affairs given the need for productive investment. These low rates do not reflect a collapse in the underlying returns to capital; instead they reflect desperately depleted confidence.

What is needed to restore confidence is a clear strategic vision with supporting policies to guide investors and capture businesses imagination. In the past, governments have got out of such recessions through setting new challenges such as rearmament, electrification, space-races and Roosevelt’s New Deal. Today, policies which recognise the inevitable transition to a low-carbon economy could provide new business opportunities for investors while tapping into a fast-growing global market for resource-efficient activities. As well as leaving a lasting legacy in delivering energy security, tackling climate change, and saving consumers and businesses costs in the long run, these sectors offer long-term returns for investors. The necessary change will be massive and transformative. It will require major investment in all regions of world across all economic sectors including buildings, transportation, agriculture, manufacturing and communications.

What is needed to restore confidence is a clear strategic vision with supporting policies to guide investors and capture businesses imagination. In the past, governments have got out of such recessions through setting new challenges such as rearmament, electrification, space-races and Roosevelt’s New Deal. Today, policies which recognise the inevitable transition to a low-carbon economy could provide new business opportunities for investors while tapping into a fast-growing global market for resource-efficient activities. As well as leaving a lasting legacy in delivering energy security, tackling climate change, and saving consumers and businesses costs in the long run, these sectors offer long-term returns for investors. The necessary change will be massive and transformative. It will require major investment in all regions of world across all economic sectors including buildings, transportation, agriculture, manufacturing and communications.

The best time to support investment is during a protracted economic slowdown. Resource costs are low and the potential to crowd out alternative investment and employment is small. The most recent figures published by the Department for Business, Innovation and Skills show that the UK low-carbon and environmental goods and services sector had sales of £116.8 billion in 2009-10, growing 4.3 per cent from the previous year and placing the UK sixth in the global league table. But the private sector is not investing as heavily as it could in green innovation and infrastructure because of a lack of confidence in future returns in this policy-driven sector due to uncertainties surrounding current energy and environment policy.

Cautious investors can be driven to act now by correctly priced public resources, sweeping standards, regulations and technology support without relying on private sector sentiment to drive demand. South Korea and China have understood the logic of this approach. They recognise that investment flows to the pioneers of the revolutions and have provided strong policy support for energy efficacy, renewable technologies and electric vehicles.

The expenditure involved in making the transition to a resource-efficient economy must be assessed as an investment and not a mere resource cost. It is also important to understand the full dynamic economic costs, benefits and risks including the cost-savings from induced innovation.

The reliance on policy to drive this market has advantages in the current fragile economic environment. Only the Government can limit policy risk. Thus, by backing its own green policies, the Government can stimulate additional net private sector investment, and make a significant contribution to economic growth and employment. It can do this, for instance, by allowing a well-capitalised Green Investment Bank to operate as a lending institution, sharing some of the risk of private investments in green infrastructure. The UK should also work with European Union to increase the target for emissions reductions for 2020 to 30 per cent from 20 per cent, supporting the carbon price within the Emissions Trading System.

Promoting future growth also requires policies to shift the tax base away from intellectual activity and towards materials and resources. Finally, conveying the false impression that there is a choice between resource efficiency and economic growth undermines private sector confidence and needlessly raises the risk premium on such investment. Loose talk costs jobs. There is no lack of private money, just a perceived lack of opportunity. This window of opportunity should not be wasted.

Note: This article gives the views of the author, and not the position of the British Politics and Policy blog, nor of the London School of Economics. Please read our comments policy before posting.

Dimitri Zenghelis is a Senior Visiting Fellow at the Grantham Research Institute on Climate Change London School of Economics, Associate Fellow Royal Institute of International Affairs at Chatham House and Senior Economic Adviser Cisco.

Jayarava – you raise the right question. But the solution to indebtedness will not be collapsing demand, falling GDP and falling prices. But this is what we will get if everyone tries to draw doubt debt by simultaneously saving. So we need an alternative.

I think this paper captures the situation we are in beautifully and powerfully http://www.princeton.edu/~pkrugman/debt_deleveraging_ge_pk.pdf. It should be essential reading for policymakers.

It is a pared-down model with a lot of algebra in it, but the importance is the clear and tractable assumptions it introduces: there are two types of people; the impatient, who borrow from the patient. Debtors are constrained after an asset price adjustment (e.g. house or share price falls) in a way creditors are not. This means that hitting the zero bound in interest rates spurs the paradox of thrift we are in where cost-cutting and saving to pay down debt become counterproductive. We enter a topsy-turvy world in which saving is a vice, increased productivity can reduce output, and flexible wages increase unemployment.

The authors argue that building up public debt does not lead to Ricardian equivalent private saving because the credit constrained will consume out of current rather than long run expected income. On this, I think they understate the immediate impact of the bond markets in offsetting consumer behaviour by pushing up risk premiums on indebted bonds, a factor of which Osborne and co are acutely aware.

But this is where the win-win beauty of ‘green’ markets comes in. Because the public sector can define such market without extra borrowing by setting up credible policies on pricing, standards and regulations and taking on policy risk which it owns, it can induce a massive recycling of private saving into productive investment, just when we need it most and just resource costs are lowest.

In past global recessions, rearmament, electrification and space races have helped restore investor confidence – this time the vision should be declaring war on resource waste.

“Growth requires investment…”

Yes. In the UK banks only invest about 8% in the real economy which should be more like 50%.

But like most people you ignore one of the major factors in the lack of investment: private sector debt. The most recent estimates put it a bit over 500% of GDP. Very much higher than in the first Great Depression. So my question is this. How is the private sector going to borrow enough for growth to occur without causing a credit crunch?

The likelihood is that with private debt at these levels we’ll have a credit crunch anyway. So why is everyone saying that the solution is for the private sector to take on even greater levels of debt, at what will be extortionate interest rates?

It might just work if the money bypasses banks and goes straight into business. It would be even better if the government just gave them money. But the debt is only going to dissipate very slowly. Like Japan.