The issue of inequality is one of the most salient in global and European politics. Thomas Piketty writes on the economic forces which have impacted upon inequality since the end of the First World War. He argues that with disparities in income and wealth rising substantially over recent decades, a global progressive tax on individual net worth would offer the best option for keeping inequality under control. He writes that although implementing such a tax would be a major challenge politically, it would be feasible if the EU and the United States, each accounting for around a quarter of world output, put their combined weight behind it.

The issue of inequality is one of the most salient in global and European politics. Thomas Piketty writes on the economic forces which have impacted upon inequality since the end of the First World War. He argues that with disparities in income and wealth rising substantially over recent decades, a global progressive tax on individual net worth would offer the best option for keeping inequality under control. He writes that although implementing such a tax would be a major challenge politically, it would be feasible if the EU and the United States, each accounting for around a quarter of world output, put their combined weight behind it.

The distribution of income and wealth is one of the most controversial issues of the day. History tells us that there are powerful economic forces pushing in every direction – towards greater equality, and away from it. Which prevail will depend on the policies we choose.

America is a case in point. Here is a country that was conceived as the antithesis of the patrimonial societies of old Europe. Alexis de Tocqueville, the 19th century historian, saw America as the place where land was so plentiful that everyone could afford property and a democracy of equal citizens could flourish. Until the First World War, the concentration of wealth in the hands of the rich was far less extreme in the US than in Europe. In the 20th century, however, the situation was reversed.

Between 1914 and 1945 European wealth inequalities were wiped out by war, inflation, nationalisation and taxation. After that, European countries set up institutions which – for all their faults – are structurally more egalitarian and inclusive than those of the US.

Ironically, many of these institutions drew inspiration from America. From the 1930s to the early 1980s, for example, Britain maintained a balanced distribution of income by hitting what were deemed to be indecently high incomes with very high tax rates. But confiscatory income tax was in fact an American invention – pioneered in the interwar years at a time when that country was determined to avoid the disfiguring inequalities of class-ridden Europe. The American experiment with high tax did not hurt growth, which was higher at the time than it has been since the 1980s. It is an idea that deserves to be revived, especially in the country that first thought of it.

The US was also first to develop mass schooling, with nearly universal literacy – among white men, at any rate – in the early 19th century, an accomplishment that took Europe almost another 100 years. But again, it is Europe that is now more inclusive. True, the US has produced many of the world’s outstanding universities, but Europe has done better at producing solid middle-ranking ones. According to the Shanghai ranking, 53 of the 100 best universities in the world are in the US, and 31 in Europe. Look instead at the top 500 universities, however, and the order is reversed: 202 in Europe against 150 in the US.

People often talk up the virtues of their national meritocracies, but – whether in France, America or elsewhere – such rhetoric seldom fits the facts. Often the purpose is to justify existing inequalities. Access to American universities – once among the most open in the world – is highly unequal. Building higher education systems that truly combine efficiency and equal opportunity is a major challenge facing all countries.

Mass education is important, but it does not guarantee a fair distribution of income and wealth. US income inequality has sharpened since the 1980s, largely reflecting the huge incomes of people at the top. Why? Have the skills of the managerial cadre advanced further than everyone else’s? In a large organisation, it is hard to know how much each person’s work is worth. But another hypothesis – that top managers by and large have the power to set their pay themselves – is better supported by the evidence.

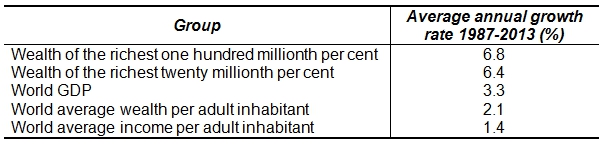

Even if wage inequality could be brought under control, history tells us of another malign force, which tends to amplify modest inequalities in wealth until they reach extreme levels. This tends to happen when returns accrue to the owners of capital faster than the economy grows, handing capitalists an ever larger share of the spoils, at the expense of the middle and lower classes. It was because the return on capital exceeded economic growth that inequality worsened in the 19th century – and these conditions are likely to be repeated in the 21st. According to Forbes global billionaire rankings, top wealth holders have been rising more than three times faster than the size of the world economy between 1987 and 2013. The Table below illustrates the overall trend in wealth and income growth for different groups.

Table: Average annual growth rate in the wealth/income of groups of the world’s population

Source: Capital in the 21st Century

US inequality may now be so sharp, and the political process so tightly captured by top earners, that this will not happen – much like in Europe before the First World War. But that should not stop us from aspiring to improve. The ideal solution would be a global progressive tax on individual net worth. Those who are just getting started would pay little, while those who have billions would pay a lot. This would keep inequality under control and make it easier to climb the ladder. And it would put global wealth dynamics under public scrutiny. The lack of financial transparency and reliable wealth statistics is one of the main challenges for modern democracies.

Of course there are alternatives. China and Russia, too, must deal with wealthy oligarchies, and they do it with their own tools – capital controls, and jails whose bleak walls can contain the most ambitious oligarchs. For countries that prefer the rule of law and an international economic order, a global wealth tax is a better bet. Maybe China will come round to it before we do. Inflation is another potential solution. In the past it has helped lighten the burden of public debt. But it also erodes the savings of the less well off. A tax on vast fortunes seems preferable.

A global wealth tax would require international co-operation. This is difficult but feasible. The US and the EU each account for one-quarter of world output. If they could speak with one voice, a global registry of financial assets would be within reach. Sanctions could be imposed on tax havens that refused co-operation. Short of that, many may turn against globalisation. If, one day, they found a common voice, it would speak the disremembered mantras of nationalism and economic isolation.

For a longer discussion of this topic, see Thomas Piketty’s book, Capital in the 21st Century

Note: This article gives the views of the author, and not the position of the British Politics and Policy blog, nor of the London School of Economics. Please read our comments policy before posting. Homepage image credit:

_________________________________

About the Author

Thomas Piketty – Paris School of Economics

Thomas Piketty is a Professor of Economics at the Paris School of Economics. He is the author of Capital in the 21st Century (Harvard University Press, March 2014).

A land value tax is better and more practicable.

Gary Reber Comments:

Such redistribution schemes, which tax those who are productive either through their capital wealth or labor or both, strengthen the politicians and State control over citizens. The focus should be on empowering EVERY citizen to be productive through access to the means of acquiring and possessing property, simultaneously with the growth of the economy, while abating further concentration of capital wealth. Thomas Piketty states that people few America America as the place where land was so plentiful that everyone could afford property and a democracy of equal citizens could flourish. But the land is now all owned; there is no more. But capital formation is virtually unlimited. And there should be the focus – broadening its ownership simultaneously with its formation so that over time EVERY child, woman and man accumulates a significant capital estate.

The end result is that citizens would become empowered as owners to meet their own consumption needs and government would become more dependent on economically independent citizens, thus reversing current global trends where all citizens will eventually become dependent for their economic well-being on the State and whatever elite controls the coercive powers of government.

This is more than necessary, it’s inevitable. Each individual from different levels of inequality spiral ought to support this theory in order to sustain economic system.

I’d much sooner see a land value tax. LVT is also more achievable.

I hope that this would be possible, but obviously the wealthy are often the politically powerful and they’d oppose it.

The focus of taxation should always be wealth and unearned income, rather than earned income.

What is/are the data sources for the claim about literacy ? “with nearly universal literacy – among white men, at any rate – in the early 19th century, an accomplishment that took Europe almost another 100 years”.