The vast majority of tall buildings—even if they appear out of scale given contemporary perceptions—have a solid economic case, write Gabriel M. Ahlfeldt and Jason Barr.

The vast majority of tall buildings—even if they appear out of scale given contemporary perceptions—have a solid economic case, write Gabriel M. Ahlfeldt and Jason Barr.

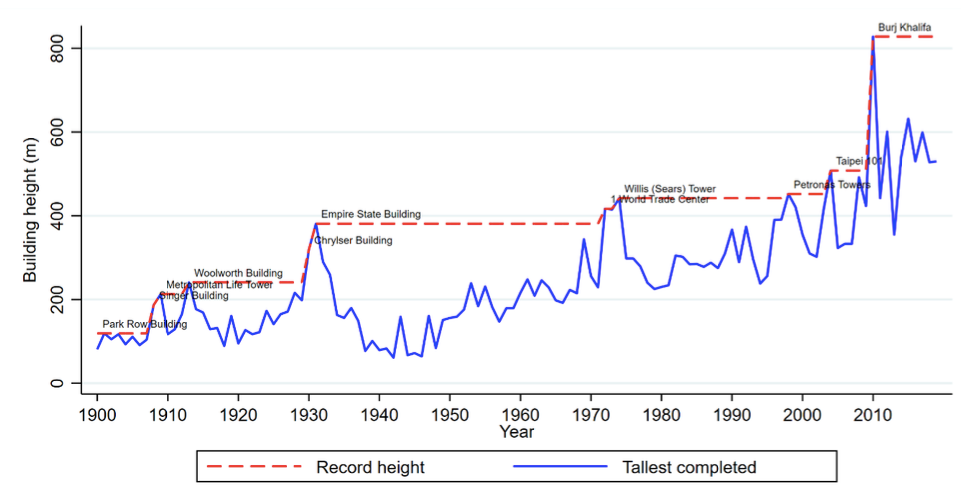

A hundred years ago, policymakers in New York were convinced that, “few skyscrapers pay large net returns…” and that, “the very tall buildings demand many things out of proportion to their increased bulk” (Heights of Buildings Commission, 1913). Despite their sentiments, their belief in the death of the skyscraper was premature. The Empire State Building, which was viewed as nothing short of maniacal in 1931, is now decidedly second tier (the 41st tallest structure in the world). In 2010, the Burj Khalifa, at 828 meters high, set the new record for the world’s tallest building. Industry experts felt that its height was driven by developers’ egos rather than compelling economics (Tomlinson, 2016). Contrary to this widespread perception, our recent review of skyscrapers’ economics suggests that economic variables are driving the trend to ever taller buildings.

The role of fundamentals

Figure 1 shows the height of the tallest building completed each year around the world from 1900 to 2019, along with the height of the world’s tallest building. The first main finding is that there is a reasonable and sustainable long-run trend, suggesting that fundamental factors matter. The average annual trend rate for the tallest structures is 1.3%. As a comparison, since 1960, real global GDP has had a trend of 3.2% (World Bank, 2020).

Figure 1 – Height of tallest building completed each year (1900-2019) vs height of world’s tallest building

Source: Ahlfeldt & Barr (2020)

To think about the economics of tall buildings, it is convenient to distinguish between drivers of building height that impact the demand versus those that impact their supply. Urban residents and businesses are willing to pay to be in tall buildings because they are centrally located and make life more convenient. Developers are willing to build tall to accommodate this demand. However, constructing taller structures comes with extra costs. Taller buildings require more sophisticated structural engineering (to withstand wind forces, for example) and more facilities such as elevators. Intuitively, developers build up to the economic height, the point where the cost of adding a floor is just equal to the revenues from that floor. Above that height, the extra revenues do not compensate for the extra costs.

As cities grow, office and apartment rents will rise over time because there is limited central-city land. Since higher rents imply greater revenues from additional floors, developers have a greater incentive to create vertical land in the sky. Furthermore, if residents are willing to use some of their rising disposable incomes to pay for better views, this will also incentivise buildings to go even taller.

On the supply side, the electric elevator and steel-framed structure inventions at the end of the 19th century removed many of the previous barriers to building tall. Since then, constant technological improvements have reduced the cost of adding floors. Computing software and wind tunnel testing has allowed engineers to design more efficient structures based on simulated tests. Such technological change reduces the costs of building tall buildings, increasing the economic height. One of the insights of our theoretical analyses is that the incentive to respond to reductions in the cost of tall buildings is largest where rents are highest. Therefore, reductions in the cost of height lead to more than proportionate changes in building heights in the city centers of global cities.

Non-economic motives

Returning to Figure 1, some buildings stand out as particularly tall relative to the trend and remain relatively tall for a very long time. This has fueled the suspicion that some developers may have non-profit-maximizing objectives. In the economics literature, skyscraper development has been modelled as a race to gain personal satisfaction by owning the tallest building. Mathematical game theory delivers the prediction that the winning developer builds a much taller structure than the economic height to preempt would-be competitors.

This notion of pre-emption would suggest that buildings will retain their titles for a very long time, say for decades. But as of 2015, only three buildings in the world held the title of world’s tallest for more than ten years (the Burj Khalifa recently joined this club). The median is just six years. Within countries, the average record length is less than ten years, and the median is only four. This fast succession substantiates the notion that long-run trends in economic fundamentals are essential drivers of vertical growth.

Yet, there are exceptions, and the most impressive is the Empire State Building, which topped the world height ranking for 40 years. Its economics were frequently called into question – it was called the “Empty State Building” during the Great Depression. While it cost a historically impressive $50 million for the land and structure (in roughly 1930 dollars), by 1950, its net operating income was about $6.8 million, thus exceeding 10% of the inflation-adjusted total cost. Its net income has increased over the years in real terms, on average (not least, thanks to the observation deck, which nowadays generates $130 million per year alone). Over its lifetime, it appears to have beaten the stock market in terms of returns on investment, which adds to the notion that a skyscraper’s economics may be rejected too casually.

Being able to draw an exact line between the economic rationale and irrational developments is still work for future research. But in the meantime, we are safe in concluding that the vast majority of tall buildings—even if they appear out of scale given contemporary perceptions—have a solid economic case. If the history of height is any guide, the future direction for their economics is only upwards.

- This blog post is based on the paper The Economics of Skyscrapers: A Synthesis, Discussion Paper 1704 of LSE’s Centre for Economic Performance (CEP). and appeared originally at LSE Business Review.

- Featured image by Nick Fewings on Unsplash

Please read our comments policy before commenting

Note: The post gives the views of its authors, not the position USAPP– American Politics and Policy, nor of the London School of Economics.

Shortened URL for this post: https://bit.ly/3hUSq6g

About the authors

Gabriel Ahlfeldt – LSE Geography and Environment

Gabriel Ahlfeldt is an associate professor of urban economics and land development at LSE’s department of geography and environment, and a researcher at LSE’s Centre for Economic Performance (CEP). He is the director of the MSc in real estate economics and finance. In his research, he is interested in how various agglomeration forces shape the spatial distribution of economic activity. His research also analysis the impact of various spatial policies on local house prices, labour markets, political preferences and urban structure.

Jason Barr – Rutgers University-Newark

Jason Barr is a professor at Rutgers University-Newark, department of economics, and an affiliated faculty member with the Global Urban Systems Ph.D. programme. His research interests include urban economics, and agent-based computational economics. He is the author of Building the Skyline: The Birth and Growth of Manhattan’s Skyscrapers (Oxford U. Press, 2016). He writes the Skynomics Blog, a blog about skyscrapers, cities, and economics.