Every so often we have an event that steals the headlines for what it was not about and such was the case for Christine Lagarde’s four-day visit to Nigeria in January 2016. The IMF Managing Director sought to disabuse widespread speculation that Africa’s largest economy ($ 500.0 billion in GDP size) was out to secure bailout in view of the fiscal migraine occasioned by cratered oil prices.

To be fair, though, it is hard to blame the rumour mills since the timing of the visit was especially suspect for the doctor-in-chief of the global financial infirmary to be visiting a country grappling with fiscal distress. In its stead, Lagarde lauded the new administration for efforts towards greater fiscal prudence — and that came with no surprise.

Nigeria had a watershed election in 2015 and it has been business unusual with the new sheriff in town – President Muhammadu Buhari. In September 2015, Buhari appointed himself Oil Minister, placing under his nose the daunting, if possible, task of plumbing wanton leakages that have been responsible for the siphoning of millions of dollars from state coffers at a time when depressed prices have yielded an economic fever build up.

Fixing Nigeria’s monetary side is more difficult

But if the focus has been on getting fiscal housekeeping right, the monetary side seems to be having a tougher needle to thread, and I explain. On 24 November 2015, the Central Bank of Nigeria slashed the benchmark rate by 200 basis points to 11 percent. The slash was significant for two reasons. One, it was the first in six years and spoke volumes of heightened efforts to inject a shot of adrenaline into the increasingly lackluster economy. Two, it leaned against the prevailing wind of monetary tightening across Sub-Saharan Africa and could well have marked the onset of policy divergence amongst major markets in the region.

Looking at underlying fundamentals, the move would seem to have been a no brainer for Godwin Emefiele, the governor of the Central Bank of Nigeria, and his team:

Growth – The economy has been dragging its feet, growing by 2.35 percent in the second quarter and 2.84 percent in the third quarter of 2015 down from 6.54 percent and 3.38 percent in the same periods of 2014 respectively.

Credit – Between January and November 2015, credit to the private sector grew by a paltry 2.9 percent, to USD 93.9 billion, posting the slowest growth in five years — compared to 12.8 percent and 9.7 percent in the same period in 2014 and 2013, respectively (data from the Central Bank of Nigeria).

Unemployment – The rate of unemployment soared from 7.5 percent in the first three months of 2015 to 9.9 percent in the third quarter of 2015, as opportunities created fell disproportionately below the influx of new entrants into the labour market. The manufacturing sector (accounting for 10 percent of the GDP and about 12 percent of formal employment) slumped deeper into contraction in the second quarter of last year (by about five percent year-on-year).

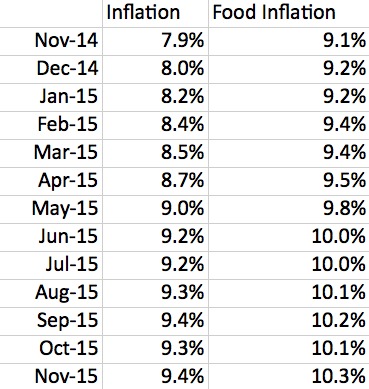

If one considers, however, that inflation soared to a high of 9.4 percent (November 2015) breaching the target ceiling by 40 basis points, it becomes clear that the Central Bank executed triage with the rate slash — the salient implication being that for Emefiele and his team, runaway inflation presents a lesser evil than an economy flirting with near stagnation. Crafting policy direction in an environment of such conflicting demands can be a tightrope; monetary tightening could prove to be a grave misdiagnosis, sapping the little, if any, energy left in a faltering economy and potentially providing an amplification channel for further economic downturn.

Table 1. Nigeria’s monthly inflation and food inflation rates in the 12 months from November 2014 to November 2015

Source: Central Bank of Nigeria

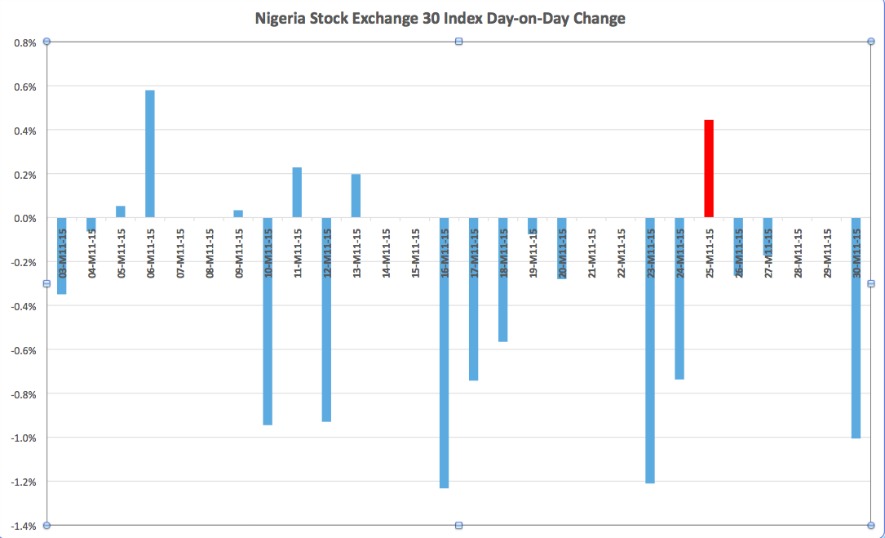

But if the rate slash was meant to be a confidence builder for investors, the market’s feedback was double edged. The Nigeria Stock Exchange 30 Index gained a marginal 0.4 percent, day-on-day, on the back of the rate slash. It was one of the few and far-spaced days in which the market made a frail attempt at clawing back lost ground in November 2015, possibly signalling much needed booting from bearish sentiments by investors.

Figure 1

Source: Bloomberg, Stratlink Africa. Note: red bar indicates the day the Central Bank cut interest rates.

On the flip side, however, the gain was both mild and short-lived enough to remind policy makers that, by and large, investors still felt snookered by the adverse economic climate, especially with oil prices plummeting far below the $ 67/barrel fiscal break-even price estimate for 2015, which increasingly raises the prospect of the Central Bank back-pedalling on its hard stance and devaluing the Naira. Away from the capital markets, however, a lot more time will be need for the transmission effect of the rate slash to filter through the economy and that is an assessment best deferred to a later date. In the meantime, however, the government seems to be leaving nothing to chance and double barrels are being fired towards revving up the economy. Alongside an accommodative monetary policy, a dose of fiscal stimulus is in the pipeline with plans to see 2016’s national budget near double that of the preceding year at about $ 40.2 billion. Interesting times they are for Africa’s largest economy.

♣♣♣

Notes:

- This post gives the views of its author, not the position of LSE Business Review or the London School of Economics.

- Featured image credit: Lagos Skyline Clara Sanchiz CC-BY-SA-2.0

Julians Amboko is a Research Analyst with StratLink Africa Ltd, a Nairobi-based financial advisory firm focusing on emerging and frontier markets. He covers macroeconomic research and analysis for Sub-Saharan Africa, including markets such as Nigeria, Kenya, Ethiopia, Ghana, and Angola.

Julians Amboko is a Research Analyst with StratLink Africa Ltd, a Nairobi-based financial advisory firm focusing on emerging and frontier markets. He covers macroeconomic research and analysis for Sub-Saharan Africa, including markets such as Nigeria, Kenya, Ethiopia, Ghana, and Angola.

2 Comments