explain why austerity is no longer an election winner – neither economically nor politically. They argue that David Cameron’s government reaped political rewards through its austerity rhetoric, but the strategy backfired in the next election, when many voters believed a Conservative government would impose more hardship on them.

In our book on the 2015 general election we showed that economic recovery was the most important factor in explaining the surprise victory for the Conservatives. It played a key role in the 2017 general election as well. So the story of these two elections supports the longstanding proposition that incumbent parties are rewarded by the voters for a good economic performance and are punished by a bad one. To repeat a famous phrase coined by James Carville, a chief campaign advisor to Bill Clinton in the 1992 US presidential election: ‘It’s the economy, stupid!’

However, the story is not as straightforward as it seems, since the initial economic policy adopted by George Osborne when he became Chancellor of the Exchequer in 2010 would have almost certainly lost the election for the Conservatives had he not changed course in the middle of the Parliament. The original austerity plan embedded in the Coalition Agreement of 2010 derived from a mixture of theoretical ideas about how the economy works, but it was also the product of a conscious electoral strategy.

In the 2010 campaign the Conservatives made much of the argument that Britain faced imminent bankruptcy and was in a similar position to Greece and other cash-strapped EU countries. This rhetoric was driven by the need to provide a radical alternative narrative to that of the Labour Party. This narrative enabled both Coalition partners to blame Gordon Brown and Labour policies for the Great Recession. This claim was very wide of the mark since the crash started when a real estate bubble in the US burst, and it spread quickly to banks and other financial institutions which themselves had been creating opaque and highly risky financial instruments that proved valueless when the crisis broke.

However, the Conservatives’ economic argument proved to be a very potent message in the 2010 general election, so much so that echoes of it were still being heard in 2015 and again in 2017. The focus on the size of the budget deficit as the root cause of the problem was an essential campaign strategy because the economy was recovering at that time. With the recovery taking place they needed to frame the debate by focusing on the bad news of debt and ignoring the good news of growth.

That said, the budget deficit in 2009-10 was very high by historical standards, but not so much that it triggered serious problems for a government trying to borrow in financial markets. We know this by looking at long-term interest rates in Britain which measure the extent to which British governments can fund their borrowing. If borrowing is so high as to trigger a fear of default, then foreign lenders would require a premium on the interest payments they receive in order to compensate them for the extra risks. This would drive long-term interest rates higher, something which actually happened to Greece. In fact, long-term interest rates in Britain declined during this period, largely because the country was experiencing deflation and also the policy of quantitative easing kept rates at a low level.

Having ousted Labour from Downing Street in 2010, the Chancellor then proceeded to follow through on the cuts. This was because he had bought the idea that austerity brings recovery. His views were set out in a speech delivered in April 2009 before the election: ‘The crisis has also exposed two fundamental arguments. The first is whether, when you are already borrowing too much, you should deliberately try to borrow your way out of debt. David Cameron and I have consistently argued against this irresponsible course of action.’

This meant that the newly-formed government embarked on a policy of deflation in a context in which traditional policy-making would have taken the opposite course of action. But following the 2010 election, the British public mood darkened as the Coalition Government’s stringent austerity policy medicine was prescribed and the country’s economic misery deepened. Evaluations of the national economy and personal financial circumstances became deeply pessimistic and, for a time, it appeared that the Government would be punished severely in 2015 for its harsh, and apparently failed, attempt to restore the country’s economic well-being.

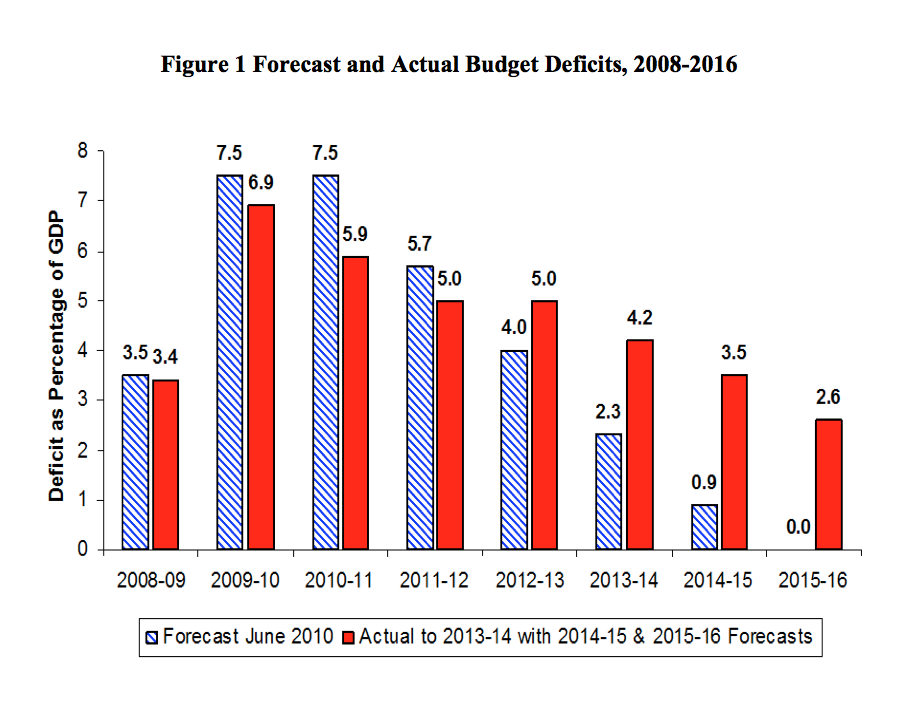

Figure 1 shows the actual and forecast budget deficits as a percentage of GDP published by the Office of Budgetary Responsibility in June 2010 and then again in December 2014. The budget deficit reduction strategy was on course to reduce the deficit to zero by 2015-16 up until 2012-13, at which point it went into reverse. In later years, the budget squeeze continued, but at a much slower rate than set out in the original plans. The result was that the gap between those plans and outcomes widened each year reaching 2.6% of GDP by the time of the 2015 election.

Figure 1 shows the actual and forecast budget deficits as a percentage of GDP published by the Office of Budgetary Responsibility in June 2010 and then again in December 2014. The budget deficit reduction strategy was on course to reduce the deficit to zero by 2015-16 up until 2012-13, at which point it went into reverse. In later years, the budget squeeze continued, but at a much slower rate than set out in the original plans. The result was that the gap between those plans and outcomes widened each year reaching 2.6% of GDP by the time of the 2015 election.

As a consequence of this deft change of strategy, the economic situation began to brighten. Statistics on key economic indicators such as growth and employment started to improve and as did the public’s economic mood. The trend accelerated as the election approached and our analysis showed that while the economy was not the only issue that mattered in the election, it was the most important factor when it came to influencing support for the major parties. The Conservatives gained and Labour, the Liberal Democrats, and UKIP all lost ground.

The Conservatives hoped to repeat the strategy in 2017 with the slogan of ‘strong and stable leadership’, but by then support for what was left of austerity had rapidly waned among the voters. Seven years of cuts involving flat-lining real wages and a severe cash crisis in the public services began to show. One group in particular which had been heavily-hit by the austerity policies were the young. A rising burden of debt produced by burgeoning fees and usurious interest rates charged on loans to students became a key political issue. Similarly, those under the age of 25 were excluded from the increase in the minimum wage introduced in April 2016 and they were increasingly aware of being left behind. As a consequence, Labour won 65% of the youth vote in 2017 on a much higher turnout of this group.

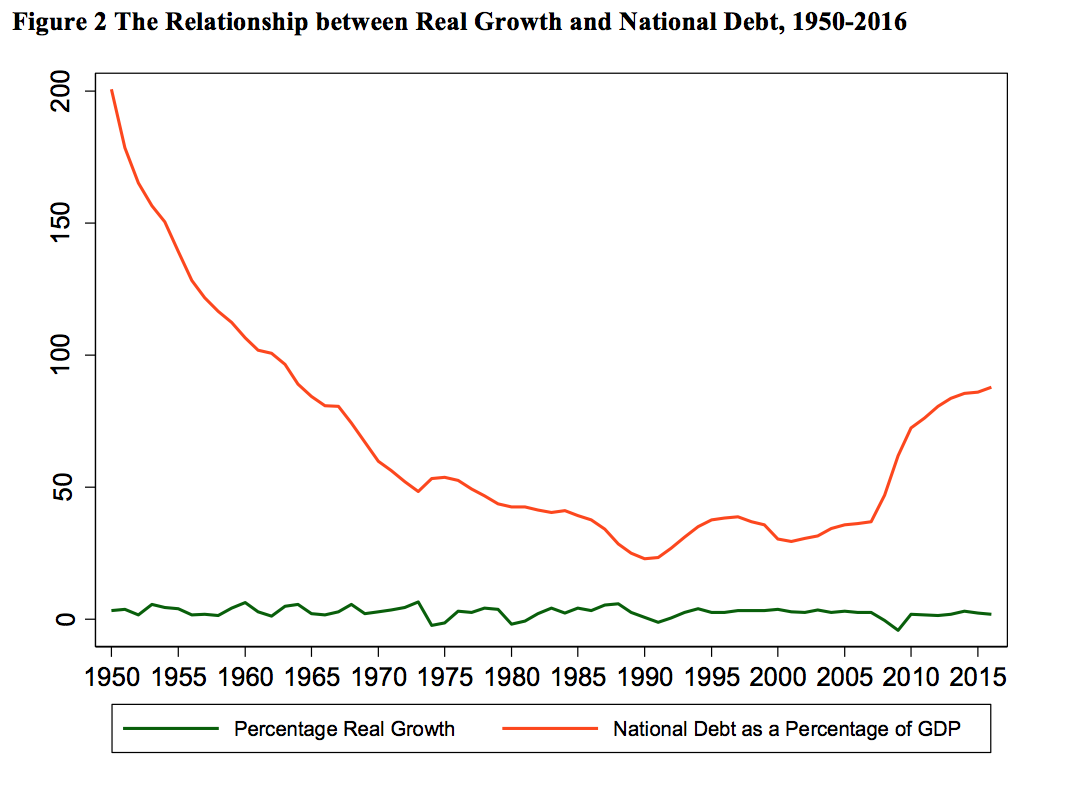

Figure 2 shows the relationship between real growth in the economy and the size of the national debt as a percentage of GDP over the period from 1950 to 2016. The data are from the Bank of England and with a very weak positive correlation between the two (+.15) it shows that there is essentially no reliable relationship between debt and growth. If anything, the positive correlation suggests that increased debt has been associated with higher, not lower, growth rates. As Mark Blyth points out in his excellent book on the history of Austerity: ‘Austerity has been tried and will keep being tried, at least for the Eurozone, until it’s either abandoned or voted out. It doesn’t work’.

In the end, austerity looks to be a loser, both economically and politically. The Cameron-Osborne Conservatives reaped political rewards in 2015 not by enforcing austerity but by relaxing it to revitalize the economy in the run-up to that year’s general election. But, as Theresa May will testify, they did go far enough. In 2017, many voters, particularly young people, believed a May-led Conservative government would impose more hardship on them in the years ahead. That prospect proved decidedly unpopular and in the wake of their near-defeat, with the Prime Minister and her colleagues now scrambling to replace both the rhetoric and the reality of austerity.

In the end, austerity looks to be a loser, both economically and politically. The Cameron-Osborne Conservatives reaped political rewards in 2015 not by enforcing austerity but by relaxing it to revitalize the economy in the run-up to that year’s general election. But, as Theresa May will testify, they did go far enough. In 2017, many voters, particularly young people, believed a May-led Conservative government would impose more hardship on them in the years ahead. That prospect proved decidedly unpopular and in the wake of their near-defeat, with the Prime Minister and her colleagues now scrambling to replace both the rhetoric and the reality of austerity.

_______

Note: the above draws on the authors’ chapter “The Rhetoric and Reality of Austerity: Electoral Politics in Britain 2010 to 2015“, in “State, Institutions and Democracy“.

About the Authors

Paul Whiteley is Professor at the Department of Government, University of Essex.

Paul Whiteley is Professor at the Department of Government, University of Essex.

Harold D. Clarke is Ashbel Smith Professor, School of Economic, Political and Policy Sciences, University of Texas at Dallas, and Adjunct Professor, Department of Government, University of Essex.

Harold D. Clarke is Ashbel Smith Professor, School of Economic, Political and Policy Sciences, University of Texas at Dallas, and Adjunct Professor, Department of Government, University of Essex.

Marianne Stewart is Professor in the School of Economic, Political and Policy Sciences at the University of Texas at Dallas.

All articles posted on this blog give the views of the author(s), and not the position of LSE British Politics and Policy, nor of the London School of Economics and Political Science. Featured image credit: Conservatives (Flickr/CC BY-NC-ND 2.0)

“This was because he had bought the idea that austerity brings recovery”

Disagree. He bought the idea that cutting public spending brings massive tax cuts to people like him, his family and his friends and the idea that it requires privatisation, which brings massive profits to people like him, his family and his friends