When questioned about the government’s Brexit sectoral impact assessments, David Davis said there were none, because “economic forecasts do not work”. Costas Milas explains why this excuse does not hold up.

When questioned about the government’s Brexit sectoral impact assessments, David Davis said there were none, because “economic forecasts do not work”. Costas Milas explains why this excuse does not hold up.

Quizzed at a hearing of the Exiting the European Union Committee, Secretary of State for Exiting the European Union David Davis stated that there are no sectoral impact assessments on Brexit. In fact, Davis ‘justified’ the apparent lack of quantitative impact within the notorious 850-page dossier on the grounds that “an impact assessment consists of a quantitative forecast” and “as we have said….economic forecasts do not work”.

Yet, quantitative forecasts are an essential part of our daily routine. Consider, for instance, a simple trip from Stoke-on-Trent to Wembley. Drivers interested in this trip do not have any hesitation to consult the ‘router planner’ of the AA website which suggests up to three alternative routes. These routes are based on a very simple quantitative model which provides three different ‘forecasts’ of the arrival time to Wembley. Ignoring forecasting because, in the words of Mr Davis, “when you have a paradigm change as in 2008, all the models are wrong” is hardly the point. Indeed, by returning to the example of the AA route planner, drivers understand (or should understand) that the alternative quantitative ‘forecasts’ provided are on the grounds that nothing will go spectacularly wrong – say a traffic jam or a car breakdown.

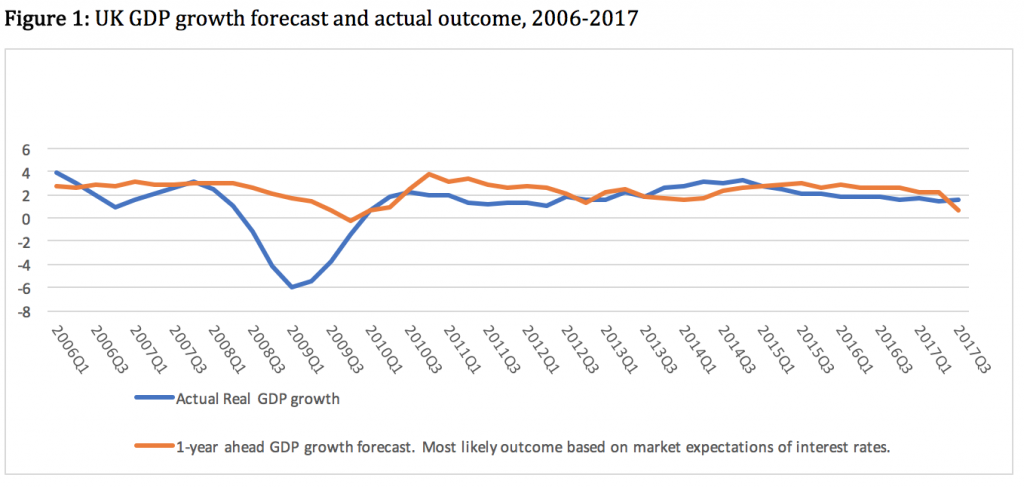

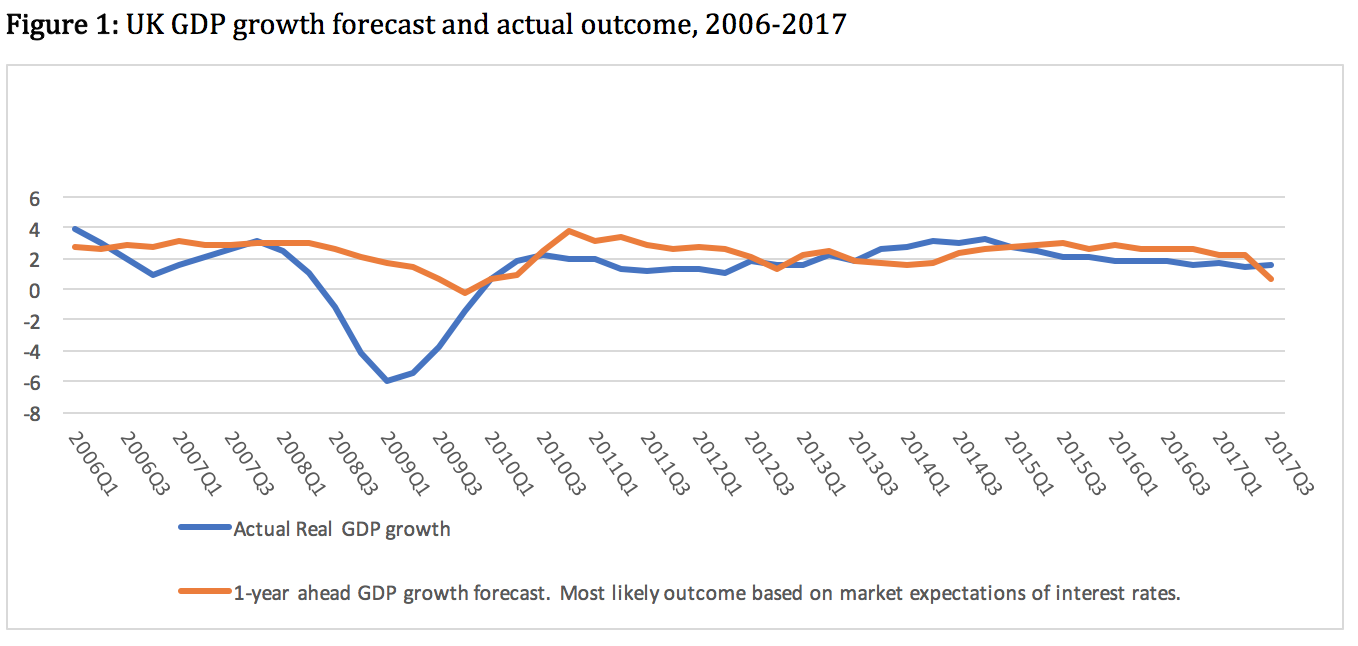

In fact, economic forecasting prior to the recent financial crisis and all the way up to the current time has not gone spectacularly bad. To fix ideas, Figure 1 plots the 1-year GDP growth forecast (this is the ‘mode’, or most likely outcome, based on market expectations of interest rates) produced by the Monetary Policy Committee (MPC) of the Bank of England together with the actual outcome. The MPC has overestimated, since 2006, 1-year ahead GDP growth by 0.8% (based on the Median statistic). Post-financial crisis (2010-2017), however, the MPC’s GDP growth forecast has definitely improved with the ‘Median prediction bias’ dropping to 0.55%.

Source: GDP growth comes from the ONS database. 1-year ahead GDP growth forecast comes from successive Bank of England Inflation Reports.

Source: GDP growth comes from the ONS database. 1-year ahead GDP growth forecast comes from successive Bank of England Inflation Reports.

The main point is that economic forecasters have tried to improve their forecasting performance since the crisis. In fact, the financial crisis triggered a lively debate among policy-makers and forecasters. For instance, the President of the Federal Reserve Bank of Boston, Eric Rosengren, pointed out in 2010 that the seriousness of the crisis was underestimated by economic forecasters because financial links, such as provision of liquidity, to the real economy were “only crudely incorporated into most macroeconomic modeling”. Adding to this, the Head of the Monetary and Economic Department at the Bank of International Settlements, Claudio Borio, noted in 2012 that for most of the post-war period “financial factors had progressively disappeared from macroeconomists’ radar screen”. Building on these very comments, I recently co-authored an academic paper which showed that an empirical model which distinguishes between illiquid and liquid stock market conditions in the UK is able to out-perform the MPC’s GDP growth forecasts.

Obviously, further improvements in our forecasting ability need to be put in place as we move into the complex and indeed challenging Brexit era. Yet, let us not forget that the outcome of the referendum is arguably also based on a ‘quantitative forecast’. Indeed, a 51.9% versus 48.1% vote in favour of Brexit was, in essence, a quantitative forecast of the electorate’s opinion as it was based “only” on a 72.2% turnout.

With this in mind, the pressing question which remains unanswered is the following: why does David Davis appear happy to fully trust the quantitative forecast of the vote but, at the same time, refuse to consider any other UK sectoral forecasts that build on the very Brexit vote? This very lack of information is a serious worry when we try to work out which ‘business model’ is the most suitable to carry forward in our future trading with Europe and the rest of the world.

Costas Milas is Professor of Finance at the University of Liverpool.

All articles posted on this blog give the views of the author(s), and not the position of LSE British Politics and Policy, nor of the London School of Economics and Political Science. Featured image credit: Number 10, Flickr (CC BY-NC)

Professor Milas, thank you very much for making these points, which raise important issues concerning public accountability.

I’d be interested to know if anyone has any references for research on the environmental impact of different Brexit options.

Thought provoking stuff Costas.

Could this be a similar problem to the one facing pollsters at the moment.

That the environment is so volatile that it’s impossible to use established models of measuring data?

No one saw the 2005 crash coming in their impact assessments and forecasting essentially Davis is correct conjecture is just that and always will be.

Even then, any economic modelling (or forecasting) does not exist in a isolation, but instead must also be ralated to all the other forms of impact assessment (ie at a basic level PST as well as E), each of which can be expected to have significant economic implications. So for example any examination of technological implications, whether opportunity or risk, whether the potential value of investment in one or mitigation of the other, should be subject to at least a rough calculation of economic magnitude. Early indications are that any attempt at such cross-referral is also missing. I hope I’m wrong but it seems as if the impact assessments done would gain at best an E in an MBA course.

Where are the EU’s ‘sectoral assessments’ of the likely changes to EU-UK trade patterns that we could test any of our own against then? Where is the EUParliamentary scrutiny o fthe EU’s negotiators andtheir positions?

No matter what ‘impact assessment’ was made it can bear no relation to the political choice to Remain or to Leave. Ignoring that the writers of any assessment would be the same civil servants who authored Project Fear statistics and predictions, none of which stood up to the public’s assessment and were rigthfully seen as risible, any prediction would have to be made on the outcome of a Trade Deal with the EU.

It is alos ridiculous to publish such guess work in negotiations with the EU,

There can be two extreme outcomes

1) Free Trade deal with no connection with EU systems outside the WTO ‘Regulatory Equivalance’ rules

Result ‘No Change’. Imports from EU decline as substitutes at lower prices obtained in world markets are substituted..

or

2) No Trade Deal and imposition of full CET on UK imports.

Result ‘WTO Rules’. Imports from EU decline, as above.

In either case the quality and value of goods exported to EU remain the same as the EU imports the minimum amount of goods from the UK in items it cannot substitute for. The UK’s exports elsewhere are better priced because no longer hamstrung by a ‘reciprocal impost’ to the EU CET.

The EU market has not substituted for these in 42 years and is unlikely to now.

So the assessment’ at anything in between would be how restrictive to the UK trade with parties other than the EU any UK-EU deal /agreement would be. Would this deal be worth the so called ‘settlement’ money the EU is indicating – ie that beyond the UK’s recognised obligations for budgets it participated in setting?.

The smuggled in term that governs the wishful thinking of the Remain camp is that the second scenario is impossible because there would be a trade embargo agains the UK, ie the EU would refuse to sell us stuff and attempt to stop imports. This is illegal both by the WTO rules and against the EU’s own constitutional arrangemnts – especially Article 50.

So the writer’s point is what exactly?