In an interview with Joel Suss, editor of the British Politics and Policy blog, Saskia Sassen discusses the UK’s economic ‘recovery’ and her new book, Expulsions: Brutality and Complexity in the Global Economy. You can watch the video or listen to the podcast of her recent public lecture at the LSE here.

In an interview with Joel Suss, editor of the British Politics and Policy blog, Saskia Sassen discusses the UK’s economic ‘recovery’ and her new book, Expulsions: Brutality and Complexity in the Global Economy. You can watch the video or listen to the podcast of her recent public lecture at the LSE here.

In the UK many are cheering a return to growth and the fall in unemployment that has been faster than anticipated. What is not visible when we report these figures? Do you think the UK has ‘recovered’?

Short answer is that it has recovered for some but is leaving out more and more people, and some types of firms and neighbourhood sub-economies. One question all these statements raise is: what is not being measured when the numbers show growth?

A good bit of the economic numbers rests on a sort of economic cleansing. I use this term to describe the purposeful doing away with the negatives: the long term unemployed no longer counted, the failed small businesses whose owners give up and often commit suicide, the impoverished neighbourhood sub-economies, the impoverished middle classes, the young who have given up finding employment, and more. All of these have been expelled from the space of ‘the economy’. I intend the term ‘economic cleansing’ to resonate with the more familiar and horrifying ‘ethnic cleansing’: I mean it to capture a brutal action and condition, even if affects a small, albeit growing, share of these economies.

A good case to examine this economic cleansing is the announcement by the UK Chancellor, George Osborne, that the UK had become the fastest growing economy in the EU. The UK’s economy has certainly been less devastated than those of Greece and Spain, but what really lies behind these forceful statements about growth and recovery? We might ask, whom does this expelling of the bad news benefit? Not those who have been expelled, and rendered invisible to the statistical and governmental eye. But it does benefit capital owners, who need ‘healthy’ economies so they can invest and make their capital work and therewith deliver profits.

What must be recognized is, first, that GDP per capita is an increasingly problematic way of measuring economic growth. This fact has received considerable attention from experts. What has received less attention is that it fails to measure concentration of benefits and capture at the top nor losses at the bottom. While GDP per capital sounds like it represents the distribution of benefits, it does not so in the current economy. It was a reasonable measure during the Keynesian phase of western capitalism when one of the major forces was the growth of the middle of the distribution – the expansion of a prosperous middle class and working class. We have long left that behind.

Getting back to the UK economy, what jumps out at you?

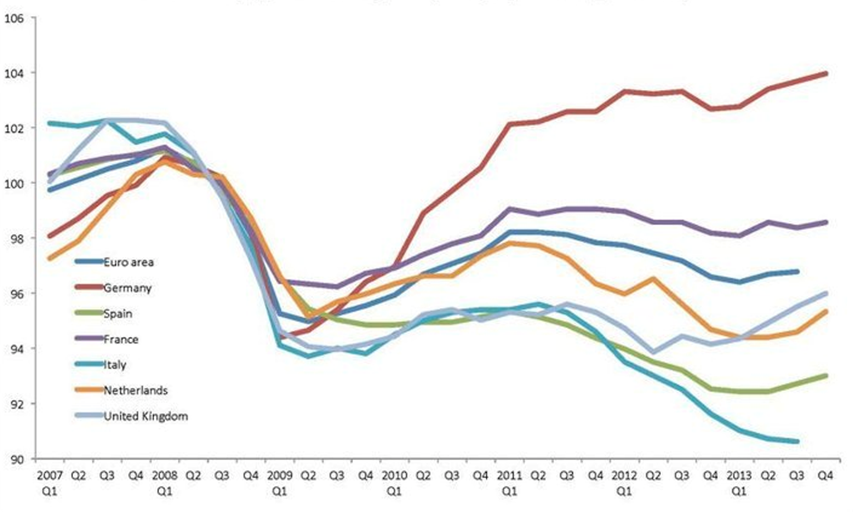

Yes! Even if we accept the facts presented by Osborne that the UK had the highest growth rate in the EU for this quarter, what this statement leaves out is, a) the UK’s growth level is actually one of the lowest given a very low starting point – lower than it was in 2008 [see Figure 1]. b) It is lower than in France, Germany, Japan and the US and is at a far lower than it was in 2008. c) It leaves out the unemployed who have given up looking for jobs and the young who are not even trying to get a job, firms that have simply died, and neighborhood sub-economies that are shrinking. d) Per capita pay, even factoring in the enormous income gains at the top, is 8 per cent down from 2010—a time of (mere!) ‘recovery’ from the crisis.

Figure 1: GDP per capita 2007-2013, select European countries (2008=100)

Source: Office of National Statistics of the United Kingdom 2014. Data can be found here.

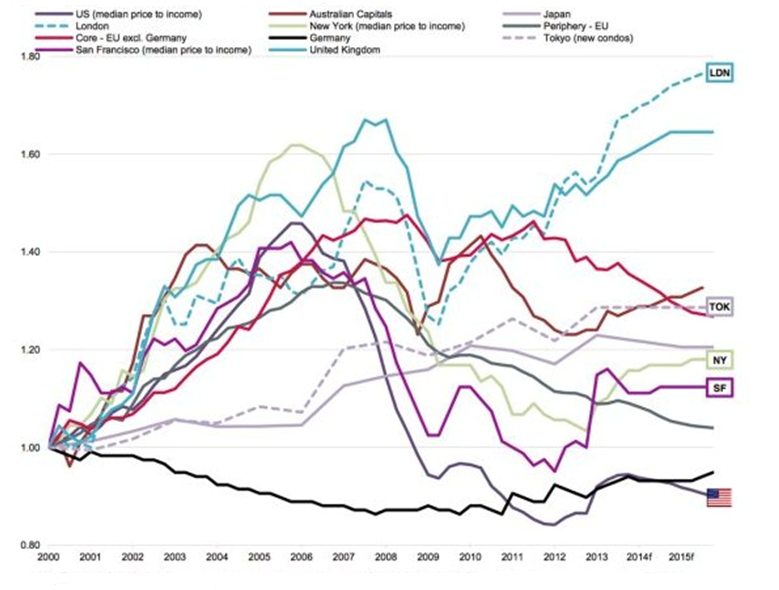

The basic GDP per capita measure also leaves out the fact that more and more British households have growing debts. And so does the government. Finally, it leaves out the skewed character of the housing market, a fairly generalized trend across very different countries, but extreme in the case of the UK. It is well known that London is one of the most expensive housing markets in the world, along with a few other cities around the world [see Figure 2]. Beyond London, the whole of the UK has extremely high housing prices.

Figure 2: Average house price to income ratio, 2000-2015 (base year 2000; forecasts for 2015 and 2016)

Source: Fitch calculations base on multiple country data sets

You’ve described finance as the steam engine of our time, re-shaping space and contributing to the expulsion of many caught up in it. Can you elaborate on the argument you make in your new book?

Saying finance, and I mean high-finance, is the steam engine of our times – rather than choosing the more self-evident information technologies — is a way of alerting an audience to the fact that finance is not simply traditional banking. I develop this in chapter 3 of my Expulsions book. Traditional banking is a service. My way of emphasising the difference is that the traditional bank sells money it has, and its source of gain is the interest on a loan. Finance sells something it does not have, and therein lies its creativity (for instance, the extraordinary algorithms, mostly built by physicists, that are a key to financial trading), and this is also what makes high-finance a danger to an economy because it has to invade other sectors to get the grist for its mill.

In this sense, high-finance is a capability, and as such it can be deployed in multiple ways; finance can financialise just about everything. Once they are done with the high quality items (fancy office buildings, highly valued commodities, high grade debt of all sorts, etc.) it can move to lower quality items (used car loans is a good example of a low quality item). Thus when I say it is the steam engine of our epoch I mean it is present in most sectors of our economy, directly or indirectly.

This is my way of explaining high-finance – If finance is the X, I explain it in non-X terms. Thus I always advise, if you want to understand high-finance do not ask a financier. They will make it difficult to understand and will be telling you about the mechanisms of financial practice, and this is indeed complex.

I argue that to understand the role of finance today we need to describe it from the perspective of the economy. Thus I have also written that insofar as finance can make capital at higher speeds and larger scales than traditional banking, it can be useful. But to be useful it has to be materialized into something useful: a green transport system, social housing, cleanups of vast toxic dumps, and so on. But we have not seen this happen. It would mean citizens and governments seeking to govern high-finance for the common good. Not easy…

Does the spate of new regulations on banks and other financial institutions in the wake of the financial crisis do anything to mediate the capability of high-finance?

When governments, notably the US and the UK, bailed out the banks with citizens’ money under the notion that a crisis of the big banks (which nowadays are mostly about high-finance), would be disastrous for the economy, they were partly right. Why? Because so much of the US and UK economy has become financialised, and is hence continuously at risk given highly speculative financial transactions. But this is only part of the story. The other half of the story is how reasonable sounding government regulations can actually be used for the opposite purpose. The new regulations in the US, for instance, and the new standards of the Basel committee [the Bank of International Settlements based in Basel, Switzerland], which raised the minimum liquidity levels they recommend banks should have – the actual money so to speak, not a derivative. This should have helped banks be better prepared to handle a crisis. But when the US government gave the banks all that cash during the crisis it did not demand that the banks extend (traditional) loans to businesses desperate for loans to fulfill existing orders for their goods, etc.. The banks used the cash for speculative and highly profitable transactions. There is no way they were going to make regular loans to modest firms when they could make super-profits on speculation with the vast new cash influx courtesy of the US citizens. How is it possible that politicians were not aware that financial firms are not interested in traditional loans? They can make much much higher profits by taking the speculative road.

We are often told of the increasing urbanisation of the world’s population in positive terms, but you have identified a more worrying reason behind urbanisation; namely, governments and large companies are buying up and pushing people off land, leaving them little choice of where to go. Can you discuss the use of the term ‘migration’ and how it obscures what are ‘expulsions’?

I am glad you picked up on this. Overseas land acquisitions are rising, with people pushed off their land and into poverty; that’s not migration of people from rural areas fascinated by ‘city lights’, or in search of a better life and all of that. These people are getting expelled from their land by mostly foreign, but not only, mining operations, palm plantations for biofuels, and such. Expulsions are effectively being rebranded as migrations. Where else can people go but cities?

True, the acquisition of land by foreign governments and firms is a centuries old process in much of the world. But I am always interested in how a condition was made, actively made. And hence it is important to understand the different mechanism that led to the specifics of each of these phases of landgrabs in what are often long and diverse histories. The British empire grabbed land in ways that differed from the Spanish way, and today’s firms grab in yet another way.

The most recent phase took off in 2006 – 220 million hectares (about 500 million acres) were acquired between 2006 and 2011 by about 15 governments and about 70 firms. I have a short analysis of this in a recent article for The Guardian, which essentially argues that the term ‘migration’ obscures the fact that our firms and government agencies contribute to expulsions.

Saskia Sassen will be speaking this weekend at the Edinburgh International Book Festival.

Note: This article gives the views of the interviewee, and not the position of the British Politics and Policy blog, nor of the London School of Economics. Please read our comments policy before posting. Featured image credit: Strelka Institute for Media, Architecture and Design CC BY 2.0

Saskia Sassen – Columbia University

Saskia Sassen is Robert S. Lynd Professor of Sociology and co-Chair of The Committee on Global Thought at Columbia University. She also was a Centennial Visiting Professor at the London School of Economics, and has just returned as a Research Fellow in Destin. Her new book is Expulsions: Brutality and Complexity in the Global Economy (Harvard University Press 2014). Other books include Cities in a World Economy (4th ed, Sage 2011), Territory, Authority, Rights: From Medieval to Global Assemblages (Princeton University Press 2008), A Sociology of Globalization (W.W.Norton 2007), and The Global City (2001, 2nd ed). Her website is www.saskiasassen.com and she can be found on Twitter @SaskiaSassen.