The recent housing boom was unprecedented in magnitude and duration. According to Philippe Bracke, the current downward trend of prices is likely to continue. Housing cycles are a normal feature of advanced economies, but policymakers should aim at making these cycles less pronounced. This is particularly relevant for the UK, where house price volatility is substantial.

The recent housing boom was unprecedented in magnitude and duration. According to Philippe Bracke, the current downward trend of prices is likely to continue. Housing cycles are a normal feature of advanced economies, but policymakers should aim at making these cycles less pronounced. This is particularly relevant for the UK, where house price volatility is substantial.

In periods of economic distress it is natural to think in terms of cycles. Reaching the bottom of the cycle is a painful experience but at least gives some hope: from that point onward, things can only get better. UK house prices, however, look still far from their bottom.

In a recent research project for the IMF, I have studied the house price expansions and contractions of 19 OECD countries since the first quarter of 1970, and identified 55 expansions (of which 6 are ongoing) and 62 contractions (of which 13 are ongoing). On average, expansions last 6 years and produce a 60% house price increase in real terms; contractions last 4 and a half years and produce a 30% real price decline.

These numbers give the impression that real house prices are increasing in the long run, because expansions are longer than contractions and entail bigger absolute price changes. If one removes the most recent house price boom from the sample, however, this impression largely disappears. Other studies, which have a more restricted geographical focus but a broader temporal window, show that over the centuries real house prices are fundamentally flat. (Piet Eicholtz, for instance, has studied three centuries of house price data for the Herengracht canal in Amsterdam and has found their average real annual growth has been fairly low, at about 0.5%).

If there is such a thing as a pattern for house prices in the long term, it is not that they are increasing; it is that they are cyclical. All the countries I examine in my research have gone through multiple expansions and contractions of national house prices. These fluctuations are not just due to randomness – in the paper I show that the probability of ending a house price expansion increases with its duration. In other words, longer expansions are more likely to terminate: what goes up has to come down.

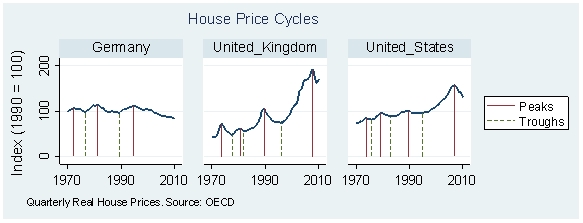

What does this mean for the UK? Figure 1 below shows the real house price index and the corresponding peaks and troughs for three countries of my sample: Germany, the UK, and the US.

Figure 1

A couple of things stand out from the chart. First, the last house price boom did not involve all countries. There are a few cases of advanced nations, like Germany (or Japan), which did not experience any substantial price increase. For Germany in particular, over the last 40 years real house prices have stayed constant or declined slightly. Once again this is proof that real house price growth should not be taken for granted, even in productive and well-functioning economies.

Second, if history is any guide, countries like the UK and the US will continue experiencing real house price declines for some time. This adjustment process is already under way. According to the Land Registry, nominal house prices in England and Wales are down 2.6% on a year-on-year basis. Taking into account an inflation rate of 5%, real house prices have fallen by almost 8% in the last 12 months. However, there is surely potential for more substantial drops, especially considering that US house prices (which have grown less than in the UK during the boom) have already fallen by more than 30% from their peak.

Third, and most importantly, while some degree of up-and-down in house prices is unavoidable, the range of these oscillations should be carefully monitored. Ups and downs are an intrinsic feature of all economic series but booms and busts are not, and this is where the UK compares unfavourably with other countries. Even by US standards, UK house prices look like a rollercoaster: they more than doubled in real terms since the mid nineties; before that, they fell by almost 40% from 1989 to 1995.

For prices to vary so much, quantities must be very sticky. Indeed, a recent OECD working paper shows that the number of new housing units built in the UK is low compared to other nations. A report by the Department of Communities and Local Government suggests that strict planning regulations hold back housing supply and make prices more volatile. Let’s hope therefore that the current debate on planning reform will provide solutions that go in the right direction.

It might seem strange to advocate more house building in a period where house prices are falling. However, the current decline in house prices represents a cyclical adjustment that is not due to abundance of housing units. If this were the case, we wouldn’t see the current rent increases.

Please read our comments policy before posting.

Thanks for your comment. Let me be precise: I’m not saying “let’s have a programme to build and sell houses”. This would be misleading, especially if referred to declining areas of the country.

I’m talking about the removal of excessive regulatory barriers to new developments. In a less restrictive regulatory environment, it is obviously up to the builders and investors to decide whether to supply new houses.

I note your paper doesn’t refer to the seminal work done by Prof Morgan Kelly of UCD on this topic, which had the advantage of predicting the housing busts we have seen. It’s not clear whether a programme of trying to build and sell depreciating assets makes sense: who is to bear the capital losses? Better is to encourage more rapid adjustment – which will depend on reducing the size of the average mortgage granted – not the gross amount of finance available.