Global demand for construction materials has risen substantially over the past decades. To keep global warming below 2°C, demand for steel and cement must peak by 2030 and fall below 2010 levels by 2070. The construction industry must make longer-lasting buildings and substitute low-carbon materials for high-carbon ones. Nikolaus Hastreiter, Antonina Scheer, Beata Bienkowska, and Simon Dietz (Transition Pathway Initiative, at LSE’s Grantham Research Institute on Climate Change and the Environment) write that the circular economy should be adopted as a comprehensive approach incorporated into each stage of these materials’ life cycles. In the short and medium-term, investing in zero emissions technologies in parallel to deploying circular economy solutions will be necessary to set construction materials on the path to a low carbon future.

For an answer to the question in the title, you can look at heavy industry. Global demand for construction materials like cement and steel has risen substantially over the past decades and is expected to continue growing (International Energy Agency, 2020a). The cement and steel sectors are big energy consumers and emitters of greenhouse gases; together they account for nearly 17% of global CO2 emissions. (Assuming global CO2 emissions of 36.8 gigatonnes (Gt), cement emissions of 2.4 Gt, steel emissions of 3.7 Gt.) They are also sectors where greenhouse gas emissions are particularly difficult to abate. The Transition Pathway Initiative showed in a recent report that only a minority of cement and steel producers are currently on track to keep the global temperature rise to below 2⁰C. Moreover, the few companies with ambitious long-term climate commitments mostly lack corresponding ambition in the shorter term. Only one out of five leading cement companies that are aligned with a 2⁰C emissions pathway in 2050 is also aligned in 2030.

Investors and regulators should be wary of backloading emissions reductions until mid-century, as it creates the risk that companies will leave themselves too much to do at the end, like a runner leaving too big a gap to the leaders to catch up and win the race. In the long term, beyond 2030, green hydrogen, low-carbon fuels and zero emissions technologies like carbon capture and storage (CCS) are likely to be key in helping cement and steel companies reduce their emissions (International Energy Agency, 2020a). But in the short term (and beyond), the concept of the circular economy offers concrete solutions to drive emissions down.

The circular economy aims to transform the current linear economic system into one that is based on ‘designing out waste and pollution, keeping products and materials in use, and regenerating natural systems’ (Ellen Macarthur Foundation). It is governed by three R’s: Reduce, Reuse and Recycle. In the construction materials sector, this approach has great potential to lower emissions by bringing together producers, intermediate manufacturers and end users, and by strengthening collaboration between sectors. A net zero future cannot be achieved if all sectors’ decarbonisation pathways remain siloed.

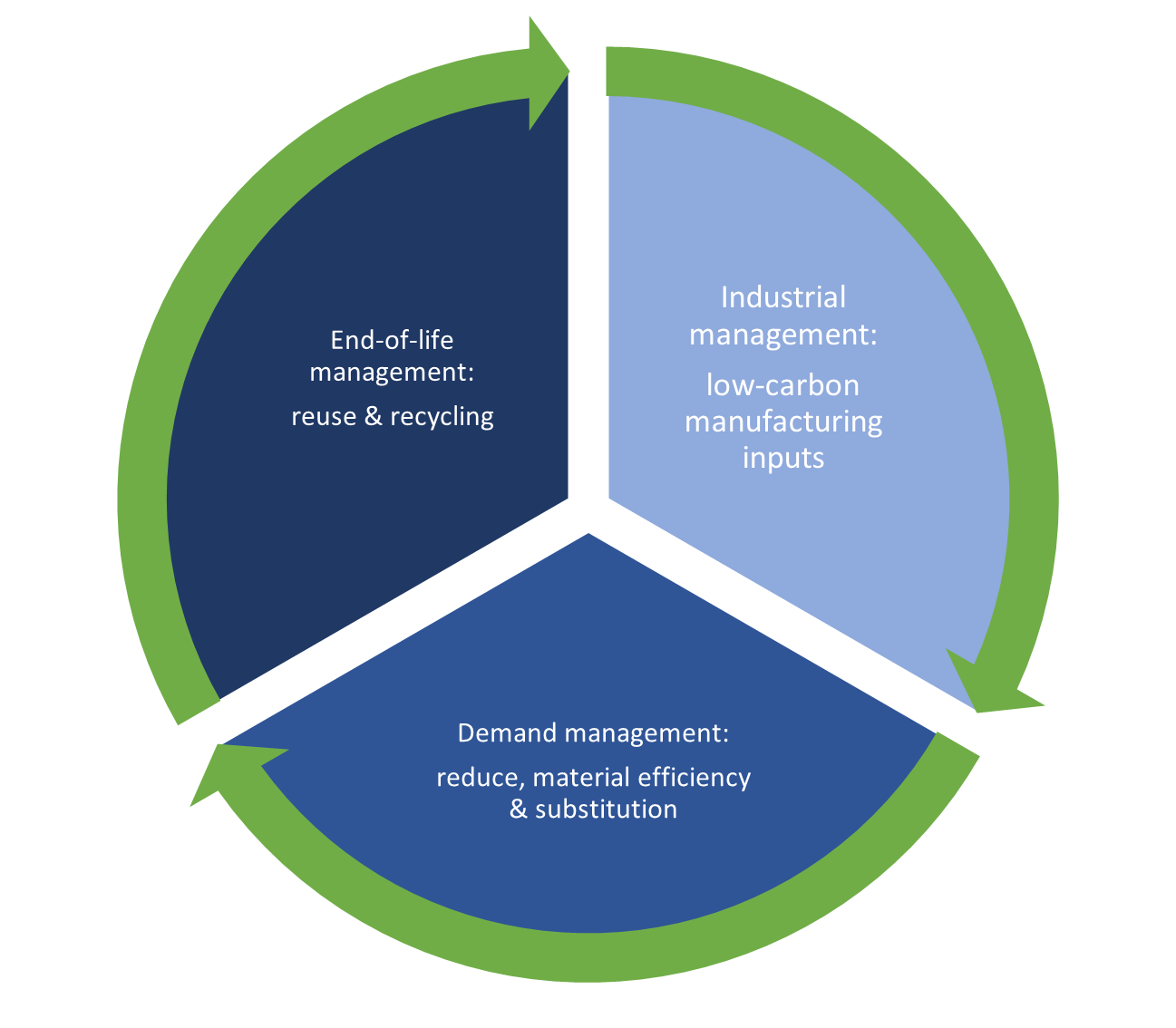

Figure 1. Circular economy components discussed here

Industrial management – harnessing cross-sectoral collaboration: The circular economy unlocks cross-sectoral collaboration by making one sector’s waste into another’s industrial input. For example, cement producers could partially substitute clinker with steel blast-furnace slag and coal ash. Since clinker is the most carbon-intensive input of cement production, this would reduce emissions substantially. These waste materials could replace 15-25% of clinker in Europe (Material Economics, 2018). Meanwhile, waste fuels from other sectors, like tyres and paint residue, could replace coal and petcoke in cement kilns.

Demand management – engaging the construction sector: To keep global warming below 2°C, demand for steel and cement must peak by 2030 and fall below 2010 levels by 2070 (International Energy Agency, 2020a). The construction sector consumes 50% of global cement production and 30% of global steel production, therefore its demand will need to decrease. From the perspective of construction companies, emissions from manufacturing these materials are upstream Scope 3 emissions. These emissions can be lowered through material efficiency measures, most importantly through making longer-lasting buildings by, for example, creating more modular spaces and prioritising renovation.

In addition, high-carbon construction materials could also be substituted with low-carbon ones. Cross-laminated timber, if sourced from sustainable forestry, has a much lower emissions intensity, and offers better opportunities for reuse and energy recovery (Ramage et al., 2017). Pioneering projects include the completed Mjøstårnet tower in Norway as well as the W350 project in Tokyo to build a 90% wooden skyscraper by 2041.

Figure 2. The tallest timber building

Note: Mjøstårnet is an 18-storey mixed-use building in Brumunddal, Norway, completed in March 2019. It is currently the world’s tallest timber building. Source: Image by NinaRundsveen, under a CC-BY-SA-4.0 licence, via Wikimedia Commons.

End-of-life management – reuse and recycling of materials: When buildings come to the end of their lives, the reuse and recycling of cement and steel are the shared responsibility of the materials and construction sectors. Steel-based structural elements can often be reused in new construction and otherwise recycled to make secondary steel. Global steel recycling rates are impressively high at 85% but can be pushed above 90% by targeting end users and regions with weaker recycling practices and infrastructure (International Energy Agency, 2020b). Recycling scrap steel is much less emissions-intensive than primary steelmaking.

Recycling cement is more challenging. Mixed with water, cement binds sand and gravel to form concrete. This chemical reaction is irreversible. However, new ideas to recycle cement and its components are materialising (Material Economics, 2018). The start-up SmartCrushers has developed a technique to recover unreacted sand, gravel, and cement from crushed concrete rubble with promising results. It is also possible to explore reusing concrete components at buildings’ end-of-life. Lendager, a pioneer in this field, built a residential area in Copenhagen by reusing abandoned walls from rural dwellings.

Interestingly, concrete re-absorbs CO2 from the surrounding air over its lifetime in buildings through recarbonation. Increasing the exposed surface area of concrete leads to increased CO2 absorption. Hence, it is recommended to expose crushed concrete to the air for several months before reusing it, for example, as road underlay. Up to 25% of the lifecycle emissions of cement can be reabsorbed through such recycling methods.

Towards a balanced decarbonisation future

None of these measures can decarbonise steel and cement in isolation. The circular economy should be adopted as a comprehensive approach incorporated into each stage of these materials’ life cycles. Not only do various measures and technologies need to be implemented, but relevant actors throughout the construction supply chain must be involved. In the short and medium-term, investing in zero emissions technologies in parallel to deploying circular economy solutions will be necessary to set construction materials on the path to a low carbon future.

♣♣♣

Notes:

- The post gives the views of its authors, not the position of LSE Business Review or the London School of Economics.

- Featured image: collage of six photos. Clockwise from top left: Cement circle, by Patrick Hendry on Unsplash; Construction skyline by C Dustin on Unsplash; Mass timber exterior wall by Anders Vestergaard Jensen on Unsplash; Indoor renovation, by Milivoj Kuhar on Unsplash; Mass timber indoor, by KK Law on naturallywood.com, under a CC-BY-NC-2.0 licence, via University of British Columbia media relations; Scrap metal, by David Hofmann on Unsplash

- When you leave a comment, you’re agreeing to our Comment Policy

{kind=link}