It is now roughly seven years since the Greek economic crisis first emerged, but why has the crisis in Greece proven so difficult to address in comparison to other Eurozone countries? Based on an analysis of crisis management in several European states, Stefanie Walter writes that because internal reform and a euro exit were particularly costly options for Greece, it opted for a path of reforming only as much as is necessary to retain outside funding. As this strategy is unlikely to be viable indefinitely, the crisis will remain unresolved for the foreseeable future.

It is now roughly seven years since the Greek economic crisis first emerged, but why has the crisis in Greece proven so difficult to address in comparison to other Eurozone countries? Based on an analysis of crisis management in several European states, Stefanie Walter writes that because internal reform and a euro exit were particularly costly options for Greece, it opted for a path of reforming only as much as is necessary to retain outside funding. As this strategy is unlikely to be viable indefinitely, the crisis will remain unresolved for the foreseeable future.

Like a neverending story, the Greek crisis has hit the news again in recent weeks. After seven years, the crisis still awaits a resolution. The Greek economy has yet to enter a recovery, the IMF insists that Greece needs more debt relief, and the possibility of a Greek default and possible eventual exit from the Eurozone – a ‘Grexit’ – still cannot be entirely ruled out, even if the immediate threat of this has receded over the last year. Why has it been so difficult to resolve the crisis?

The Greek crisis was caused by huge deficits in the country’s budget and current account, which means that the country had been consuming much more than it had been producing for a long period of time. When the crisis hit, rebalancing the economy became an urgent issue. Faced with the option to default on its debt, to leave the Eurozone, or to implement tough austerity measures and reforms in return for financial support from abroad, Greece chose the latter strategy.

But rather than implementing serious structural reforms that would end privileges for politically well-connected groups and would make the economy competitive, policymakers predominantly relied on austerity measures that chiefly hurt politically less influential groups, such as the young and the poor. Moreover, it only implemented the minimum of measures needed to receive continued financial support from abroad.

In a recent study of crisis politics in Europe, I show that this type of crisis management is typical for countries that find both austerity/structural reforms (internal adjustment) and a devaluation of the currency (external adjustment) costly courses of action. Policymakers in countries that exhibit such a ‘vulnerability profile’ fight tooth and nail to avoid any serious reforms as long as possible.

Crisis management in these countries is difficult: political turmoil and public protests abound. Reforms are delayed. Support from outside, typically the IMF, is usually called in to cover the financing needs that the lack of resolute crisis management generates. And when policymakers cannot avoid implementing reforms in return for this outside support, they usually design these reforms in a way that shields their own voters and targets those that lack political influence.

Crises are much easier to resolve through swift and substantial reforms when one reform strategy is clearly less costly than another. Take the Baltic states in 2008/9: Faced with a similar crisis as Greece, governments in these countries slashed public spending and fired thousands of public employees. This resulted in serious recessions, during which unemployment more than tripled, but also resolved the crises rather quickly.

Because these countries had a relatively sound fiscal basis and flexible labour markets, this internal adjustment strategy was much less costly than the alternative, giving up their pegged exchange-rate to the euro. A devaluation of the currency would not only have put the goal of entering the Eurozone in question. It would also have significantly increased the debt burden of the large majority of individuals and firms who had borrowed in euros, rather than their national currency. Given this vulnerability profile, Baltic policymakers were able to implement these drastic measures quickly and without major public protests.

Crisis resolution was also easier in Poland, where lowering the exchange rate was much less costly than austerity and internal structural reforms. As a result, the country immediately allowed its currency to depreciate when pressures mounted in the wake of the Lehman Brothers collapse in 2008.

Why reforming Greece is so difficult

In contrast to the Baltic and Polish cases, both external and internal adjustment strategies are associated with very high costs in Greece. Given the immense deficits in the budget and current account, the austerity needed in Greece to rebalance remains huge. Entrenched and clientelistic structures make reforms of the Greek economy politically difficult. Internal adjustment has hence been challenging. The alternative, however, an exit from the Eurozone, is also an extremely risky and costly strategy, and one that has been deeply unpopular among Greeks.

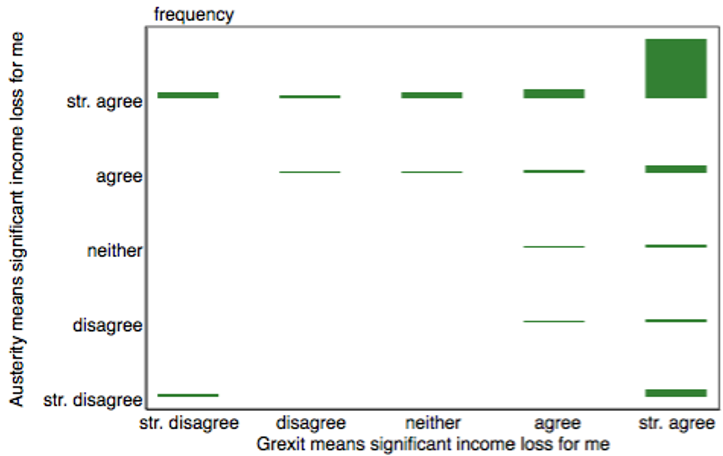

Greek voters’ perceptions about the consequences of different crisis resolution strategies illustrate this difficult situation. In a survey that I jointly conducted in December 2015 with Elias Dinas, Ignacio Jurado, and Nikitas Konstantinidis, 59.7% of respondents stated that they expected significant income losses both if the government implemented the austerity measures agreed with creditors, and if the country were to leave the euro (see figure 1).

This leaves them between a rock and a hard place: No matter how the government tries to resolve the crisis, they understand that they will be hurt. This explains why the government has been trying to implement only the bare minimum required to get continued financial support from outside and, hopefully, some debt relief.

Figure 1: Perceptions about the consequences of austerity and leaving the euro in Greece

Note: UoM poll conducted on 2-6 December 2015; Dinas, Jurado, Konstantinidis and Walter (2015)

Why creditors continue to support Greece

So why is Greece continuing to receive financial support from outside? European policymakers are struggling to achieve two main goals: safeguarding the irreversibility and stability of the Eurozone and protecting their own banks and taxpayers’ money. To achieve these goals, they have lent the country huge sums of money to keep it financially afloat and in the Eurozone, while demanding austerity and deep reforms in return.

But to date, they have been unwilling to either let Greece default or to grant substantial debt relief. This approach to manage the Greek crisis has drawn a lot of criticism and debate. What is clear is that the lack of decisive action and the willingness to push painful decisions down the road have proven detrimental for Greece.

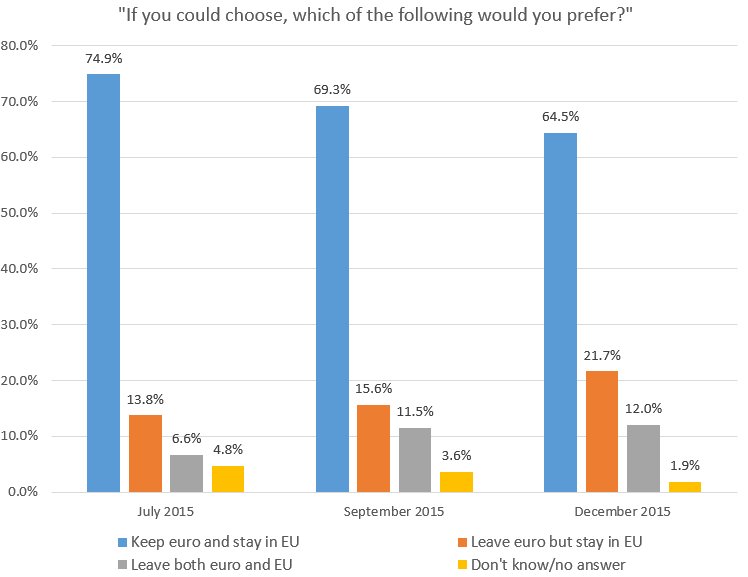

Despite numerous protests and riots, the repeated election of a populist left government, and a referendum against the conditions associated with a bailout package, the euro is still popular in Greece. But support for the euro is declining. Figure 2 shows more survey evidence that my collaborators and I collected in Greece during 2015. As the crisis dragged on, voters seemed to realise that Greece will not be able to remain in the Eurozone without a substantial reform of its economy and continued austerity. Support for the euro dropped by more than ten percentage points over the course of only a few months.

Figure 2: Preferred future course for Greece (July – Dec 2015)

Note: Polls conducted on 4 July 2015, 7-8 September 2015 and 2-6 December 2015

As long as creditors are willing to finance Greece’s financial needs at the bare minimum it needs to survive, and as long as a majority of Greeks want to stay in the Eurozone, the crisis is unlikely to be resolved quickly. If a majority of Greeks start to prefer a return to the drachma, however, the crisis could quickly escalate one last time.

Please read our comments policy before commenting.

Note: This article gives the views of the author, and not the position of EUROPP – European Politics and Policy, nor of the London School of Economics. Featured image credit: herolx (CC-BY-SA-2.0)

Shortened URL for this post: http://bit.ly/2dHyvqD

_________________________________

Stefanie Walter – University of Zurich

Stefanie Walter is full professor for international relations and political economy in the Department of Political Science at the University of Zurich, and the author of “Financial Crises and the Politics of Macroeconomic Adjustments” (Cambridge).