Steve Keen argues that neoclassical economists have a blind-spot when it comes to the role of private debt in macroeconomics. They should be worried by the incredibly high UK levels and be seeking ways to avoid the next crash.

As a car driver, you have surely had the experience of changing lanes and being beeped by a car with which you were about to collide—but which you didn’t see before the lane change. It’s because the car was clearly visible in your rear-view mirror, but that part of the image fell on your retina’s blind-spot—so you didn’t see it. Fortunately most of us learn that we have a blind spot, and so we check carefully to avoid being fooled by it again—and causing an avoidable accident.

If only economists could learn the same way, we might not now be in the accident of this never-ending economic crisis. “Neoclassical” economists (who dominate both academic economics and policy advice to governments) have a blind-spot about the role of private debt in macroeconomics, yet despite the economy crashing once before because of it during the Great Depression, they continue to argue that it’s irrelevant now—during this latest crash.

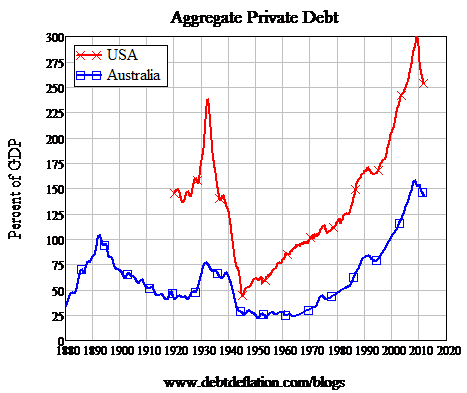

First, let’s establish that there was indeed a “car in the rear view mirror” in the 1930s and today. Data on long-term private debt levels is difficult to find, but I’ve located it for both the USA from 1920 till today, and for Australia from 1880 (see Figure 1). Clearly, there was a debt bubble before the Great Depression, and a plunge in debt levels during and after it (and Australian data also shows the same phenomenon during an earlier bubble and crash in the Depression of the 1890s; see Fisher and Kent 1999). The same process is clearly afoot again now.

Figure 1

Now for the blind-spot. Anyone not blessed—or rather cursed—by an economics education might think there was something in that coincidence of debt and depressions. But it’s nothing to worry about, leading neoclassical economists assure us—thus confirming that either they know something profound that proves that the coincidence is irrelevant, or that they have a blind-spot which means that their judgment can’t be trusted.

The profound insight they believe they have is that the level of debt doesn’t matter, and that only the distribution of debt can be important. Ben Bernanke rejected Irving Fisher’s “Debt Deflation” explanation for the Great Depression on this basis; after noting that Fisher did influence Roosevelt’s policies, Bernanke added that:

‘Fisher’s idea was less influential in academic circles, though, because of the counterargument that debt-deflation represented no more than a redistribution from one group (debtors) to another (creditors). Absent implausibly large differences in marginal spending propensities among the groups, it was suggested, pure redistributions should have no significant macro-economic effects…’ (Bernanke 2000, p. 24)

One crisis later, leading neoclassicals like Paul Krugman continue to argue that only the distribution of debt can matter:

People think of debt’s role in the economy as if it were the same as what debt means for an individual: there’s a lot of money you have to pay to someone else. But that’s all wrong; the debt we create is basically money we owe to ourselves, and the burden it imposes does not involve a real transfer of resources. That’s not to say that high debt can’t cause problems — it certainly can. But these are problems of distribution and incentives, not the burden of debt as is commonly understood. (Krugman 2011)

So can we ignore the level of private debt? No—because this “profound insight” is in fact a blind-spot about the role of banks and debt in a capitalist economy. Neoclassical economists treat banks as irrelevant to macroeconomics—which is why banks are not explicitly included in their models—and regard a loan as merely a transfer from a saver (or “patient agent”) to a borrower (or “impatient agent”), as in Krugman’s “New Keynesian” model of our current crisis:

In what follows, we begin by setting out a flexible-price endowment model in which “impatient” agents borrow from “patient” agents, but are subject to a debt limit. (Krugman and Eggertsson 2010, p. 3)

With that model of lending, a change in the level of debt has no inherent macroeconomic impact: the lender’s spending power goes down, the borrower’s goes up, and the two changes roughly cancel each other out.

However, in the real world, banks lend to non-bank agents, giving them spending power without reducing the spending power of other non-bank agents. The difference between the neoclassical model of lending and the real world is easily illustrated using transaction tables. Figure 2 illustrates the neoclassical model (with an implicit banking sector): in this world, a change in the level of debt has no macroeconomic implications.

Figure 2: Neoclassical perspective on lending

| Assets | Deposits (Liabilities) | ||

| Action/Actor | Patient | Impatient | |

| Make Loan | +Lend | -Lend | |

Figure 3 illustrates what actually happens: the bank creates a new deposit and a new loan simultaneously, adding to Impatient’s spending power without reducing Patient’s.

Figure 3: Real-world lending

| Bank Assets | Bank Deposits (Liabilities) | ||

| Action/Actor | Patient | Impatient | |

| Make Loan | +Lend | -Lend | |

This case has been made theoretically and empirically by non-neoclassical economists for decades. Schumpeter argued it was the primary source of investment (Schumpeter 1934, p. 73), Basil Moore showed empirically that this endogenous creation of credit, and not the “money multiplier”, was the explanation for money growth (Moore 1979), and most succinctly, a Senior Vice-President of the New York Fed asserted it when arguing against the monetarist experiment of the 1970s:

In the real world, banks extend credit, creating deposits in the process, and look for the reserves later. (Holmes 1969, p. 73)

Unfortunately, neoclassicals continue to ignore it because it doesn’t fit their model. Well it’s time to ignore them—because their model doesn’t fit the real world. Once we take the endogenous creation of money by banks into account, rising debt has a macroeconomic impact because it adds to aggregate demand. It also is the primary way in which speculation on asset prices is financed, as Minsky emphasised (Minsky 1982, p. 24).

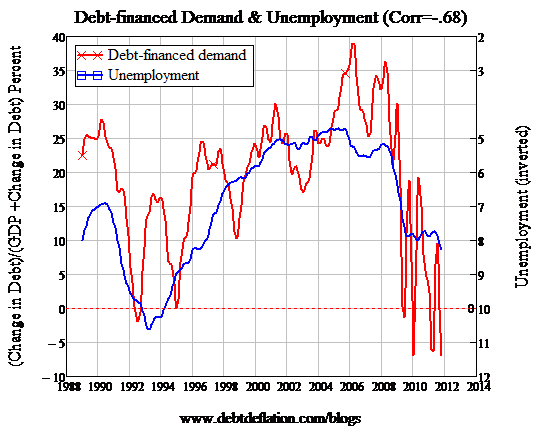

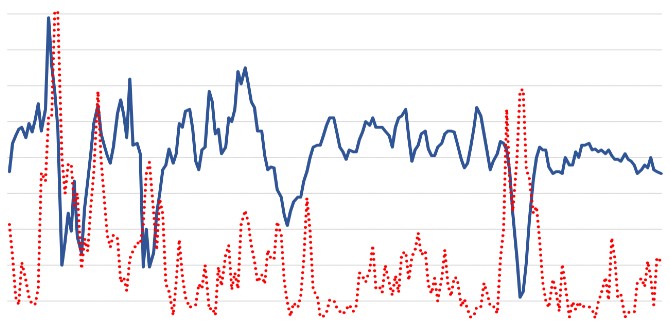

The crisis we are in suddenly becomes entirely explicable—and predictable before the event—when the blind-spot on debt is removed. Because the change in debt adds to aggregate demand (and is spent on assets as well as goods and services), there is a strong causal link between rising debt and both falling unemployment and rising asset prices. This is evident in the UK data: unemployment fell as the debt-financed component of aggregate demand rose, and unemployment is now rising as the growth in private debt subsides (see Figure 4, where unemployment is inverted to make the correlation more obvious).

Figure 4: Change in Debt & UK Unemployment

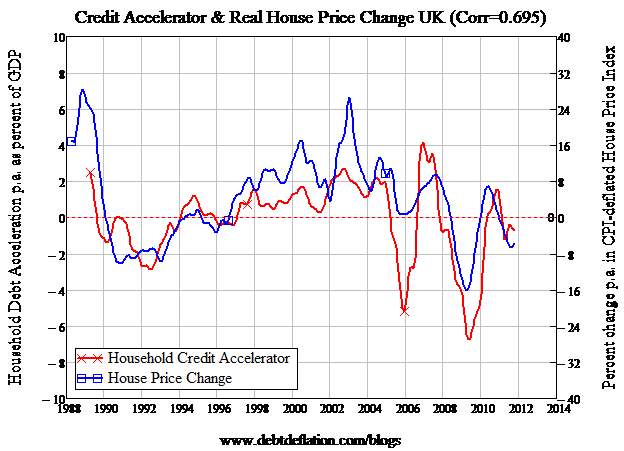

The reason that our economic crisis is a financial one as well is that changing debt drives not just demand for goods and services, but asset prices as well. And since changing debt is a major source of demand for share and property purchases, for asset prices to rise, the level of debt must not merely grow but accelerate. Accelerating household debt clearly drove the UK’s property bubble, and that bubble is now vulnerable as household debt decelerates (see Figure 5).

Figure 5: Relationship between accelerating household debt and change in house prices

Ignoring the role of private debt in the economy is thus as dangerous as driving a car while ignoring the fact that your vision has a blind-spot. It’s why neoclassical economics has to be consigned to the dustbin of history, and a realistic, credit based economics must take its place.

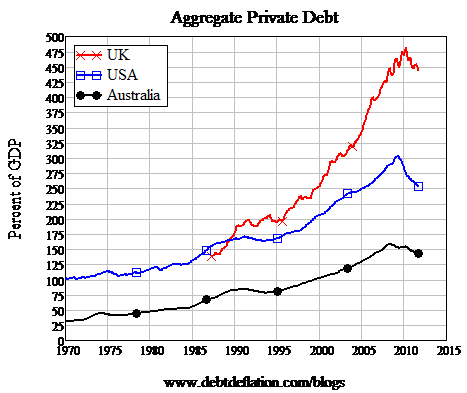

Oh, and as passengers in the UK economic car, are you hoping that your economists are better drivers? Figure 6 shows the level of UK private debt compared to that of the USA and Australia. I suggest that you tighten your seat-belts.

Figure 6: Aggregate private debt level

Note: This article gives the views of the author, and not the position of the British Politics and Policy blog, nor of the London School of Economics.

Please read our comments policy before posting.

Steve Keen is Professor of Economics & Finance at the University of Western Sydney, and author of the popular book Debunking Economics, a second edition of which has just been published (Zed Books UK, 2011; www.debunkingeconomics.com). He will be delivering a public lecture at the LSE on 3 April 2012. Steve blogs at http://www.debtdeflation.com/blogs/ and is on Twitter: @ProfSteveKeen.

I am reminded of sitting in a film class populated by English literature grad students being introduced to post-structuralism. They came to watch movies. It was implicit that everything they’d learned was suddenly useless. Worse than useless because it all had to be unlearned. They were angry. The part that bugged me was no one ever suggested there were ‘schools’ of thought. Just the one true way. We were all cheated.

Great post. Very informative. I liked it very much.

Hi Steve,

I think it would be clearer in the neo-classical lending versus real world lending table if you also included some asset i.e. neo-classical would have -realThing, +realThing as this is the basis of the transaction, a real exchange. That seems the key distinction from the real world. That is implied but without that explicitly, I think you can argue that in the real world the + of the bank asset is transferred through bonuses and bank salaries to the equivalent of the Patient.

Hi Steve

What you say is of course dead right as far as it goes. however the ‘impatient’ borrower doesnt hang onto the credit he is advanced but uses it to buy a house of whatever. as a result the bank’s liability to the borrower becomes a liability to the vendor or the vendor’s bank. both sides of banks’ balance sheets grow. by 2007 the size of uk bank balance sheets had grown to 500% of gdp from around 70% in 1964. i have grabbed a chart of debt for g10 countries off facebook whcih i can email you. it shows debt divided into government debt, house hold debt, non financial, and financial. the thing that stands out is that it is only in the financial sector that the uk (at over 600% of gdp) really stands out from other G10 countries. Does the term ‘private debt’ include financial sector debt?

Steve, I’m one of these cursed economics graduates, but find your analysis far more convincing than any of the other main stream economists. Probably that is because I’ve since dropped economics and moved into a more real science based enviroment, an enviroment were evidence always trumps assumptions.

I would be very interested in reading a rebuttal from somebody like Krugman, or even Bernanke 🙂 . Can you point me to anything?

The best mainstream economists can usually do is use reactionary rhetoric against Keen, without much substance:

http://www.australianreview.net/digest/2001/08/davidson.html

However, Arnold Kling has a somewhat thoughtful review, even if he does argue that deregulation didn’t cause the crisis in it (!):

http://econlog.econlib.org/archives/2011/10/of_bunk_and_eco.html

some other GMU professors also have a decent review of the first edition:

http://www.gmu.edu/depts/rae/archives/VOL16_4_2003/6_BR_Murphy.pdf

Robert Vienneau has more reviews and responds to them:

http://robertvienneau.blogspot.com/2006/07/response-to-comments-on-steve-keens.html

It’s why neoclassical economics has to be consigned to the dustbin of history, and a realistic, credit based economics must take its place.

Public or private is beside the point that applies to all. There is no such thing as a realistic credit that a person, a company, a bank, a government or society at large would grant to itself.

In simple terms, borrowing is live now pay later. The blind spot is the impossibility of paying later for as long as the fact of the matter is that exponential growth into a finite space fails to compute.

“creation of money by banks” means that there is nothing to back to promise to pay later that any sort of money is , no gold reserve, no collateral, no consideration to part with apart from the promise itself, a pot of gold at the end of the rainbow.

“Neither a borrower, nor a lender be; for loan oft loses both itself and friend, and borrowing dulls the edge of husbandry.”

— (Hamlet, Act I, Scene 3)