The Private Finance Initiative has been used to build 127 hospitals and facilities but has also locked the NHS into decade-long contracts paying back debt at very high interest rates. Is there a way out? Vivek Kotecha analyses some of the options that are available to policymakers to address the problems caused by existing PFI schemes.

The Private Finance Initiative has been used to build 127 hospitals and facilities but has also locked the NHS into decade-long contracts paying back debt at very high interest rates. Is there a way out? Vivek Kotecha analyses some of the options that are available to policymakers to address the problems caused by existing PFI schemes.

In our previous blog on the subject of the Private Finance Initiative (PFI) we explained that whilst it may be difficult to tackle the existing legacy of such schemes in the NHS there were options available to government. Building on this work, we have published a report on these options, with the intention of providing a potential “toolbox” for policy makers.

Our starting point was to recognise that the PFI deals insulated the lenders and equity investors from the risk that any future government may renege on the original agreements or seek to renegotiate them. This has meant that irrespective of the extreme budgetary constraints on local authorities and NHS Trusts, as well as the shrinking amount of money available for schools, hospitals and social care, they are still required to make annual payments to the PFI companies.

These guaranteed payments provide PFI companies and their lenders with substantial returns in the form of profit and interest which are in excess of returns on projects with similar risks. They also lock public authorities into contracts for 25-30 years for cleaning and facilities maintenance services, and sometimes require that they make payments for buildings which are no longer needed. The ultimate end point for dealing with the legacy of these deals in the public sector is therefore to reduce the cost of the debt repayments, end excess profiteering, and allow public bodies to break the contracts.

But how can this be achieved? Our view is that a range of policy tools need to be employed to bring those shareholders and their lenders (typically investment funds and banks) to a point where a re-negotiation of the original PFI arrangements is in their interest.

To start with, part of the burden of the high cost of PFI debt needs to be taken away from individual trusts and be borne by central government. One of the most pernicious aspects of PFI in the NHS is the extent to which local health economies are required to service high cost loans effectively imposed on them by the Treasury as a means for keeping public sector investment off the nation’s balance sheet. Servicing this debt distorts resource allocation at local level, meaning that cash which could go to patient care is instead diverted to loan repayments.

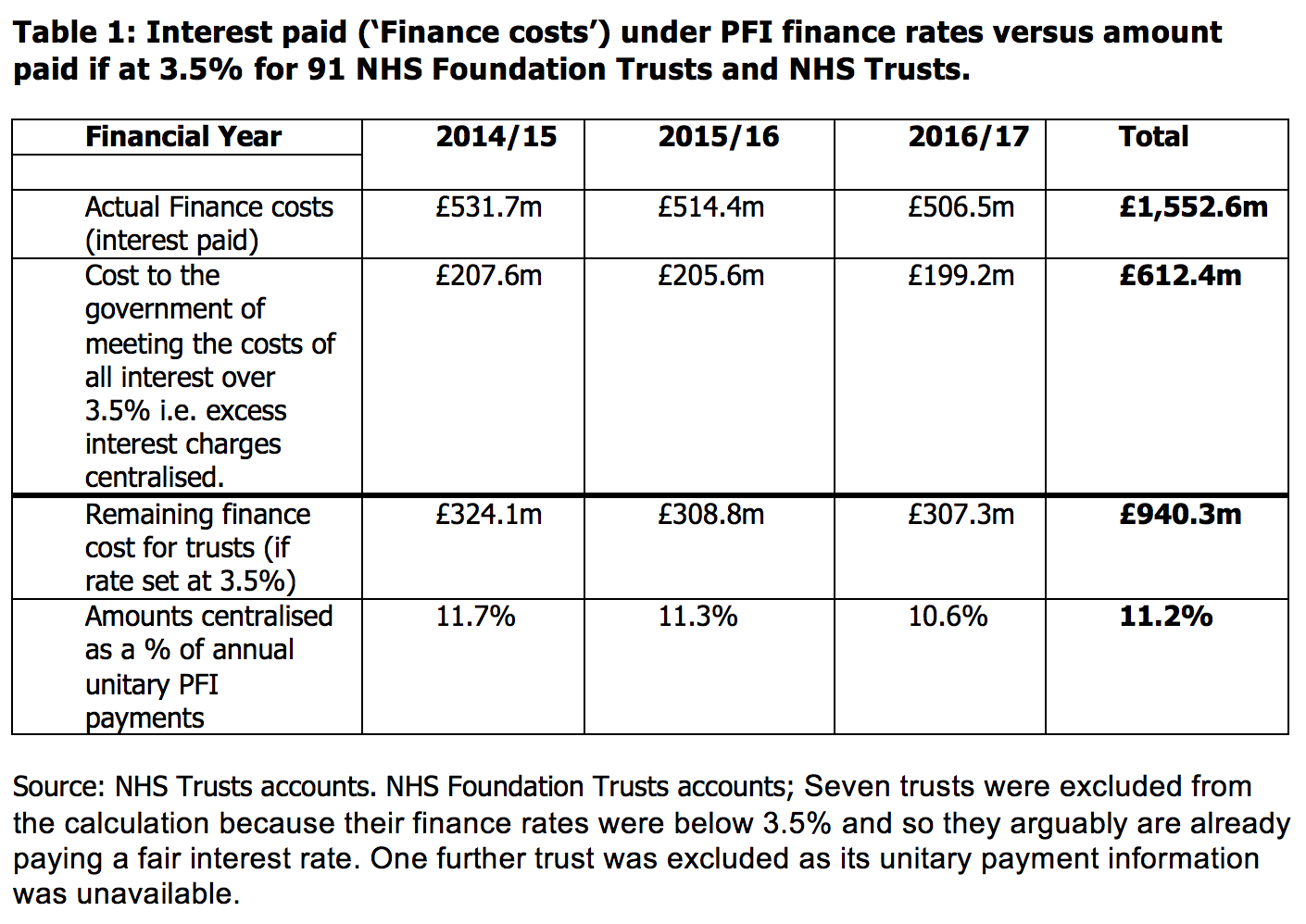

This doesn’t mean that all of the PFI debt would be centralised. Instead we propose removing the additional borrowing costs associated with PFI. For fairness we assumed that the cost of providing services and the cost of building were still paid for by the NHS trust that benefits from them. However, the interest charge attached to the PFI debt under this proposal is capped at 3.5%, which is the borrowing cost of publicly-funded equity from the Department of Health and Social Care. With an average interest rate of 7.0% for NHS PFI schemes, this effectively halves the amount of interest paid by trusts, with the remainder being paid for centrally (Table 1). In addition some of the PFI deals have debt repayments rising with inflation – a very unusual feature compared to ordinary loan repayments which fall due to inflation over time.

Over the three years from 2014/15 to 2016/17 the amount of excess interest and inflation that would have been paid from the centre and not by trusts totals £1.3bn. In 2016/17 the size of PFI costs centralised, £400m, would reduce the deficits of those trusts by 30%, a significant and arguably equitable improvement to their financial ability to provide healthcare. By centralising the ‘excess’ debt element of all PFI schemes, this then places central government departments in a position to engage with the PFI industry as a whole rather than to leave any attempts at renegotiation down to individual NHS trusts.

Enhance the monitoring and enforcement of PFI contracts

The first tool we consider for engendering a renegotiation is enhanced contract and performance management of PFI contracts by the NHS. The public sector has been too passive in managing and enforcing PFI contracts with evidence that insufficient data is collected to assess performance and too few specialist staff tasked with holding the private sector to account under the PFI contract. Deductions can be levied on PFI contracts for underperformance on the services provided (e.g. cleaning, maintenance) or for parts of the building being unavailable.

The data in our report shows that in 2016/17 NHS trusts made £17m of deductions for PFI underperformance and unavailability – 2% of the total PFI payment made in the year. We estimate that if all trusts with PFI schemes made deductions at a similar level to the highest performing trusts then it would save the NHS £29m a year.

This could be achieved more easily by pooling contract management staff regionally, or by supplier, but is hindered by a significant minority of trusts who don’t have standardised PFI contracts, which makes enforcement harder. The savings are small compared to the financial challenges facing trusts but this approach has the potential to yield a greater reward in the long-term: consistent underperformance by a PFI operator gives the trust the right to terminate the contract early.

We recognise that the termination of PFI contracts is a costly affair, but this is likely to depend on how it is done. We model two options in our report. The first looks at the affordability of the approach taken by Northumbria Healthcare NHS Foundation Trust which terminated and bought out the Hexham Hospital PFI scheme using a loan from a local authority. Current Treasury and Department of Health and Social Care policy actively dissuades Trusts from pursuing this route.

Terminate PFI contracts

The second option is to terminate the contract on the basis that the contractor has consistently underperformed. The data shows that termination due to a default by the PFI operator is a potential option for a number of trusts with 16 NHS trusts (15% of all NHS hospitals with PFI schemes) saying that they had had the right to terminate their PFI contract in the last 3 years. In one case, the threat of early termination allowed the Trust to take the 25-year-long outsourcing of services out of the contract, giving it greater flexibility and significant financial savings.

Another of these NHS trusts, Tees Esk and Wear Valleys NHS Foundation Trust, won the right to terminate its PFI contract in June 2018. What we do not know at this stage is the cost of this option to the Trust and what type of arrangements will result from the termination. Certainly the standard contract terms were designed to place a financial obstacle in the way of termination by requiring large compensation payments by the public sector. Irrespective of this, the threat of termination and the fact that so many NHS Trusts have been in a position to terminate shows that the public sector is in a much stronger negotiating position than previously thought.

Tax the profits of PFI companies

The third tool available to government is to use their tax raising powers to limit the extent of profit-making by those with equity stakes in the deal. We’ve previously estimated that a windfall tax which returned the corporate tax rate paid by PFI companies back to the 30% anticipated when signing the contracts would yield £106m for NHS PFI schemes from 2016-2020. This is a relatively small amount compared to the overall costs of PFI and there could be legal challenges along with profit shifting to avoid any tax. However, it could be used as a credible threat to encourage a renegotiation of the price paid for PFI services given the relatively small number of equity investors in PFI schemes.

Nationalise the PFI companies in order to renegotiate the debt

The final option, and the most radical, is nationalising the PFI operating companies. This proposal envisages the state buying out entirely the equity stakes, taking on the responsibility for all existing service contracts and then using state ownership to renegotiate the debts of the former PFI companies (which typically make up over 90% the cost of PFI to the public sector). If the interest rates on these debts can be successfully renegotiated down, this would generate significant savings. In addition, state ownership might lead to the eventual termination of outsourcing services as part of the contract, although this will require negotiations with those companies who are currently contracted to deliver cleaning and maintenance services.

Whilst all this is possible, it will require a government with a large majority to get such a controversial measure through parliament. The level of compensation proposed (£2.6billion for all public sector PFI contracts) will almost certainly be disputed in the courts and it is uncertain how readily lenders will be willing to renegotiate debts without further legislation. That said, this option should remain on the table as a way of demonstrating a determination and a commitment to resolving the legacy of PFI schemes.

In conclusion, whilst none of the options presented are perfect there is also no excuse for inaction. PFI contracts were drawn up in such a way so as to insulate investors against adverse actions by future governments. But, given the small number of owners and lenders to PFI schemes, the use of tax powers alongside the threat of termination and nationalisation could encourage renegotiation in favour of the public sector. Certainly, no rational investor in a PFI deal would welcome the additional costs and prolonged uncertainty associated with fending off these threats if deployed strategically by policymakers.

_____________

Note: the above draws on CHPI’s report, available here.

Vivek Kotecha is Research Officer at the Centre for Health and the Public Interest. He

All articles posted on this blog give the views of the author(s), and not the position of LSE British Politics and Policy, nor of the London School of Economics and Political Science. Featured image credit: Pixabay, Public Domain.

CHPI’s report contains serial inaccuracies, omissions and misunderstandings in it presentation of the proposal to nationalise the Special Purpose Vehicles. You can see the original proposal by Helen Mercer and Dexter Whitfield, together with an annex providing a detailed analysis of CHPI’s report here;

https://www.gre.ac.uk/about-us/news/articles/2017/a-solution-to-controversial-pfi-deals

Great article Vivek. Something has to be done about this very unpleasant legacy of Gordon Brown.