By 2035, airlines will see new revenues from e-commerce, advertising and premium content services in the sky, writes Alexander Grous.

By 2035, airlines will see new revenues from e-commerce, advertising and premium content services in the sky, writes Alexander Grous.

‘Disruption’ is one of the buzzwords that defines our economy at the moment. While much of the focus has been on entrepreneurial start-ups – soliciting early funding for the next ‘the Airbnb of…’ – taking a look at how more established businesses are responding to the technological revolution is just as interesting. Aviation is one such sector that is worth exploring. After all, within 20 years, the equivalent of today’s global population will be carried in the air annually.

We are all familiar with screens in the back of seats as the traditional form of inflight entertainment, serving us up a selection of movies, TV shows and video games for view and use as we traverse the globe. However, with today’s travellers increasingly looking to access the same always-on services they use every day whilst flying – whether that’s work emails or social media platforms or online shopping sites – the demand for secure, high-quality in-flight Wi-Fi is growing rapidly.

On the back of strong passenger demand, it is anticipated that inflight internet will be ubiquitous on commercial aircraft by 2035. Indeed, some studies show that it is quickly becoming one of the top decision-making factors when choosing an airline – creeping up behind concerns about price and flight times, but ranking ahead of loyalty programmes.

Currently 3.8 billion passengers fly annually, but only 53 out of an estimated 5,000 airlines worldwide offer inflight broadband connectivity. This is often of variable quality, with patchy coverage, slow speeds and low data limits. Using International Air Transport Association (IATA) passenger traffic data and forecasts of growth, including a near doubling of passenger numbers to 7.2 billion annually, this study, ‘Sky High Economics’, sets out to comprehensively model and forecast the socio-economic impact of the connectivity. Crucially, for the first time, this study defines the commercial opportunities of high-quality inflight broadband over a 20-year period both to the airlines and the wider ecosystem of suppliers.

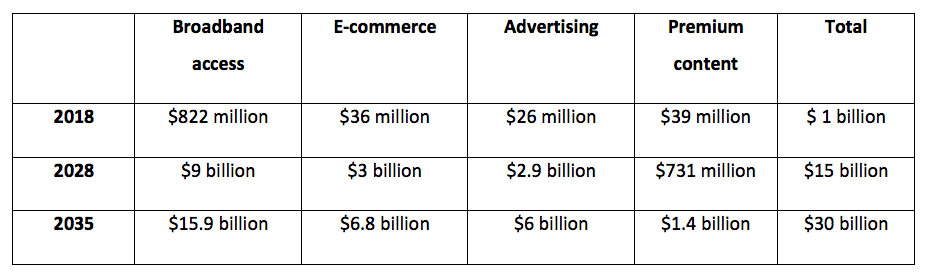

Drawing on quantitative and qualitative sources alike, the study builds on many years of research in this areas, culminating with dedicated effort over the past 12 months to create a complex model of 16,000 lines. The research forecasts broadband-enabled ancillary revenue streams will reach an estimated $30 billion for airlines by 2035. This sits with a total forecast market of $130 billion by this period. From a regional perspective, Asia Pacific has the highest figure at $10.3 billion, followed by Europe with $8.2 billion, North America with $7.6 billion, Latin America with $1.9 billion, Middle East at $1.3 billion and Africa with $0.58 billion.

‘Traditional’ ancillary services such as seat upgrades, on-board duty free and baggage fees are currently worth around $60 billion to airlines but by factoring high-speed broadband into the equation, the research predicts that airlines will benefit from four new revenue streams:

- Broadband access charges – providing connectivity to passengers inflight

- E-commerce and destination shopping – making purchases on-board aircraft with expanded product ranges and real-time offers

- Advertising – pay-per-click, impressions, sponsorship deals with advertisers

- Premium content – providing live content, on demand video and bundled W-IFEC access

This research contrasts other material available in its granularity, breadth and socio-economic approach, drawing on both specific attributes for countries and passenger segments to create demand conditions, whilst also building the supply side factors utilising publicly available data such as aircraft growth from major manufacturers and IATA regional passenger growth forecasts. The forecast airline split of the $30 billion broadband enabled ancillary revenue opportunity across the four categories is:

From the data, it’s clear that the immediate and main source of revenue in this market will come from broadband access – confirming that airlines will be able to generate near term returns from access fees alone; propelling the case for deploying the requisite technology. By 2035, we see that this access revenue is forecast to remain the highest single source of new ancillary revenues, accounting for 53 per cent of the total market – this amounts to an extra $4 per passenger head. Today, traditional ancillary revenues deliver $17 per passenger.

Connectivity transforms the cabin into a marketplace. It’s only a matter of time until we see innovative content deals struck, partnerships formed and a well-developed ecosystem of products and services available, all with the passenger’s satisfaction and entertainment in mind. Data generated by passengers while in-flight is also create a whole other field of opportunity and engagement for savvy airlines and their partners.

Making the most of the opportunities presented by a connected cabin with high quality continuous internet coverage will, however, depend on airlines having the right kit and adopting more of a consumer-orientated, retailer mind-set. They will need to seek out and be open to third party suppliers and engage with them in a new way for many. Ultimately, if airlines can embrace, a ‘sky high’ multibillion dollar opportunity exists for the global airline industry that can transform the existing passenger experience and in the process, deliver additional ancillary revenue enabled by on-board connectivity.

- This blog post is based on the author’s Sky High Economics – Chapter One: Quantifying the commercial opportunities of passenger connectivity for the global airline industry and first appeared at the LSE Business Review.

- Featured image credit: Photo by Thomas Hawk, under a CC-BY-NC-2.0 licence

Please read our comments policy before commenting.

Note: This article gives the views of the author, and not the position of USAPP– American Politics and Policy, nor of the London School of Economics.

Shortened URL for this post: http://bit.ly/2zUzzXc

_________________________________

About the author

Alexander Grous – LSE Media and Communications

Alexander Grous is a lecturer and researcher in the Department of Media and Communications at LSE, and has also worked in the Department of Management and Centre for Economic Performance, since 2007. He co-teaches MC435 Disruptive Digital Worlds: Competing Economic and Political Economy Explanations and on LSE Executive Programmes and Summer School in Digital, Social Media, Management, Transformation, Regulation, and other areas. Dr Grous also directs research projects within LSE Enterprise and undertakes applied advisory work for major clients including Microsoft, Warner Brothers, BBC, Amadeus, BSkyB, BMC, GB Group, Barclays, RBS, Motorola, Inmarsat, WBX Group, and others, with numerous high profile reports published. Dr Grous has also developed and teaches on Management and Digital programmes in Spain as the academic lead, and has been an advisor to the Government of Bizkaia and Gipuzkoa in the Basque Country on socioeconomic reform and digital political campaigning. Dr Grous brings considerable international industry experience to LSE in previous CEO and VP roles in e-commerce, Internet, P2P, satcoms/telecoms, FMCG, Broadcasting and Fashion, in global companies, including Lockheed Martin, PepsiCo, Telstra, BBC, and others. He has also held turnaround roles in FinTech’s, and SMEs in Digital Rights Management, P2P, and Micropayments.