By Riccardo Crescenzi (LSE), Marco Di Cataldo (LSE, Ca’ Foscari University of Venice), and Mara Giua (LSE, Roma Tre University).

By Riccardo Crescenzi (LSE), Marco Di Cataldo (LSE, Ca’ Foscari University of Venice), and Mara Giua (LSE, Roma Tre University).

Global capital markets are increasingly competitive and the attraction of Foreign Direct Investment (FDI) has taken centre stage in public policies world-wide. Nowadays countries with no active Investment Promotion Agencies (IPAs) are only a small minority in the world (OECD, 2015). In addition to national IPAs, whose competence covers an entire country, sub-national IPAs have also become the norm across the globe. The activity of IPAs is now an essential component of both national and local government strategies to attract inward investment. National and sub-national IPAs registered at the World Association of Investment Promotion Agencies (WAIPA) have increased from 112 in 2002 to 170 in 2018.

IPAs are increasingly popular tools leveraged by national and sub-national governments to attract foreign capital in both advanced and emerging economies. However, the evidence base supporting this relevant (and expanding) area of public policy intervention remains rather limited. Some studies have estimated positive IPA impacts in advanced economies (Bobonis and Shatz, 2007; Charlton and Davis, 2007), while others have instead suggested that impacts materialise only in developing economies where red tape and bureaucratic barriers to investors are predominant (Harding and Javorcik, 2011; 2012; 2013).

However, this debate fails to consider the large (and increasing) heterogeneity between and within national economies in terms of FDI location drivers and investment promotion efforts. It has become apparent that major market failures, preventing the optimal allocation of capital, have emerged within (rather than between) countries both in advanced and emerging economies. The national-level focus of previous studies, together with the omission of sub-national investment promotion efforts, has so far masked relevant insights for public policies targeting global capital flows.

A recent Working Paper by LSE’s Riccardo Crescenzi, Marco Di Cataldo and Mara Giua revisits the question of the impact of IPAs to explore: a) the capability of national-level investment promotion efforts to deal with the heterogeneity of host economy characteristics both between and within countries; b) the impact of sub-national IPAs, designed to leverage (or compensate for) this heterogeneity in investment conditions. Their research, focused on economies that are part of the same EU Single Market (with stringent constraints on tax incentives and anti-competitive behaviour), has made it possible to minimise the influence on FDI location decisions of national-level factors other than IPA efforts. When looking within countries, these confounding factors become even less relevant.

The paper leverages a newly-developed ad hoc survey on both national and regional (i.e. sub-national) IPAs for a large number of European countries. Figure 1 shows the coverage of the IPA survey: areas in green are covered by the national IPA survey while areas in blue are covered by both the national and regional IPA survey. This dataset makes it possible to capture, for the first time, the full institutional architecture of the investment promotion efforts that is indeed highly diversified across countries. The specification of within-countries models by sub-national units and sectors makes it possible to better control for confounding factors that might affect between-countries estimates and capture the heterogeneity of impacts.

Figure 1 – National and Regional Investment Promotion Agencies in Europe

Our survey unveils a significant heterogeneity among the different models of investment promotion in Europe. Some countries have adopted a centralised system with no regional agencies (e.g. Greece); other countries rely on both national and regional agencies (in all regions, e.g. Poland, or only in some, e.g. Italy). Other countries have only regional agencies (e.g. Belgium).

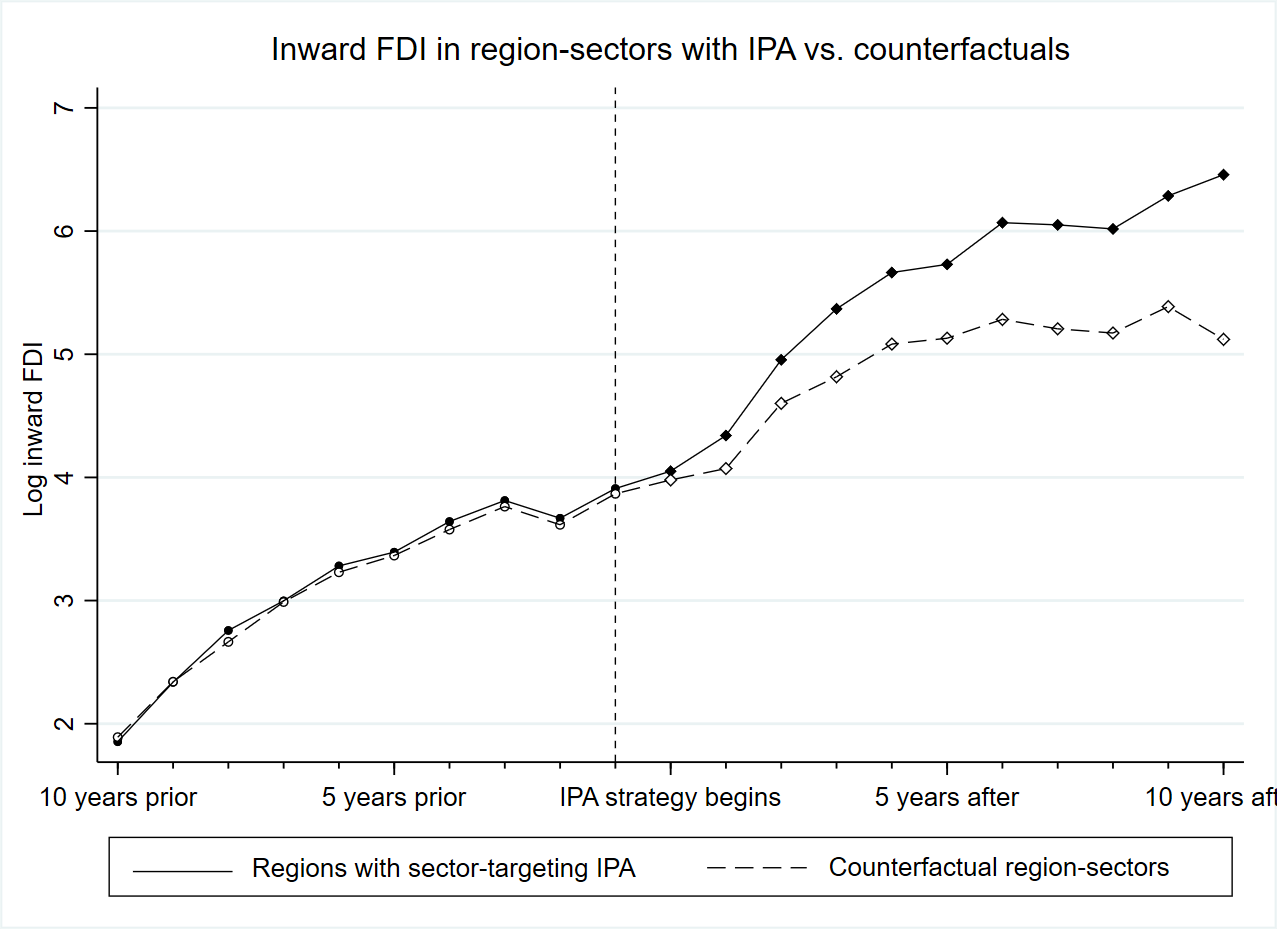

The results of the counterfactual study (addressing the problem of the non-randomness of the investment sectors chosen by the agencies for FDI attraction by means of difference-in-differences and synthetic controls) suggests that national IPAs have a limited role to play, either between or within countries. Conversely, sub-national IPAs effects (analysed for a selected sub-group of the sample) on the inflow of FDI are positive: sectors targeted by regional IPAs attract higher shares of greenfield FDI, after the strategy has been introduced, vis-à-vis region-sectors that are never targeted by a regional IPA (Figure 2). Regional IPAs contribute to increasing the probability of receiving FDI and boost the amount of total foreign investment received as well as the jobs directly created by the investment.

Figure 2 – graphical evidence from counterfactual analysis

Regional IPAs are local organisations closer to the investor and its surrounding environment, and this proximity makes it possible for them to effectively influence investment operative conditions. The capacity of regional IPAs to influence FDI inflows by removing investors’ operational bottlenecks is confirmed by the concentration of the estimated impact in the less developed regions of the sample, where information asymmetries and institution failures are more widespread. This finding suggests that, in attracting FDI towards less developed areas, sub-national IPAs act as compensation for malfunctioning institutions and inadequate information diffusion mechanisms. IPAs in less developed regions increase the probability of attracting foreign capital by up to 14% on average, increase the inflow of investment by 71% and the number of jobs created by 102% on an annual basis. The estimated effect corresponds to an additional 17 million dollars in greenfield FDI and 98 new jobs per year per each investment sector, on top of what would have been received/created in the same region in absence of the agency.

When looking across sectors within less developed regions, the impact is concentrated in knowledge-intensive sectors where collaborative systemic conditions are more relevant to the success of the investment. As information asymmetries are unlikely to vary across sectors within the same local economy, this finding may suggest that the capacity to create a supportive environment on the ground is complementary to the capacity to address information asymmetries highlighted by the existent literature on IPAs. The stronger attractive capacity in knowledge intensive sectors identified in our results offers support for the hypothesis that the highest returns from investment promotion efforts come from the removal of practical bottlenecks to investors’ operations. This suggestive evidence is also coherent with the explanation that regional IPAs are more effective than national IPAs thanks to their proximity to investors’ operations on the ground.

The novel results produced in this paper have relevant implications for public policy, in particular given the increasing attention of policy makers for the attraction of global capital flows. IPAs are viable tools to attract FDI even in advanced economies. However, investment promotion is a multi-layered architecture that involves both national and sub-national organisations. In advanced economies with integrated capital markets, sub-national regional IPAs play ceteris paribus a key role in FDI attraction. Investment promotion policies should be focused around the organisational layer closer to the actual investment and its environment in order to remove the operational barriers to the activity of foreign investors where they emerge. Knowledge intensive FDI are identified as those relying more on the connectivity between foreign investors and domestic firms and institutions, therefore benefitting the most from the improvement of the local business ecosystem triggered by IPAs. These findings seem to suggest that the devolution of responsibilities for investment promotion in favour of less developed regions may be a viable policy option to improve their attractiveness to foreign investors, and, possibly, to stimulate their economic development.

Read more in the authors’ paper published in the Journal of International Economics (2021): “FDI Inflows in Europe: Does Investment Promotion Work?”

References

Bobonis, G. J. and H. J. Shatz (2007), ‘Agglomeration, Adjustment, and State Policies in the Location of Foreign Direct Investment in the United States’, Review of Economics and Statistics 89, 30–43.

Charlton, A. and N. Davis (2007), ‘‘Does Investment Promotion Work?’’, B.E. Journal of Economic Analysis & Policy 7, 1-21.

Crescenzi R., Di Cataldo M. and Giua M. (2019) FDI inflows in Europe: does investment promotion work? LSE-Institute of Global Affairs Working Paper #9/2019

Harding, T., and B. Javorcik (2011). “Roll out the Red Carpet and They Will Come: Investment Promotion and FDI Inflows.” Economic Journal 121 (557), 1445–76.

Harding, T. and B. Javorcik (2012). “Foreign direct investment and export upgrading”, Review of Economics and Statistics 94 (4), 964–80.

Harding, T. and B. Javorcik (2013). ‘Investment Promotion and FDI Inflows: Quality Matters’. CESifo Economic Studies 59: 337–59.

The authors are part of the ERC GILD (Global Investments and Local Development) Team at the LSE

Riccardo Crescenzi is a Professor of Economic Geography at the London School of Economics.

Marco Di Cataldo is an ERC Post-Doctoral Researcher at the London School of Economics and a Research Fellow at Ca’ Foscari University of Venice.

Mara Giua is an Assistant Professor (tenure-track) of Economic Policy at the Roma Tre University (Italy) and a Visiting Fellow at the London School of Economics.

If the local conditions, resources and environments match MNCs’ strategy, MNCs will invest. Investment promotion doesn’t necessary work as many governments’ policy-makers around the world believe. Many economists in many investment promotion agencies fail to acknowledge strategic management viewpoint from global companies. That’s why I agree with this article.