The UK will soon vote on whether to end its 43-year membership in the European Union. Opinion polls suggest the vote is too close to call, with the “stay” and “leave” side switching leads on a regular basis, and this uncertainty is reflected in swings in the stock market, explains Nicholas Bloom. Using data from the Economic Policy Uncertainty Index, he explains why the uncertainty could be having a material negative impact on the UK’s economic performance.

The UK will soon vote on whether to end its 43-year membership in the European Union. Opinion polls suggest the vote is too close to call, with the “stay” and “leave” side switching leads on a regular basis, and this uncertainty is reflected in swings in the stock market, explains Nicholas Bloom. Using data from the Economic Policy Uncertainty Index, he explains why the uncertainty could be having a material negative impact on the UK’s economic performance.

The very real risk the UK will leave the European Union, possibly leading to a massive economic disruption, has led to heightened stock market and exchange rate volatility; swings in opinion polls lead to swings in the FTSE 100 and the value of the Pound. Every time the “leave” vote surges, the stock market and pound sink as markets price in a higher risk of a post-Brexit economic downturn.

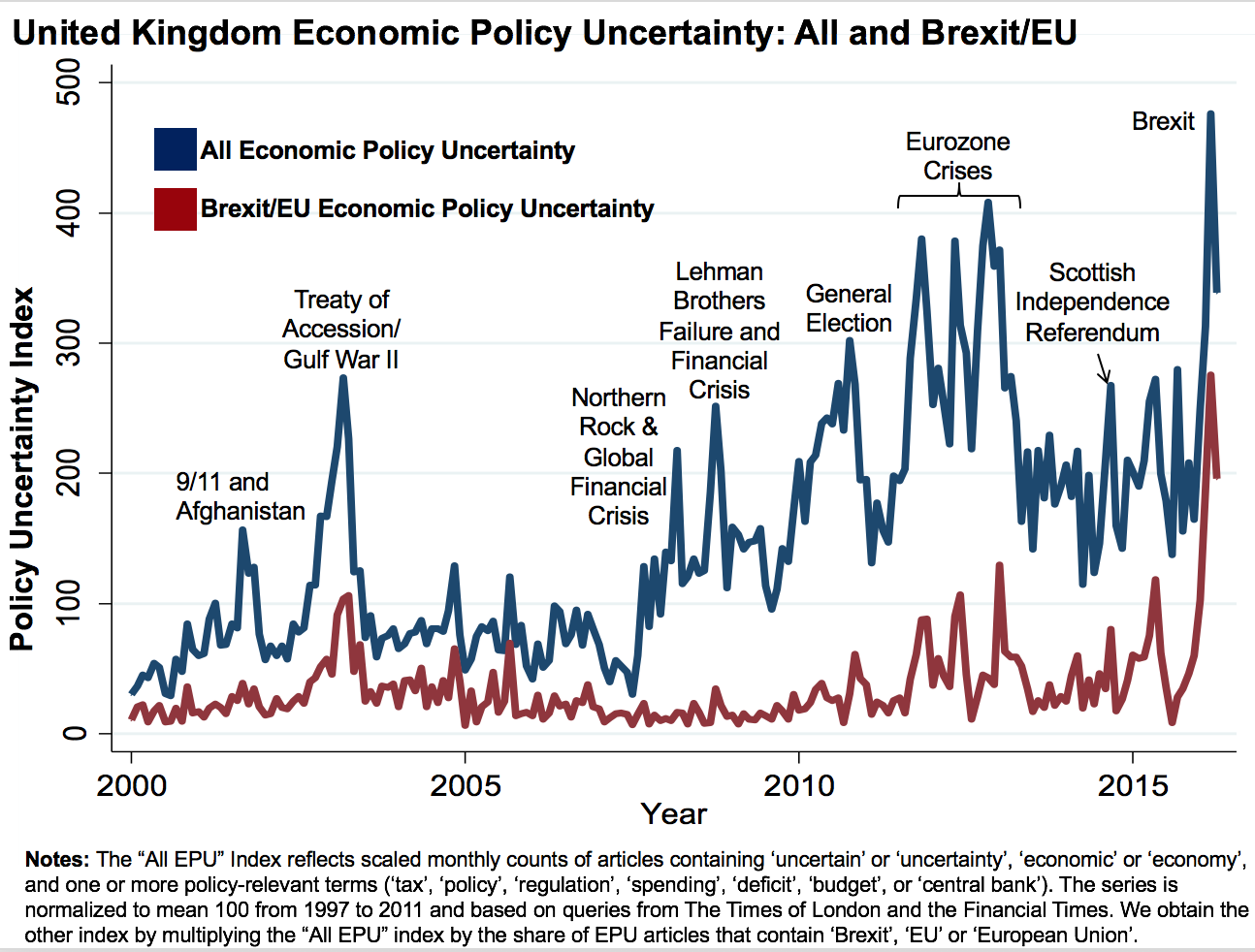

We are tracking uncertainty related to the Brexit vote using our Economic Policy Uncertainty (EPU) Index. This index reports the share of newspaper articles in the Financial Times and Times of London that discuss Economics (proxied by the words “economy” or “economic”), Policy (proxied by “tax”, “policy”, “regulation”, “spending”, “deficit”, “budget” or “Bank of England”) and Uncertainty (proxied by “uncertain” or “uncertainty”). See the higher blue line in Figure 1, which highlights several economically traumatic events in the UK since 2000.

Working backwards in time, we see the largest EPU spike occurs in Spring 2016 due to Brexit concerns, surpassing even the spikes around the 9/11 attacks and the Second Gulf War, the Northern Rock collapse, the global financial crisis, the European debt crisis and the Scottish independence vote. So the upcoming Brexit referendum appears to be generating an extraordinary level of economic policy uncertainty – at least as gauged by coverage in the Times and Financial Times newspapers.

Indeed, to confirm that the recent surge in policy-related uncertainty reflects Brexit concerns, we created a second index – the lower line in red – which scales our EPU index by the share of EPU articles that also contain “Brexit”, “EU” or “European Union”. In March and April of 2016, nearly 60 per cent of newspaper articles about economic policy uncertainty also contain “Brexit”, “EU” or “European Union”.

So what are the near-term effects of this uncertainty on the UK economy? While it is hard to be sure, we  can use estimated responses to EPU in the US economy from our paper “Measuring Economic Policy Uncertainty” as a guide. In that analysis we estimated that a 90-point upward innovation in the US EPU Index led to short-term declines of 1.2 per cent in US industrial production, about 0.6 per cent in its gross investment and about 0.5 per cent in its level of employment. Since the Brexit-related increase in the UK EPU index appears to be even larger, we think Brexit-related uncertainty is having a material negative effect on UK economic performance.

can use estimated responses to EPU in the US economy from our paper “Measuring Economic Policy Uncertainty” as a guide. In that analysis we estimated that a 90-point upward innovation in the US EPU Index led to short-term declines of 1.2 per cent in US industrial production, about 0.6 per cent in its gross investment and about 0.5 per cent in its level of employment. Since the Brexit-related increase in the UK EPU index appears to be even larger, we think Brexit-related uncertainty is having a material negative effect on UK economic performance.

This Brexit-induced slowdown is partly driven by firms pausing new investment and hiring projects until the future status of the UK is clear – if uncertainty is high and will soon be resolved, it pays to wait to see what the future brings. This is likely to be particularly true for foreign multinationals, for which trade access to Europe is an important benefit of UK investments. Until the Brexit vote takes place, many of these multinationals will be waiting on the sidelines. Why invest in the UK in advance of a close Brexit vote rather than wait a few months? Or, even worse for the UK, why not invest in mainland Europe and avoid the Brexit-related threat of limited access to mainland European markets?

If voters say no to Brexit, UK policy uncertainty is likely to subside rapidly and any harmful effects due to Brexit-related uncertainty are also likely to diminish quickly. But if the voters say yes, then the UK will face an extended period of elevated policy uncertainty as the UK undergoes a protracted separation from the European Union and finds it necessary to re-negotiate many of its international economic agreements.

___

Nicholas Bloom is the William Eberle Professor of Economics at Stanford University, a Senior Fellow of SIEPR, and the Co-Director of the Productivity, Innovation and Entrepreneurship program at the National Bureau of Economic Research. He is a longstanding Associate of the Centre for Economic Performance’s Growth Programme at the LSE.

Image credit: Véronique Debord-Lazaro CC BY-SA

1 Comments