The way the government is attempting to stave off the recessionary impact of the pandemic on the economy means that both the UK budget deficit and debt are rising rapidly. Costas Milas explains why in this context there is an urgent need for government bonds to be linked to GDP.

The way the government is attempting to stave off the recessionary impact of the pandemic on the economy means that both the UK budget deficit and debt are rising rapidly. Costas Milas explains why in this context there is an urgent need for government bonds to be linked to GDP.

Pythagoras famously said that ‘number rules the universe’. Experts, however, do not agree on which number does that. To keep the current pandemic under control, epidemiologists are keen on a COVID-19 reproduction number substantially lower than one. Policy-makers and economists are keen on a 2% economic growth rate which represents the historical median growth of the UK economy over the last three centuries. (Though needless to say, policy-makers would currently be happy with any positive GDP growth number.)

But there is a trade-off, at least in the very short run, between controlling COVID-19 based on non-pharmaceutical interventions and saving jobs by keeping part of the economy open. Current research shows that the greater the strength of government interventions at an early stage, the more effective these are in slowing down or reversing the growth rate of COVID-19 deaths. In fact, the earlier these interventions take place, the smaller the associated economic hit.

The economic consequences for the UK economy can be seen in Figure 1 which plots UK GDP together with Google mobility data. Figure 1 also includes a measure of COVID-19 related stringency measures produced by the Blavatnik School of Government at the University of Oxford. This is an index capturing how strict social distancing rules and other measures are; the higher the index, the stricter the rules. As stringency measures increase, visits to groceries and pharmacies, retail and recreation and workplaces take a hit and, consequently, UK GDP also suffers. Notice that retail and recreation revived in August 2020 when the government introduced the ‘Eat out to Help out Scheme’. From September onwards, however, retail and recreation has been on the slide again. The latest data suggests that in August 2020 GDP stood 9.3% below its pre-pandemic level.

Figure 1: UK recovery, stringency measures and Google mobility data

Data sources: UK real GDP Google mobility data and Government Response Stringency Index

Data sources: UK real GDP Google mobility data and Government Response Stringency Index

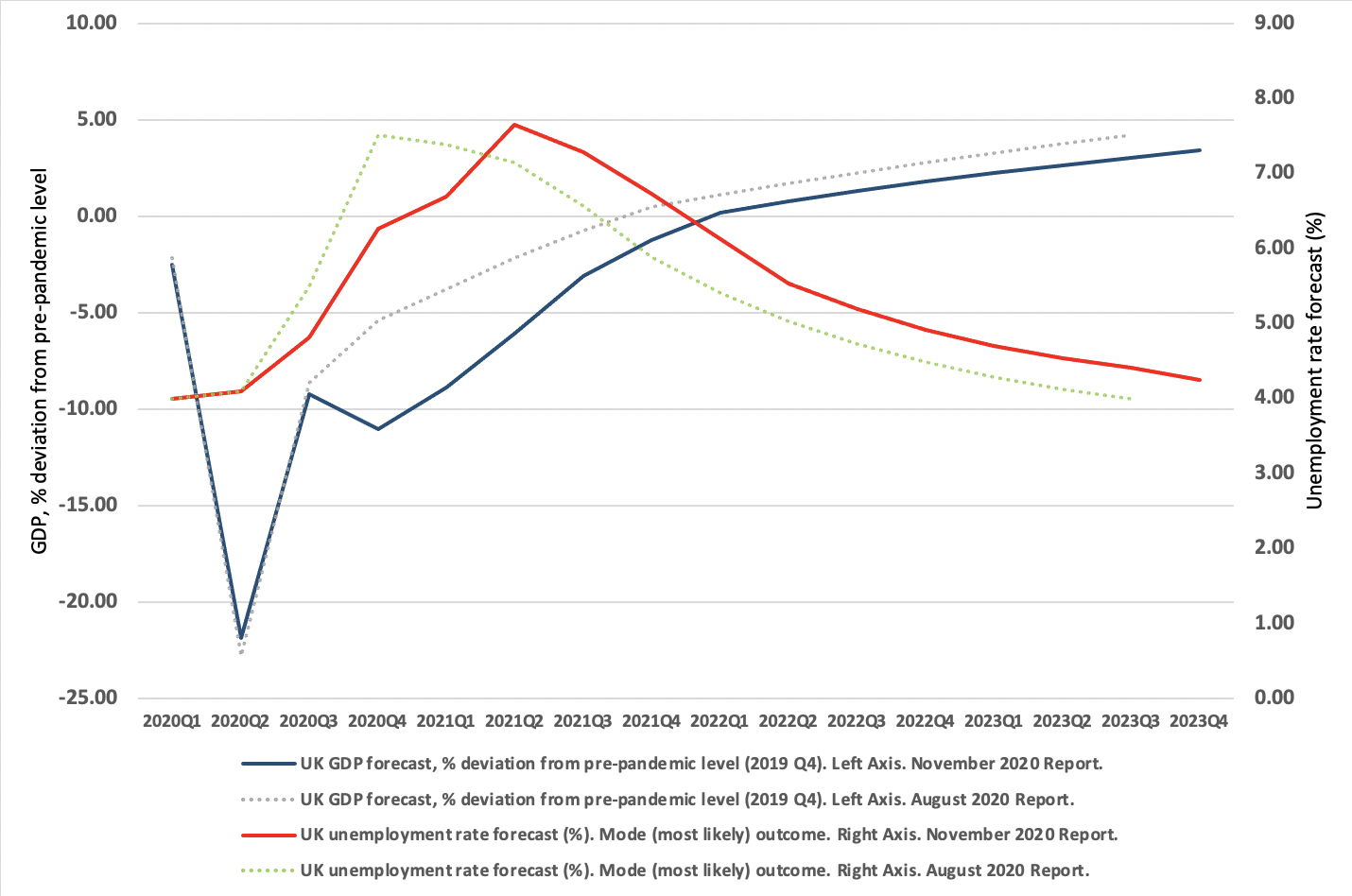

The latest Bank of England Monetary Policy Report predicts that, in the presence of the second lockdown, and without taking into account the possibility of further lockdowns, GDP will follow an (incomplete) “W-type” recovery. This suggests a double-dip recession, as UK GDP is expected to shrink by 11% per annum in 2020Q4 and by 6.5% per annum in 2021Q1 before recording strong annual growth of 11% in 2021Q4. In fact, as Figure 2 suggests, the Bank has revised both its GDP and unemployment rate forecasts quite notably relative to its predictions only three months ago. It now predicts that UK real GDP will return to its pre-pandemic level as late as 2022Q1, whereas the UK unemployment rate will rise to 7.65% in 2021Q2 before returning to its pre-pandemic level in mid-2023.

Figure 2: UK real GDP and unemployment rate forecasts (quarterly data)

Note: Forecasts are based on market expectations of interest rates and current support measures. Source: Bank of England.

Note: Forecasts are based on market expectations of interest rates and current support measures. Source: Bank of England.

To support the economy, the Bank of England has authorised an additional £150bn of quantitative easing. This is the policy that aims to shore up the financial system by creating new money to buy assets like government bonds. Nevertheless, quantitative easing is fairly ineffective in the current environment of extremely low interest rates. In other words, injecting more quantitative easing in an attempt to lower the country-specific costs of borrowing, which is in turn intended to pass through to lower corporate borrowing, has most likely reached (or is about to reach) its limits.

Rishi Sunak rightly relies on fiscal policy to stave off the recessionary impact of COVID-19. He just announced an extension of his Job Retention Scheme until March 2021. For those of us who thought that the Bank’s unemployment rate forecasts in Figure 2 above looked rather optimistic, Sunak’s announcement will strengthen their credibility (it looks unlikely that these forecasts had considered these new measures). In doing so, however, the government’s policy means that both the UK budget deficit and debt are rising rapidly. The International Monetary Fund predicts that the UK’s budget deficit will jump from 2.2% of GDP in 2019 to 16.5% of GDP in 2020 whereas its gross debt will jump from 85.3% of GDP in 2019 to 108% in 2020. This borrowing will have to be paid back in the future. To raise the money, Sunak will have to increase taxes and/or cut public expenditure in the not-so-distant future. Which brings into the picture the urgent need for government bonds to be linked to GDP.

The idea here is that the interest due on GDP-linked bonds would go up or down depending on the issuing country’s economic performance. When GDP growth is weak, its debt-servicing costs will decline. The ratio of its debt to GDP will therefore rise less sharply during a downturn, thus reducing the need for austerity to bring down the debt pile later. On the other hand, when GDP growth is strong and tax revenues are on the rise, the debt-servicing costs will increase. In other words, the UK would have to pay more when it could afford it, and significantly less when it could not. In fact, recent research at the Bank of England suggests that yields on these hypothetical bonds would be lower than those on conventional US bonds. Needless to say, once many countries issue these bonds, these can become part of a well-diversified portfolio which will allow investors to share risk and benefit from growth.

History is telling us that between 1935 and 2017, the median 10-year borrowing cost in the UK was 5.2%. Currently, the 10-year UK cost of borrowing is around 0.25%. Do we really believe that, in light of rapidly deteriorating fiscal conditions, we will keep on borrowing at such a low rate for very much longer? Whether we believe it or not, why not hedge against adverse risk by issuing GDP-linked bonds?

___________________

Costas Milas is Professor of Finance at the University of Liverpool.

Photo by Max Fuchs on Unsplash.